Selling vehicles to vehicles: “The WMPs [wealth management product] used to be predominantly sold to the public, but now they’re increasingly being sold to banks and other WMPs.”

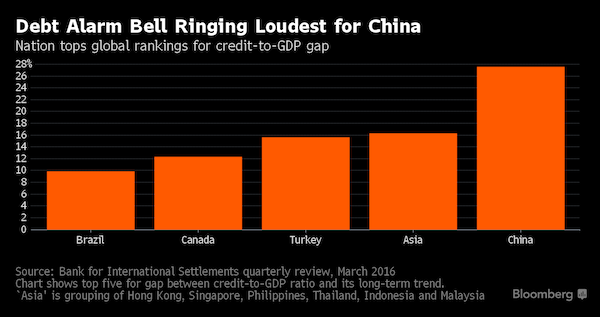

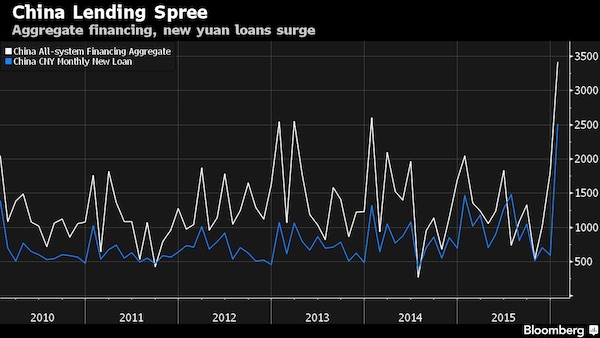

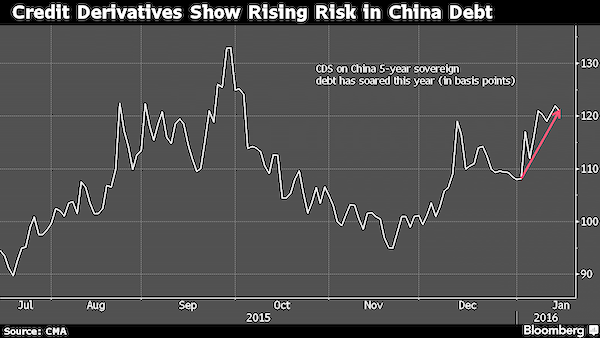

Charlene Chu, a banking analyst who made her name warning of the risks from China’s credit binge, said a bailout in the trillions of dollars is needed to tackle the bad-debt burden dragging down the nation’s economy. Speaking eight days after a Communist Party newspaper highlighted dangers from the build-up of debt, Chu, a partner at Autonomous Research, said she was yet to be convinced the government is serious about deleveraging and eliminating industry overcapacity. She also argued that lenders’ off-balance-sheet portfolios of wealth-management products are the biggest immediate threat to the nation’s financial system, with similarities to Western bank exposures in 2008 that helped to trigger a global meltdown.

The former Fitch Ratings analyst uses a top-down approach to calculating China’s bad-debt levels as the credit to GDP ratio worsens, requiring more credit to generate each unit of GDP. She’s on the bearish side of the debate about the outlook for China and has sounded warnings since the nation’s credit binge began in 2008. “China’s debt problems are large and severe, but in some respects a slow burn. Over the near term, we think the biggest risk is banks’ WMP [wealth management product] portfolios. The stock of Chinese banks’ off-balance-sheet WMPs grew 73% last year. There is nothing in the Chinese economy that supports a 73% growth rate of anything at the moment.

Regardless of all of the headlines and announcements about the authorities cracking down on WMPs, they have done very little, really, and issuance continues to accelerate. “We call off-balance-sheet WMPs a hidden second balance sheet because that’s really what it is – it’s a hidden pool of liabilities and assets. In this way, it’s similar to the Special Investment Vehicles and conduits that the Western banks had in 2008, which nobody paid attention to until everything fell apart and they had to be incorporated on-balance-sheet. “The mid-tier lenders is where these second balance sheets are very large. China Merchants Bank is a good example. Their second balance sheet is close to 40% of their on-balance-sheet liabilities. Enormous.”

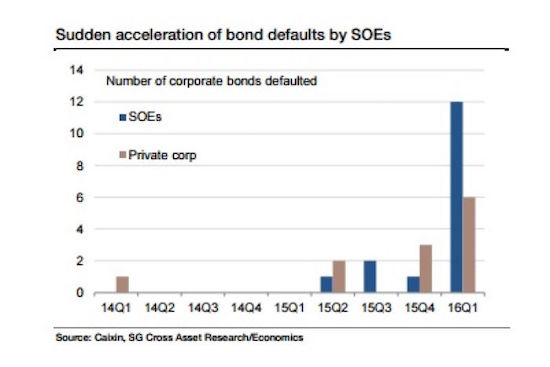

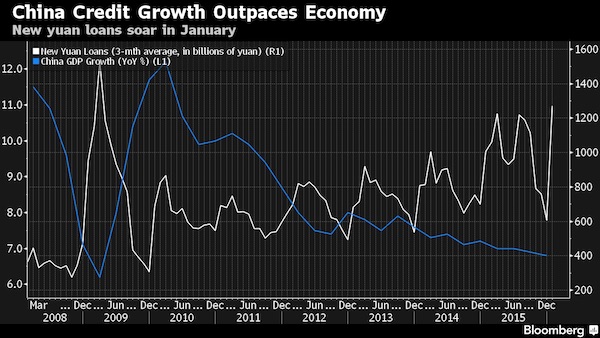

Chinese banks are looking down the barrel of a staggering RMB 8 trillion – or $1.7 trillion – worth of losses according to the French investment bank Societe Generale. Put another way, 60% of capital in China’s banks is at risk as authorities start the delicate and dangerous process of reining in the debt-bloated and unprofitable state-owned enterprise (SOE) sector. Disturbingly though, debt is not only not shrinking, it is accelerating, making the eventual reckoning far worse. China’s overall non-financial debt grew by 15.2% in 2015 to RMB 167 trillion ($35 trillion) or almost 250% of GDP. That is up from 230% of GDP the year before and the 130% it was eight years ago before the global financial crisis hit.

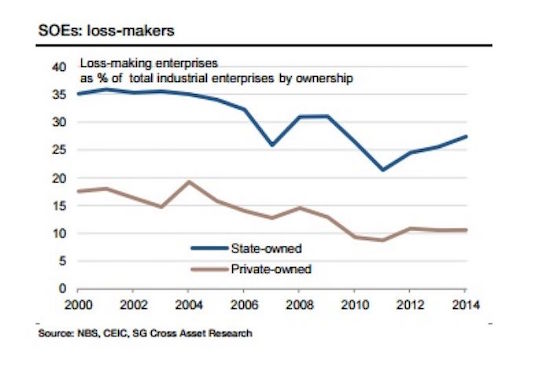

The problem is largely centred on China’s 150,000 or so SOEs, which suck-up an entirely disproportionate amount of the nation’s capital. “Although contributing to less than one-third of economic output and employment, SOEs take up nearly half of bank lending (RMB 37 trillion) and more than 80% of corporate bond financing (RMB 9.5 trillion),” Societe Generale found. “While the inefficiency of SOEs is gradually dragging down economic growth, recognising even a small share of SOEs’ non-performing debt would easily overwhelm the financial system.” Despite their moribund financial performance, the SOEs still enjoy a considerable advantage in access to funding through the banking system than the private sector.

“To put things into perspective, a quarter of SOEs’ loans and bonds are equivalent to the entire capital base of commercial banks plus their loan-loss reserves, equivalent to 23% of GDP,” Societe Generale’s China economist Wei Yao said. On the bank’s figures, if just 3% of loans to SOEs sour, commercial banks’ non-performing loans would double.

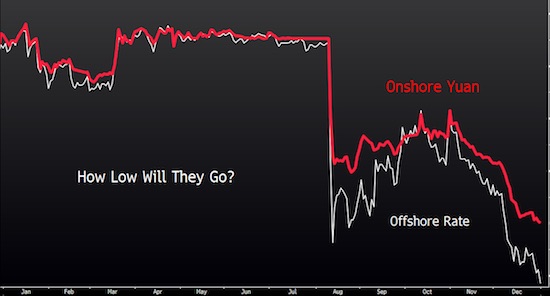

Behind closed doors in March, some of China’s most prominent economists and bankers bluntly asked the People’s Bank of China to stop fighting the financial markets and let the value of the nation’s currency fall. They got nowhere. “The primary task is to maintain stability,” said one central-bank official, according to previously undisclosed minutes of the meeting reviewed by The Wall Street Journal. The meeting left little doubt China’s top leaders have lost interest in a major policy shift announced in a surprise move just nine months ago. In August 2015, the PBOC said it would make the yuan’s value more market-based, an important step in liberalizing the world’s second-largest economy.

In reality, though, the yuan’s daily exchange rate is now back under tight government control, according to meeting minutes that detail private deliberations and interviews with Chinese officials and advisers who spoke with The Wall Street Journal about the country’s currency policy. On Jan. 4, the central bank behind closed doors ditched the market-based mechanism, according to people close to the PBOC. The central bank hasn’t announced the reversal, but officials have essentially returned to the old way of adjusting the yuan’s daily value higher or lower based on whatever suits Beijing best. The flip-flop is a sign of policy makers’ deepening wariness about how much money is fleeing China, a problem driven by its slowing economy.

For now, at least, officials believe the benefits of freeing the yuan are outnumbered by the number of threats. Re-emphasizing the yuan’s stability would also bring a sigh of relief to trading partners who worried a weaker currency would boost Chinese exports at the expense of those produced elsewhere. Freeing the yuan, the biggest overhaul of China’s currency policy in a decade, was meant to empower consumers and help invigorate the economy. The negative reaction, from financial markets world-wide and Chinese who sped their efforts to take money out of the country, was so jarring that the top leadership, headed by President Xi Jinping, began to have second thoughts.

At a heavily guarded conclave of senior Communist Party officials in December, Mr. Xi called China’s markets and regulatory system “immature” and said “the majority” of party officials hadn’t done enough to guide the economy toward more sustainable growth, according to people who attended the meeting. To the central bank, there was only one possible interpretation: Step on the brakes.

Japanese banks reluctant to pay for the privilege of lending are opting out by using derivatives. The options set a floor on rates used to determine interest on loans, and the holder will be paid if the rates fall below that level, according to Aozora Bank and Tokyo Star Bank. The benchmark three-month Tokyo interbank offered rate has plunged to a record low of 6 basis points since the Bank of Japan announced it would start charging fees on some lenders’ reserves in January. Options with floors at zero% or minus rates have been traded recently, according to Aozora Bank. “There’s a need to hedge against money-losing lending that could happen if the Tibor falls to negative levels,” said Tetsuji Matsuka, the head of the ALM planning treasury department at Tokyo Star Bank.

“We think demand will increase” for such products, he said. Japanese banks are getting hurt as the negative-rate policy compresses their lending margins, with the top-three firms including Mitsubishi UFJ Financial forecasting this month that net income will fall a combined 5.2% in the year started April 1. The BOJ’s radical stimulus has already dragged yields on more than 70% of Japanese government bonds to below zero, meaning that investors will have to effectively pay a fee to hold such debt to maturity. In the yen London interbank offered rate market, where some rates are already below zero, options have been traded with floors as low as minus 1%, according to Nobuyuki Takahashi, the general manager of the derivatives sales division at Aozora Bank.

The three-month yen Libor was at minus 0.02% on Friday. Companies that borrow at floating rates may also be able to use floor options to ensure that interest-rate swaps they use to hedge against rising rates don’t end up costing them due to negative rates, Takahashi said. Actual trades of such derivatives are still not that common because the contracts are expensive to buy now, he said. “It will be hard to price these options unless we get more liquidity,” said Tateo Komatsu, a deputy general manager of global markets at Sumitomo Mitsui Trust Bank Ltd. “It will take time for the market to get used to minus rates.”

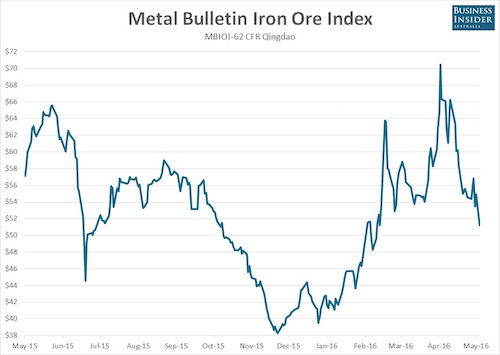

The iron ore price is imploding. Following the ugly lead provided by Chinese futures on Monday, the spot iron ore price followed suit, suffering one of the largest declines seen in years. According to Metal Bulletin, the spot price for benchmark 62% fines fell by 6.69%, or $3.67, to $51.22 a tonne, leaving it down 27.3% from the multi-year peak of $70.46 a tonne struck on April 21. The decline was the third-largest in percentage terms in the past two years, and left the price at the lowest level seen since March 3 this year. The losses in physical and futures markets followed news that Chinese iron ore port inventories swelled to over 100 million tonnes last week, leaving them at the highest level seen since March last year.

That followed the revelation that Chinese crude steel output contracted in April after hitting a record high in March, declining marginally according to figures released by the China Iron and Steel Association (CISA). Given the increasing correlated relationship between the two, it’s also clear that an unwind of speculative positioning in Chinese iron ore futures is also impacting prices in the physical iron ore market. After watching prices in many bulk commodity futures rally more than 50% in less than two months, regulators at both the Dalian Commodities Exchange and Shanghai Futures Exchange introduced measures in recent weeks to discourage excessive levels of speculation in these markets.

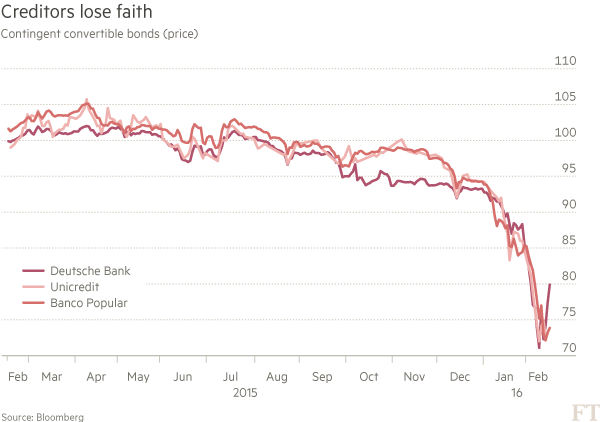

Deutsche Bank had its credit rating cut by Moody’s Investors Service, which said the German lender faces mounting challenges in carrying out its turnaround. The bank’s senior unsecured debt rating was lowered to Baa2 from Baa1, Moody’s said Monday in a statement. That left the grade two levels above junk. The firm’s long-term deposit rating fell to A3 from A2. “Deutsche Bank’s performance over the last several quarters has been weak, and substantial operating headwinds, including continuing low interest rates and macroeconomic uncertainty, will challenge the firm,” Moody’s said in the statement. CEO John Cryan’s planned overhaul of the bank, laid out in October, ran into an industrywide slump in trading and investment banking, as well as interest rates that have gone from low to negative in parts of Europe and Asia.

Net income fell 61% in the first quarter, leaving the company at risk of a second straight annual loss this year as it tries to resolve legal cases. Results so far and the challenges ahead, including a chance of further slumps in retail and market-linked businesses, will probably force Deutsche Bank to balance restructuring costs with the need to amass capital for stiffened regulatory requirements, Moody’s wrote. “The plan they’re trying to execute is a good plan for the bondholder in the long run, but they face some pretty challenging headwinds when you look at the current operating environment,” Peter Nerby, a senior vice president at Moody’s, said in a phone interview. “They’re working on it, but it’s tougher than it was.”

The IMF has just released its latest Debt Sustainability Analysis (DSA) for Greece. It makes grim reading. Greece is never going to grow its way out of debt. And the 3.5% primary surplus to which the Syriza government seems hell-bent upon committing is frankly unbelievable: the IMF thinks sustaining even 1.5% would be a stretch. Banks will need another €10bn (on top of the €43bn the Greek government has already borrowed to bail them out). Asset sales are a lost cause, mainly because the banks – which were a large proportion of the assets up for sale – won’t be worth anything for the foreseeable future. Like it or not, debt relief will be necessary. If there is no debt relief, by 2060 debt service will soar to an impossible 60% of government spending. Of course, Greece would default long before that – but that would make the situation in Greece even worse.

None of this is news. The IMF has been saying for nearly a year now that Greece will need debt relief. This latest DSA is designed to shock the Europeans into giving it serious consideration. It is not surprising, therefore, that the debt sustainability projections are significantly worse than in previous DSAs. No doubt the European creditors will disagree with them, the Syriza government will side with the Europeans because the only alternative is Grexit, and the European Commission will claim there is “progress” when all that is really happening is that a very battered can is being kicked once again. But buried in the IMF’s report are some very unpleasant numbers indeed – the IMF’s projections for population and employment out to 2060. And I think the world should know about them. Here is what the IMF has to say about the outlook for Greek unemployment:

Demographic projections suggest that working age population will decline by about 10 percentage points by 2060. At the same time, Greece will continue to struggle with high unemployment rates for decades to come. Its current unemployment rate is around 25%, the highest in the OECD, and after seven years of recession, its structural component is estimated at around 20%. Consequently, it will take significant time for unemployment to come down. Staff expects it to reach 18% by 2022, 12% by 2040, and 6% only by 2060. So even if the Greek economy returns to growth and its creditors agree to debt relief, it will take 44 years to reduce Greek unemployment to something approaching normal. For Greece’s young people currently out of work, that is all of their working life. A whole generation will have been consigned to the scrapheap.

Almost everyone who gives the matter serious thought agrees that George Osborne and David Cameron want to reshape Britain. The spending cuts, the upending of the NHS, even this month’s near-miss over the BBC: signs lie everywhere of how this will be a decade, maybe more, of massive change. Yet even now it is little understood just how far Britain might shift – and in which direction. Take austerity, the word that will define this government. Even its most astute critics commit two basic errors. The first is to assume that it boils down to spending cuts and tax rises. The second is to believe that all this is meant to reduce how much the country is borrowing. What such commonplaces do is reduce austerity to a technical, reversible project.

Were it really so simple all we would need to do is turn the spending taps back on and wash away all traces of Osbornomics. Austerity is far bigger than that: it is a project irreversibly to transfer wealth from the poorest to the richest. It’s doing the job very nicely: while the typical British worker is still earning less after inflation than he or she was before the banking crash, the number of UK-based billionaires has nearly quadrupled since 2009. Even while he slashes benefits, Osborne is deep into a programme to hand over much of what is still owned by the British public to the wealthiest. Privatisation is the multibillion-pound centrepiece of Osborne’s austerity – yet it rarely gets a mention from either politicians or press. The Queen mentioned it in her speech last week, but the headline writers ignored it.

And if you don’t know that this Thursday is the closing date for consultation on the sale of the Land Registry, our public record of who owns what property, that’s hardly your fault – I haven’t spotted it in the papers, either. But without getting rid of prize assets, Osborne’s austerity programme falls apart. At a time when tax revenues are more weak stream than healthy flood, those sales bring much-needed cash into the Treasury and make his sums add up. The independent Office for Budget Responsibility has ruled that the only reason the chancellor met his debts target last year was because he flogged off our public assets. And what a fire sale that was, with everything from our last remaining stake in the Royal Mail to shares in Eurostar shoved out the door in the biggest wave of privatisations of any year in British history.

A US appeals court has opened the door for more claims against the big banks for rigging benchmark interest rates, by overturning a three-year-old ruling which threw out a host of private antitrust-related lawsuits. Monday’s decision by the 2nd US Circuit Court of Appeals in Manhattan could be a setback for the likes of Bank of America, JPMorgan Chase and Citigroup, which had hoped that most of the wave of post-crisis litigation was behind them. The decision reverses a lower court decision from 2013, in which US District Judge Naomi Reice Buchwald dismissed claims on the grounds that the plaintiffs had failed to plead antitrust injury.

The lawsuits had accused 16 major banks of collusion in manipulating the London interbank offered rate, or Libor, which approximates the average rate at which a select group of banks can borrow money. Beginning in 2007, the plaintiffs argued, the banks engaged in a horizontal price-fixing conspiracy, with each submitting an artificially low cost of borrowing US dollars in order to drive Libor down. At the time of her rejection, Judge Buchwald reasoned that the Libor-setting process was co-operative rather than competitive, and so any attempt to depress the rate did not cause investors to suffer anti-competitive harm. At best, she said, investors had a fraud claim based on misrepresentation.

But the appeals court on Monday disagreed and sent the case back to the lower court for further proceedings. A three-judge panel found that price-fixing was an antitrust violation in itself, and therefore needed no separate plea of harm. “The crucial allegation is that the banks circumvented the Libor-setting rules, and that joint process thus turned into collusion,” the panel said. The private suits are separate from the criminal and civil probes into Libor rigging, which have ensnared banks and traders around the world and drawn about $9bn so far in penalties.

Italian vessels have helped rescue more than 2,600 migrants from boats trying to reach Europe from North Africa in the last 24 hours, the coastguard said on Monday, indicating that numbers are rising as the weather warms up. Some 2,000 migrants were rescued off the Libyan coast from 14 rubber dinghies and one larger boat in salvage operations by the Italian navy and coastguard, the medical charity Medecins Sans Frontieres and an Irish navy vessel, the coastguard said. Another 636 migrants were rescued from two boats in Maltese waters, in operations involving Maltese and Italian vessels, it said. It gave no information about the nationalities of those saved. More than 31,000 migrants have reached Italy by boat so far this year, slightly fewer than in the same period of 2015.

Humanitarian organizations say the sea route between Libya and Italy is now the main route for asylum seekers heading for Europe, after an EU deal on migrants with Turkey dramatically slowed the flow of people reaching Greece. Officials fear the numbers trying to make the crossing to southern Italy will increase as conditions improve in warmer weather. More than 1.2 million Arab, African and Asian migrants fleeing war and poverty have streamed into the European Union since the start of last year. Most of those trying to reach Italy leave the coast of lawless Libya on rickety fishing boats or rubber dinghies, heading for the Italian island of Lampedusa, which is close to Tunisia, or toward Sicily.

Greek police started moving migrants and refugees out of a sprawling tent camp on the sealed northern border with Macedonia on Tuesday where thousands have been stranded for months trying to get into western Europe. Reuters witnesses saw several bus loads of migrants leaving the makeshift camp of Idomeni early on Tuesday morning, with about another dozen buses lined up. It appeared to be mainly families who were on the move. Greek authorities said they planned to move individuals gradually to state-supervised facilities further south in an operation expected to last several days. “The evacuation is progressing without any problem,” said Giorgos Kyritsis, a government spokesman for the migrant crisis.

A Reuters witness on the Macedonian side of the border said there was a heavy police presence in the area but no problems were reported as people with young children packed up huge bags with their belongings. Media on the Greek side of the border were kept at a distance and a group of people dressed as clowns waved balloon hearts and animals as the buses drove past. “Those who pack their belongings will leave, because we want this issue over with. Ideally by the end of the week. We haven’t put a strict deadline on it, but more or less that is what we estimate,” Kyritsis told Reuters. At the latest tally, 8,199 people were camped at Idomeni after a cascade of border shutdowns throughout the Balkans in February barred migrants and refugees from central and northern Europe. More than 12,000 lived in the camp at one point.

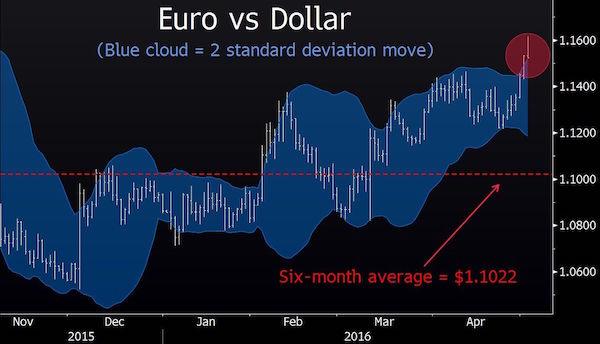

The foreign exchange market is notorious for overshooting. A currency that starts moving in a particular direction as economic fundamentals change will often end up at a rate that can’t be justified by the data. So trying to nudge the matrix of currency values is akin to policy makers attempting to steer a Ouija board pointer – which is exactly what seems to have happened since their February Group of 20 meeting in Shanghai produced a tacit truce in the currency war. Suspicions that finance ministers had agreed in February to stop talking their currencies down seemed confirmed by the dollar’s decline of more than 6% from its Jan. 20 peak.

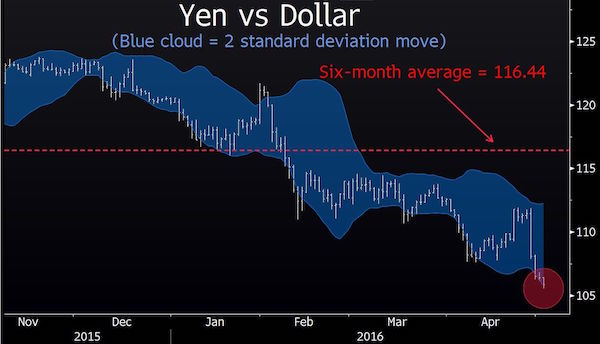

China’s recent moves to boost the yuan’s reference rate to its highest levels this year also backed the impression of a suspension of hostilities. But while U.S. manufacturers worried that a too-strong dollar would threaten their exports and profits, the recent reversal, and gains for the euro and the yen, pose bigger risks to the struggling economies of Europe, and Japan. The euro, for example, pierced $1.16 on Tuesday, reaching its highest level since August:

The yen, meanwhile, has breached 106 to the dollar, down from as weak as 122 in January:

Those are the kinds of moves that make central banks uncomfortable – especially when, like the ECB and the BOJ, they’re already struggling to avert deflation. Australia’s surprise decision to cut interest rates overnight, driving its currency lower against all 31 of its major trading peers, is a sign that skirmishes might be breaking out again. Marcus Ashworth, a strategist at Haitong Securities in London, said in a research note: The rumor mill has been incessant (despite official denials) that the so-called Shanghai G-20 accord to pacify markets and quell unrest between the members has actually served to make international relations as toxic as they have been for many years.

The Shanghai deal was to stop the negative feedback loop and thereby prevent a sharp devaluation of the yuan; however, it was meant to curtail the rise of the dollar, not sharply reverse it. [..] It’s clear the Treasury doesn’t want the dollar to resume its ascent. But it’s also clear that trying to steer the currency market into stasis has failed, and that the inflation outlooks in both the euro zone and Japan are deteriorating. The environment looks ripe for hostilities to break out again, providing yet another reason to be pessimistic about the prospects for a global economic recovery.

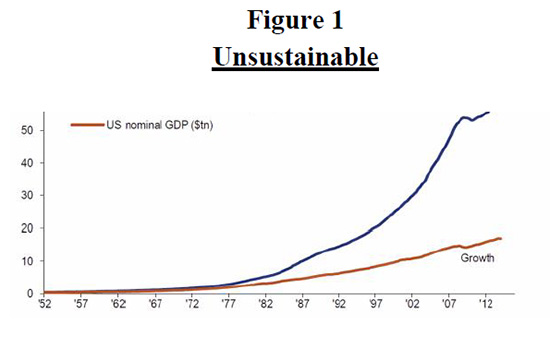

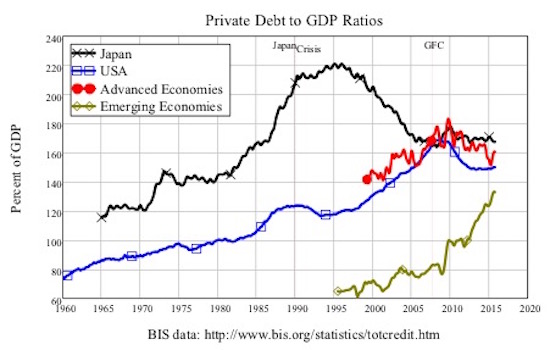

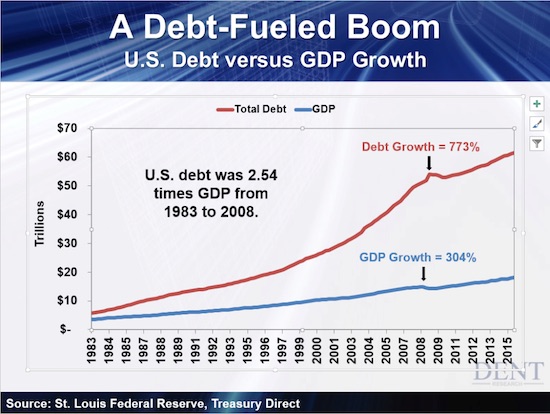

According to Hoisington and Hunt, the ratio of nonfinancial debt-to-GDP rose to 248.6% at the end of 2015, higher than the previous record of 245.5% set in 2009 and well above the average of 167.5% since this figure started to be tracked in 1952. They also point out that since 2000 it has taken $3.30 of debt to generate $1.00 of GDP compared with $1.70 in the 45 years prior to 2000. This points to the fact that a greater proportion of new debt is devoted to unproductive uses. Debt drains away vital resources from economic growth. Fighting a debt crisis with more debt is doomed to failure, yet that is not only what global central banks did during the crisis but long after markets stabilized (though the crisis never truly ended, just slowed). This was an epic policy failure that continues today.

U.S. government debt is growing to unsustainable levels. Gross debt (excluding off-balance sheet items) reached $18.9 trillion at the end of 2015, equal to 104% of GDP (considerably higher than the 63-year average of 55.2%). Government debt increased by $780.7 billion in 2015, or $230 billion more than the nominal or dollar rise in GDP. This actual debt increase is considerably larger than the budget deficit of $478 billion reported by the government because many spending items were shifted off-budget. Readers should remember this the next time The WSJ editorial page trumpets that the deficit dropped significantly from the four consecutive years of $1 trillion+ deficits between 2009 and 2012. And these figures don’t even touch upon the $60 trillion of unfunded liabilities (calculated on a net present value basis) for Social Security and other entitlement programs.

Globally, the debt picture is more disturbing. Total public and private debt/GDP is 350% in China, 370% in the U.S., 457% in Europe and 615% in Japan, respectively. Those numbers should speak for themselves.

Strolling through Tokyo on a Sunday afternoon, it’s hard to tell Japan’s economy is a mess. Deflation has returned, while growth hasn’t. But Shibuya Crossing remains as packed with diners, bag-toting shoppers and gawking tourists as ever. Nearby, a line of more than 50 people stretches outside a restaurant selling overpriced burgers. Lost decades be damned! Japan had the good fortune to have become wealthy before entering its years of stagnation. Some Japanese are now suffering in an economy that’s endured four recessions in eight years; the poverty rate has reached 16%, its highest level on record. But for many, especially in big cities such as Tokyo, life hasn’t so much deteriorated as frozen in time. GDP per capita, on a nominal basis, is little different now than in 1992.

And though the quality of many jobs has waned due to the increase of temporary work, joblessness remains a rarity. The unemployment rate is an enviable 3.2%. The Shibuya crowds raise serious and uncomfortable questions about the direction of Tokyo’s economic policy. Even as some analysts urge the Bank of Japan to double down on its monetary easing program and the government to ramp up its own spending in an effort to boost inflation, there’s a good argument to be made that the approach of Japan’s policymakers has been dead wrong, and for a very long time. The thrust of Japanese policies since the bursting of its gargantuan asset-price bubble in the early 1990s has been to spur growth with lots and lots of cash, whether from the government or the BOJ.

Since 2013, Prime Minister Shinzo Abe has dramatically pumped up that strategy – running large budget deficits, delaying taxes and encouraging the BOJ to print money on an ever grander scale. Arguably, however, Japan’s main focus should be to preserve the wealth it’s already accumulated. With a population that’s aging and shrinking, Japan can get richer on a per capita basis even if GDP remains perfectly flat. In that sense, deflation – long considered the scourge of Japan’s economy – is actually a boon: Falling prices raise the future value of savings, helping the elderly and others on fixed incomes. In constant terms, Japan’s GDP per capita is 17% higher than in 1992, thanks to deflation.

The 1980s were the apex of Japanese culture and economic might. Back then, Japan’s economy was growing so fast, it was thought they would overtake the US. But that all came to a screeching halt. Truth is, Japan’s meteoric rise was fueled by an epic lending bubble. Similar to the Roaring 20s in America. And when the bubble popped, the government launched massive and misguided measures that set Japan back decades. Their economy hasn’t expanded since. They are stuck in the 1980s. There’s been no growth for 30 years. And as you’ll hear about this in this special bonus video, the United States could be going down the same path. Imagine, if we are stuck in the 2000s for the next couple decades. How will you ever be able to retire?

Euro zone retail sales fell more than expected in March against February as consumers cut purchases of food, drinks and tobacco, the EU’s statistics office said on Wednesday. Retail sales, a proxy for household spending, decreased 0.5% in March month-on-month in the 19-country currency union, Eurostat said. Economists polled by Reuters had forecast a much smaller decrease of 0.1%. Yearly figures were also lower than expected, with sales up 2.1%, below market forecasts of a 2.5% rise. The fall in March sales was partly offset by an upward revision of data for February.

Eurostat said on Wednesday that in February sales rose 0.3% on a monthly basis and 2.7% year-on-year. It had previously estimated an increase of 0.2% monthly and 2.4% yearly. On a monthly basis, retail sales of food, drinks and tobacco products dropped 1.3% in March, the biggest fall among all the categories. Sales of non-food products, excluding automotive fuels, went down 0.5% month-on-month. Purchases of fuel for cars also dropped 0.4% on a monthly basis. Among the largest euro zone economies, Germany posted a 1.1% monthly drop of retail sales and France recorded a decrease of 0.7%. In Spain, sales increased 0.4% on a monthly basis in March.

Kyle Bass, founder of Hayman Capital Management, said investors wouldn’t be investing in China if they realized how vulnerable its banking system is. “Common sense will tell you that they are going to have a loss cycle,” he said at the Milken Institute Global Conference in Beverly Hills, California, on Wednesday. “So if you think about how precarious that system is, you wouldn’t be allocating money to China.” Bass, a hedge fund manager famed for betting against U.S. subprime mortgages, is predicting losses for China’s banks and raising money to start a dedicated fund for bets in the nation. Bass said investors putting money in Asia should ask if they can handle 30 to 40% writedowns in Chinese investments.

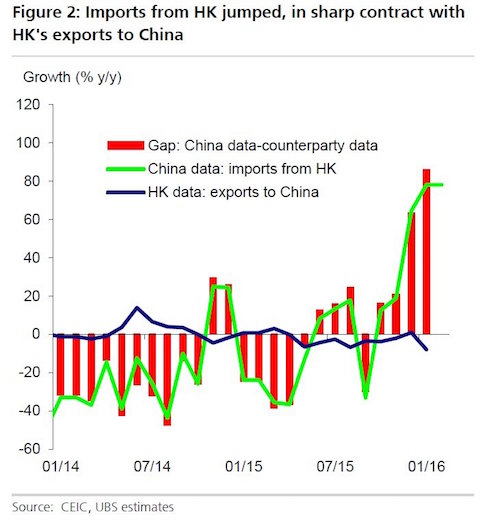

Hong Kong is conducting a multi-pronged customs, shipping and financial sector crackdown against so-called fake trade invoicing that allows billions of dollars of capital to leave China illegally. Hong Kong’s central bank told Reuters it has beefed up its scrutiny of banks’ trade financing operations, while customs officials are doing more random checks on shipments crossing border posts and conducting raids on warehouses to ensure the authenticity of goods, senior officials working in shipping, logistics and banking said. The head of a logistics company said surprise customs inspections at Hong Kong border posts had doubled. The sources[..] said the increased efforts began this year and reflected concerns about billions of dollars in illicit cash authorities suspect are being channeled through Hong Kong following a stock market crash in China last year.

“Examinations and investigations reflect one of the strongest trends we are seeing now in the financial sector,” said Urszula McCormack, a partner at law firm King & Wood Mallesons, which helped co-author a report published by The Hong Kong Association of Banks in February that highlighted shipping as a sector where fake invoicing can thrive. “(Hong Kong) regulators are now in enforcement mode.” China has become increasingly concerned about capital outflows since the middle of last year when Chinese rushed to get money offshore for safekeeping or to invest following the stock market slump and unexpected yuan devaluation. Hong Kong is the most popular route, analysts say, because of its proximity to China.

Nobody quite knows what it means for a bank to be “too big to fail,” so the regulators in charge of solving the problem have an understandable focus on tidiness. A bank that fails tidily, sensibly, in neat little compartments, probably won’t do much damage to anyone else. A bank whose failure is sprawling and incomprehensible might well turn out to be catastrophic. So the preferred mechanism for winding up a possibly too-big-to-fail bank these days is largely about compartmentalization. You put all of the important, messy stuff into subsidiaries – put the deposits in a bank subsidiary, the repurchase agreements and derivatives in a broker-dealer subsidiary, etc. – and put those subsidiaries under a “clean” bank holding company with a fairly large amount of capital and long-term debt.

Then if things go horribly wrong, the holding company’s shareholders and bondholders are the ones who lose money, shielding the people who have messier and more systemic claims on the subsidiaries. The regulators swoop in and recapitalize the holding company, or just sell the subsidiaries to other, healthier banks, in any case without ever interrupting service at the systemic subsidiaries. All the bad stuff happens at the holding company, all the important stuff happens at the subsidiaries, and you try to avoid mixing the two. Then all you have to do is make sure that the holding company has enough equity and long-term debt to shield the subsidiaries against any plausible bad outcome. But to make this work you really need to keep things in their boxes. Derivatives have a tendency to want to jump out of their boxes.

In particular, if bad things are happening at a large and systemically important bank holding company, there isn’t a lot of reason for the bank’s derivatives counterparties and repo creditors to stick around. Repo is meant to be a super-safe place to park your money overnight; if it looks like a repo counterparty might default, then you look for a different counterparty. And derivatives are just supposed to work: If Bank A owes you money under an interest-rate swap, and you owe Bank B money under an offsetting swap, and Bank A defaults, then all of a sudden you have an unanticipated unhedged risk. So if your derivatives or repo counterparty gets in trouble, you bail immediately to protect yourself. (Also there is always the possibility of making a lot of money on the unwind.) But while this is individually rational, it is systemically bad. As Janet Yellen put it yesterday:

“The crisis underscored that when a large financial institution gets into trouble, its failure can destabilize other firms. This is because large banking organizations are connected with each other by the business they do together and through the contracts that result from that business. Indeed, in the 21st century, a run on a failing banking organization may begin with the mass cancellation of the derivatives and repo contracts that govern the everyday course of financial transactions. When these contracts, known collectively as Qualified Financial Contracts or QFCs, unravel all at once at a failed large banking organization, an orderly resolution of the bank may become far more difficult, sparking asset firesales that may consume many firms.”

So yesterday U.S. banking regulators proposed new rules to prevent that from happening. The rules basically say that a bank subsidiary’s derivatives and repo contracts can’t be cancelled for 48 hours after the bank’s holding company files for bankruptcy or otherwise enters resolution proceedings. This gives the regulators two days to swoop in and conduct the neat resolution of the bank before its derivatives spill out everywhere and create a mess.

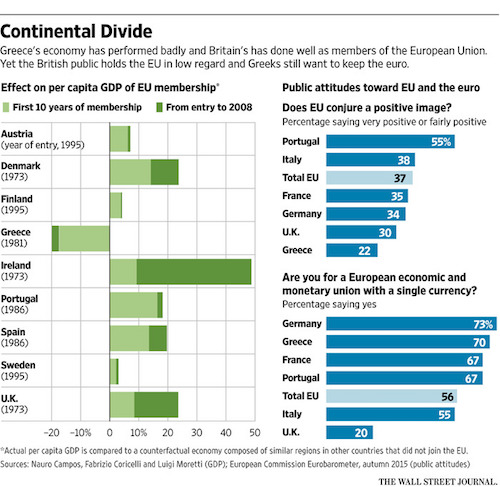

Britain’s flirtation with leaving the European Union is as puzzling as Greece’s stubborn desire to stay. After all, Britain’s economy has done quite well inside the bloc while Greece’s has been decimated. What explains both sentiments is that the European project has always been about more than economics. It also seeks “an ever closer union among the peoples of Europe,” as the Treaty of Rome, its founding charter, declared in 1957. “Closer union” with Europe deeply appeals to Greeks, whose own state has failed them so badly. But it repels many Britons, whose state works just fine and who want no part of a European political union. For them, the quagmire of the euro, which Britain hasn’t adopted, is a cautionary tale of what such a union could bring.

How they decide between the economic benefits and political risks of staying could determine whether Britain votes to leave the EU in a June 23 referendum. Greece joined the European Economic Community, the EU’s predecessor, in 1981, in search of shelter from foreign invaders, domestic coups, and its own dysfunctional government. Economics actually argued against membership: EEC technocrats said Greece wasn’t ready, but were overruled by political leaders worried about geopolitical instability on the Continent’s southern flank. The same logic brought Greece into the euro in 2001 when its debts and deficits should have disqualified it. Greece’s underdeveloped, overprotected economy was poorly prepared for life inside the EU.

A study led by Nauro Campos of Brunel University concluded only Greece was poorer in 2008 for having joined the EU; Britain, they reckon, was 24% richer. Eurozone membership initially brought down Greek interest rates and unleashed a borrowing binge but resulted in crisis and a six-year depression. Yet Greeks still don’t want to give up the euro. “Anglo Saxons think the euro is only an economic and financial project,” said Yannis Stournaras, governor of the Greek central bank, in an interview. “It’s political as well. It’s a means to an identity. We feel safer in the euro.” British considerations were just the opposite. A Conservative government took Britain into the EEC in 1973 largely for its trade benefits, a decision voters overwhelmingly approved in a 1975 referendum.

Fresh turmoil in the EU risks triggering the disintegration of the entire bloc, according to Moody’s. In a stark warning, the rating agency said the “painful adjustment” faced by some countries in the eurozone meant the collapse of the single currency area and wider EU was believed by some to be a question of “when” not “if”. Moody’s said that even a “small crisis” threatened to set off an uncontrollable chain of events that would “threaten the sustainability” of the EU and its institutions. The rating agency praised the “significant political progress” made since the crisis in putting the foundations in place for a banking union and creating a eurozone rescue fund. However, it said endless austerity demands in return for bail-outs had fuelled deep resentment across the region, especially in countries weighed down by sky-high unemployment.

“Significant vulnerabilities” facing the bloc such as a British exit from the EU also remained, which would fuel support for “anti-establishment and anti-EU parties elsewhere”, it warned in a report. Colin Ellis, Moody’s chief credit officer for Europe, said a British exit could spark an “existential moment” for the bloc. “Even if the EU survives its current challenges largely unscathed, even a ‘small’ future crisis could threaten the sustainability of current institutional frameworks, if it coincided with negative public sentiment and populist political developments,” the report said. “This can create the impression that the question is when the system breaks, rather than if.”

It came as Mervyn King, the former governor of the Bank of England, warned that the eurozone faced four “unpalatable choices” as policymakers struggle to lift the bloc out of its economic malaise. Lord King said the single currency area would have to choose between an economic “depression” in the south, higher inflation in northern states like Germany, permanent fiscal transfers or a “change of composition of the euro area”. However, he told an audience in Frankfurt that there was “a limit to the economic pain that can be imposed in pursuit of a federal Europe without risking a political reaction. “There are no empires in Europe any more and our leaders would do well not to try to recreate one.”

Unloved, untimely, and unnecessary, the putative free trade pact between Europe and America is dying a slow death. The Dutch people have amassed 100,000 signatures calling for a referendum on this Transatlantic Trade and Investment Partnership, or TTIP. The number is likely to soar after Greenpeace leaked 248 pages of negotiation papers over the weekend. The documents do not exactly show a “race to the bottom in environmental, consumer protection and public health standards” – as Greenpeace alleges – but they do raise red flags over who sets our laws and who holds the whip hand over our eviscerated parliaments. Dutch voters have already rebuked Brussels once this year, throwing out an association agreement with Ukraine in what was really a protest against the wider conduct of European affairs by an EU priesthood that long ago lost touch with economic and political reality.

French president François Hollande cannot hide from that reality. Faced with approval ratings of 13pc in the latest TNS-Sofres poll, a TTIP mutiny within his own Socialist Party, and electoral annihilation in 2017, he is retreating. “We don’t want unbridled free trade. We will never accept that basic principles are threatened,” he said. In Germany, just 17pc now back the project, and barely half even accept that free trade itself a “good thing”, an astonishing turn for a mercantilist country that has geared its industrial system to exports. The criticisms have struck home. The Dutch, Germans, and French, have come to suspect that TTIP is a secretive stitch-up by corporate lawyers, yet another backroom deal that allows the owners of capital to game the international system at the expense of common people.

Weighty principles are at stake. The Greenpeace documents show that the EU’s ‘precautionary principle’ is omitted from the texts, while the rival “risk based” doctrine of the US earns a frequent mention. Clearly, the two approaches are fundamentally incompatible. It is a heresy in our liberal age – a sin against Davos orthodoxies – to question to the premises of free trade, but this tissue rejection of the TTIP project in Europe may be a blessing in disguise. You can push societies too far. [..] The European Commission’s Spring forecast this week has an eye-opening section on the rise of inequality. Without succumbing to the fallacy of ‘post hoc, propter hoc’, it is an inescapable fact that the pauperisation of Europe’s blue collar classes corresponds exactly with the advent of globalisation.

News that Turkish Prime Minister Ahmet Davutoglu, after meeting President Recep Tayyip Erdogan, is to announce the holding of a party congress on Thursday, effectively signifying his resignation, has sent shockwaves through the country. The value of the Turkish Lira dropped from 2.79 to the dollar earlier in the day to 2.94. Davutoglu is expected to make the announcement at 1100am local time. After 14 years in power, the ruling Justice and Development Party (AKP) may be coming apart at the seams. But far more threatening than the unravelling of a political party are fears about the direction in which the country is headed. Both domestic and international critics have for years pointed to the growing authoritarianism and strong-man tactics employed by Erdogan. The fact that he can so easily dismiss the prime minister, a man he rapidly promoted through the ranks, is sending shivers down the spines of many.

“This is a palace coup,” said Yusuf Kanli, a veteran commentator on Turkish politics. “The president wanted the prime minister to step down and that’s it. Now we will have a party convention in May or early June,” Kanli told Middle East Eye. Rumours of tensions within the party have been rife for almost a year, but not even the AKP’s worst enemies had imagined a split could occur on such a scale. Unconfirmed reports suggest the AKP will convene a party congress within 60 days and that Davutoglu will not stand as a candidate. “Events today show that the AKP will move to consolidate Erdogan’s aspirations of becoming a super president. Whether they will succeed remains to be seen. These are very fine political calculations,” Kanli said. The party congress elects the party chairman, who automatically becomes their choice for prime minister.

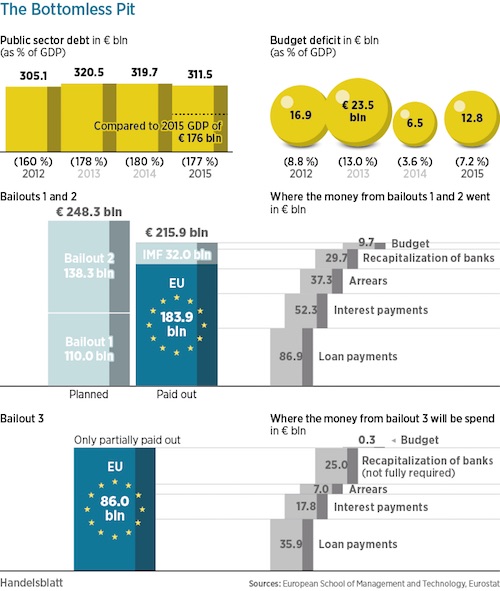

After six years of ongoing bailouts amounting to more than €220 billion, or $253 billion in loans, Greece just cannot get out of crisis mode. It is tempting to blame those who refused to reform the country’s pensions and labor markets for the latest calamity. But a study by the European School of Management and Technology, a copy of which Handelsblatt has obtained exclusively, gives another perspective. The aid programs were badly designed by Greece’s lenders, the ECB, the EU and the IMF. Their priority, the report says, was to save not the Greek people, but its banks and private creditors. This accusation has been around for a long time. But now, for the first time, the Berlin-based ESMT has compiled a detailed calculation over 24 pages.

Their economists looked at every individual loan instalment and examined where the money from the first two aid packages, amounting to €215.9 billion, actually went. Researchers found that only €9.7 billion, or less than 5% of the total, ended up in the Greek state budget, where it could benefit citizens directly. The rest was used to service old debts and interest payments. The report comes as the EU and the Greek government prepare to hold negotiations about further debt relief. E.U. Economics Commissioner Pierre Moscovici said he hoped all sides could reach an agreement at a special meeting of the Eurogroup of euro-zone finance ministers next Monday. Extensions of credit repayment periods, deferments and freezing interest rates are all being discussed. This “debt relief light” would not affect private investors – just the loans from Europeans.

At the moment, German Chancellor Angela Merkel and her colleagues are not inclined to listen to the Greek prime minister, Alexis Tsipras, as he asks for a new multi-billion euro aid package. It is easy to understand why. The chancellor must feel she has seen it all before. She has experienced many near state bankruptcies since early 2010 when she put together the first bailout for Greece. But Jörg Rocholl, president of the European School of Management and Technology said that his institute’s research shows that the biggest problem lies with the way the bailout packages were designed in the first place. “The aid packages served primarily to rescue European banks,” he said. For example, €86.9 billion were used to pay off old debts, €52.3 billion went on interest payments and €37.3 billion were used to recapitalize Greek banks.

Of course, the servicing of debts and interest payments is a major source of expenditure in any state budget – so the Greek state did benefit from it indirectly, as it had also spent the loan money beforehand. But the new calculations do throw doubts on whether the aid programs were sensibly constructed: The loans were used to service debt, although Greece has been de facto bankrupt since 2010.

Apart form the obvious human tragedy, I don’t know why, but nobody talks about this being the end of the tar sands industry. That’s a real possibility, though. Nearly all workers live in the town. And so oil prices are up a bit for the moment.

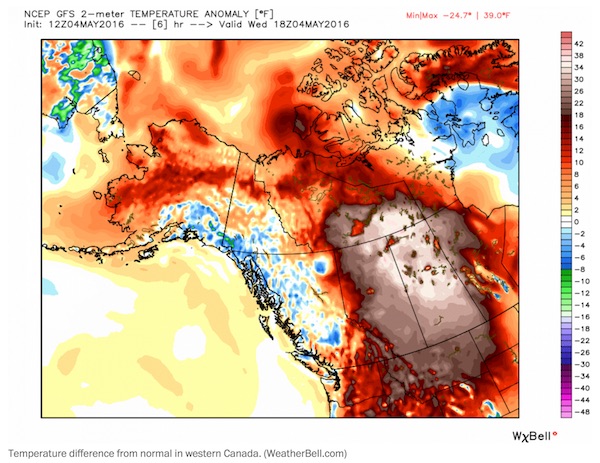

On Monday, residents of Fort McMurray watched anxiously as wildfires burned southwest of the northern Alberta city. Fort Mac’s streets are carved out of the boreal forest at the spot where the Clearwater River flows into the Athabasca. Backyards in the residential neighbourhoods in the west and northwest run up against walls of pine and spruce. Forest fire is always a threat, but on Monday the smoke and flames appeared to be far enough away to allow for hope that the city was safe. On Tuesday, the worst happened. The winds came up and the wildfires flanked the city. The two oldest residential developments, Abasands and Beacon Hill, have been decimated. Thickwood, Timberlea and Parsons Creek, the newest and by far the largest residential developments, where there are modern schools and shopping malls and a beautiful ravine park, were on the verge of being overrun by the flames.

The destruction by fire of an entire Canadian city of more than 80,000 people is suddenly a possibility. Fort McMurray is a remarkable place. People from across Canada and the world have built lives there. In grocery stores, you’ll find halal meats displayed alongside cod tongues. Muslim and Christian children mix easily at the new Roman Catholic high school. Fort Mac is often maligned as a transient, wild west town and a symbol of oil extraction at all costs, but it is in fact a tolerant, diverse and progressive city – a very Canadian boomtown. Not perfect, but doing its best to be a durable home for oil sands workers in spite of the capriciousness of oil prices, the isolation and the long winters.

The focus now is on the logistics of caring for 89,000 evacuees – a staggering challenge. Government officials at all levels and in all provinces, along with private industry and the many native bands around Fort McMurray, are offering aid. Residents are safe and, miraculously, no one has been reported killed or injured. But many, or even perhaps all, may not have homes to return to.

Unseasonably hot weather in Alberta, Canada, is fueling the worst wildfire disaster in the country’s history. An extreme weather pattern, known as an omega block, is the source of the heat. An omega block is essentially a stoppage in the atmosphere’s flow in which a sprawling area of high pressure forms. This clog impedes the typical west-to-east progress of storms. The jet stream, along which storms track, is forced to flow around the blockage. At the heart of the block in Canadian’s western provinces, the air is sinking and much warmer than normal. Such a clog can persist for days until the atmosphere’s flow is able to break it down and flush it out.

Centers of storminess form on both sides of the block, and the resulting jet stream configuration takes on the likeness of the Greek letter omega. In this case, cool and unsettled weather is affecting the eastern Pacific Ocean and eastern North America, including much of the U.S. East Coast. As the Fort McMurray wildfire rapidly spread Tuesday, temperatures surged to 90 degrees (32 Celsius), shattering the daily record of 82 degrees set May 3, 1945. Dozens of other locations in Alberta also had record high temperatures. More records are likely to fall today. Temperatures are forecast to climb well into the 80s today at Fort McMurray, about 30 degrees warmer than normal. The average high is in the upper 50s.

A top United Nations official warned of a new tide of refugees from Syria if world powers didn’t succeed in calming an outbreak of hostilities in and around the northern Syrian city of Aleppo. Staffan de Mistura, the U.N.’s special envoy for Syria, said after meeting with European diplomats and Syrian opposition officials Wednesday that the priority in moving forward with a peace process for Syria was to stop the fighting around what was once Syria’s most populous city. “The alternative is truly quite catastrophic,” Mr. de Mistura said. “We could see 400,000 people moving toward the Turkish border.” The talks in Berlin centered on ways to return to talks in Geneva on Syria’s political future. The opposition’s High Negotiations Committee, headed by Riad Hijab, pulled out of those talks on April 18 as a cessation of hostilities agreed to in February disintegrated.

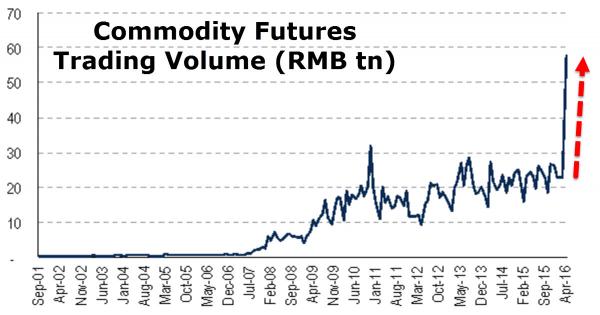

The credit-fueled speculative bubble in China’s commodity market, as we detailed previously, exploded this week as the mainstream slowly comes to realize that the gains in industrial metals are not a “sign of strength in China’s and the world’s economic recovery” but merely the next rotation of fast-money slooshing from Chinese equities to Chinese corporate bonds to Chinese real estate and now to Chinese commodity futures… Trading in futures on everything from steel reinforcement bars and hot-rolled coils to cotton and polyvinyl chloride has soared this week, prompting exchanges in Shanghai, Dalian and Zhengzhou to boost fees or issue warnings to investors. Deutsche Bank details the total crazinesss…

The onshore China commodity markets this week traded (conservatively) $350bn notional, a 17x increase on the $20bn notional that traded on Feb 1st 2016 i.e. a month ago (is it coincidence that the notional is about the same as at the peak of the equity frenzy?).

My calculations are pretty basic; I’ve trawled the screens and chosen 32 commodities in agri, metals and coke/coal and done a quick (contracts x value)/CNY for a dollar amount. I have not used the largest day’s volume either (e.g. Deformed Bar, RBTA has traded close to $100bn, but I used closer to $60bn). Cotton (VVA Comdty) has been trading $15bn, up from $500mm in Feb. In the US, the long established cotton contract (CT1 Comdty) trades $600mm. China listed Sugar (CBA Comdty) has traded $14bn versus the US listed sugar beet at $850mm.

Shopping is the national pastime. High streets, malls and retail parks have long been places people went for a day out, rather than on a mission to buy a particular item, and their spending helped lift the country out of recession. But a big drop in footfall – the number of people visiting high street and retail centres – over the past year has exposed fresh cracks in the high street, leaving retail chiefs wondering where all their customers have gone. Analysts are reporting declines in the number of shopper visits to high streets and shopping centres around the country of as much as 10% in some cities over the past year. Worries about the economic outlook, coupled with the rise of internet shopping, jitters about the EU referendum and more spending on eating out and leisure leave little cash left over for splurging in the shops.

“There is a lot of nervousness around [among retailers],” says Tim Denison, retail analyst at Ipsos Retail Performance. “People have had more disposable income but retailers have not been as successful as they could have been in taking their share. Instead any spare money has gone on leisure and holidays rather than pure retail spend.” According to Ipsos’s retail traffic index, overall footfall was down 0.9% in the first quarter of 2016 compared with the same period a year ago. But that headline masks the fact that some towns and cities are faring much worse than the national picture would suggest. The Ipsos data singles out Newcastle upon Tyne as the worst performer, with shopper numbers down a hefty 9.95% over the past year, closely followed by Stoke-on-Trent, down 8.1%. Other pockets of particular weakness were Chelmsford, Lincoln and Cambridge.

By comparison Ashford in Kent, Crawley in West Sussex and Epsom in Surrey were among the best-performing retail centres – the result, according to Denison, of wealth radiating out from London. Even in those towns, however, growth is not exactly rampant. Five of the top seven best-performing shopping centres were up less than 1% year on year. A number of retail chains have already blamed poor performance on declining numbers of shoppers. Poundland has pointed directly to the fact there are fewer people on the high street as a key reason behind its slowing sales. Last week value fashion retailer Primark revealed its first drop in UK underlying sales for 12 years, although boss George Weston said it was not yet time to press the panic button, given that chilly spring weather had weighed on all sales for all fashion retailers. “We need some warm weather and then we will know if there is a real problem on the high street,” he said.

“..the labor participation rate has fallen from a high of 67.3% in 2000 to 62.6% today. That 62.2% represents a 38-year low, which puts Bloomberg’s claim of a 42-year-low in joblessness in perspective.”

On Apr. 14, Bloomberg News announced that jobless claims in the US have reached their lowest level since 1973. “All other labor market data are telling us that the economy is creating a lot of jobs,” economist Patrick Newport told the outlet. “This is further confirmation that the labor market is strong.” That same day, thousands of fast food workers, airport workers, home care workers, and adjunct professors took to the streets across the country to protest brutal labor conditions and demand a $15 minimum wage. Most of these workers make far below $15 per hour. Some make as low as $7.25 per hour, the current federal minimum wage. Most lack benefits. Some, like adjunct professors, have contingent, temporary jobs, sometimes consisting of only one poorly paid course per year.

Many low-wage employees work two or even three jobs in an attempt to cobble together enough income to cover basic needs. According to the US Bureau of Labor, all of these workers are considered “employed.” They are viewed as part of the American economy’s success story, a big part of which is our 5% unemployment rate. As president Barack Obama boasted in February: “The United States of America right now has the strongest, most durable economy in the world.” Obama’s claims of a strong economy ring hollow for the many thousands of workers who say they cannot make enough to survive. But Obama’s claims of a strong economy ring hollow for the many thousands of workers—in professions ranging from those which require a GED to those which require a PhD—who say they cannot make enough money to survive.

And these people, at least, are working. Those who cannot find work at all tell an even grimmer story.] There are three main reasons the vaunted economic recovery still feels false to so many. The first is the labor participation rate, which plunged at the start of the Great Recession and discounts the millions of Americans who have been out of work for six months or more. The second is “the 1099 economy,” a term The New Republic’s David Dayen coined to refer to the soaring number of temps, contractors, freelancers, and other often involuntarily self-employed workers. The third is a surge in low-wage service jobs, coupled with a corresponding decrease in middle-class jobs.

Employment statistics in particular have a habit of eclipsing the real story. As any worker will tell you, it is not the number of jobs that matters most, but what kind of jobs are available, what they pay, and how that pay measures against the cost of living. The 5% unemployment rate, other words, is hiding the devastating story of underemployment, wage loss, and precariousness that defines life for millions of Americans. Since 2008, the labor participation rate has fallen from a high of 67.3% in 2000 to 62.6% today. That 62.2% represents a 38-year low, which puts Bloomberg’s claim of a 42-year-low in joblessness in perspective. The jobless number is “low” only because more people are no longer considered to be participating in the workforce.

“..the visage of an old age colony being hurtled toward the edge of a debt cliff by central bankers who have taken leave of their faculties does not bring the idea of economic recovery and growth immediately to mind.”

I mistakenly took Squawk Box off mute this morning. It was just in time to hear one of the regular anchors – the one who makes Joe Kernen sound slightly insightful by comparison – forecast a pick-up in global growth on the grounds that “China is recovering”. Yes, the credit intoxicated land of the Red Ponzi just tied one on for the record books. During Q1 it generated new debt at a madcap annual rate of $4 trillion or nearly 40% of GDP. And that incendiary deposit of more unpayable debt, which came on top of the $30 trillion already smothering history’s greatest construction site and open air gambling den, did indeed goose China’s real estate prices, state company CapEx, infrastructure building and steel production. Call it fiat growth because even pyramid building adds to stated GDP, at first.

Even then, the overwhelming share of this explosion of new credit went to pay interest on the existing mountain of IOUs. Charles Ponzi could never have imagined a scam so audacious. Nor are the red suzerains of Beijing unique in the headlong dash toward the financial cliff. Except for the nicety that Japan’s 30-year and 40-year bonds are trading at a microscopic fraction this side of zero (0.3%), Kuroda and his tiny band of mad men at the BOJ have driven the entirety of Japan’s monumental public debt – which is now actually measured in the quadrillions of yen – into the netherworld of negative yield. Needless to say, the visage of an old age colony being hurtled toward the edge of a debt cliff by central bankers who have taken leave of their faculties does not bring the idea of economic recovery and growth immediately to mind.

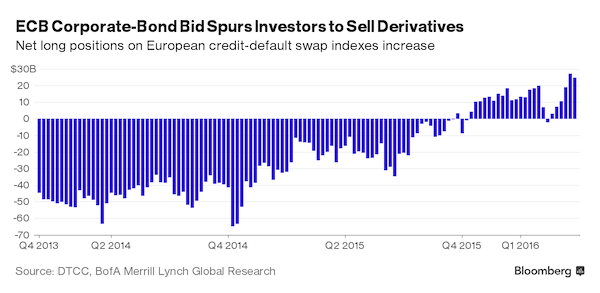

The same can be said for the ECB’s $90 billion per month bond buying bacchanalia. Having made German bunds so scarce as to have eviscerated any semblance of yield and turned Italy’s sovereign junk into super-bluechips, the ECB will soon be slurping up the corporate bonds of any global company that can fog a BBB credit breathalyzer and plant an SPV within the borders of the EU-19. What happens when Draghi is finally stopped and the Big Fat Bid of the ECB and its fast money front-runners disappears? The hopeful CNBC anchor-lady didn’t say. And about what happens if he isn’t stopped, she didn’t say, either.

The fact is, Simple Janet has already proven the end game. Money printing central bankers can’t stop. Were they to allow financial prices to normalize and trillions of bad credit to be liquidated, the whole financial house of cards they have built around the planet would blow sky high. The “soft landing” case is a null set.

“The sole purpose of this “sober and serious” text, there can be no doubt, was to produce one conclusion – an alarming headline “finding” which, however dubious, can be repeated again and again in the weeks to come, until it lodges in the public consciousness.”

Earlier this month, the government published a leaflet strongly urging us to vote “Remain” in the European Union – and sent it to all 27m UK households. Not only did the multi-million pound cost of producing and distributing this leaflet undermine the carefully-negotiated spending rules relating to the referendum on June 23, designed to stop the campaign becoming a money-driven free-for-all. The text itself was blatant propaganda – full of statistical sleights of hand disguised as reasoned arguments, a master-class in passive aggressive manipulation. It turns out, though, this tawdry leaflet was just the start when it comes to “Remain” using taxpayer cash and “the government machine” to bolster its cause.

For last week, Chancellor George Osborne launched a thumping 200-page “Treasury study” into the long-term implications of leaving the EU, which “forecast a £4,300 fall in GDP per household” if we leave. For many millions of voters, that’s a scary number – around a quarter of today’s average disposable income. Once again, this huge Treasury document represents a clear breach of long-standing rules that Whitehall remains detached from political campaigning, rules of particular relevance during a knife-edge referendum contest. And, reading through it, one is constantly stuck by the grotesque extent to which, for all the scientific pretence, the “analysis” is deliberately skewed.

The sole purpose of this “sober and serious” text, there can be no doubt, was to produce one conclusion – an alarming headline “finding” which, however dubious, can be repeated again and again in the weeks to come, until it lodges in the public consciousness. Rather than Her Majesty’s Treasury, this document could have been produced by Orwell’s Ministry of Truth. Unusually for a newspaper pundit, perhaps, I’m a trained economist. And in all my many years of studying official economic documents – budgets, comprehensive spending reviews and the like – through all that sifting and weighing of fine-print, I’ve never come across methodology and assumptions so blatantly rigged.

The euro zone needs negative interest rates to avoid sliding into deflation, ECB Governing Council member Ewald Nowotny said in an Austrian newspaper interview, defending the policy against widespread criticism in Germany. The ECB kept the cost of borrowing for banks at zero on Thursday and will continue to charge them 0.4% for parking money at the central bank. A slew of German politicians have complained in recent weeks that low interest rates are hurting savers. But Nowotny defended the policy. “You have to discuss negative rates in a broad context,” the head of the Austrian central bank was quoted as saying by the newspaper Der Standard on Saturday.

They are part of the central bank’s efforts to stabilize Europe’s economic situation after a severe crisis, he said. “Now it is all about preventing Europe from dropping into deflation.” He said that he would welcome it if interest rates could be raised again “the sooner the better”, but that the conditions must be right. “This will happen as soon as the economy is doing better, business activity picks up and inflation gets higher.” Countering the criticism of low interest rates, Draghi himself said on Thursday that some of it could be seen as endangering its independence, which could delay investment and hence prolong its current policies.

German Finance Minister Wolfgang Schaeuble said Greece doesn’t need debt relief now and won’t require an easing of its debt burden as long as the troika of creditors determines that debt sustainability is ensured. The European Stability Mechanism, the euro region’s financial backstop, will seek to lock in the favorable refinancing costs it’s passing on to Greece for an extended period of time, Schaeuble said in Amsterdam. While not part of the Greek program, these operations – if in place – would help ease pressure on Greece, he said. “The debt sustainability analysis determines whether measures are needed” to help the cash-strapped country, Schaeuble told reporters after a two-day meeting of EU finance ministers. “It is my conviction that this is not necessary for the coming years.”

Greece’s government bonds rose for a third day on Friday after euro-area finance ministers and the IMF signaled that a deal on the nation’s next bailout installment is in sight. Schaeuble said “we have no desire” to repeat the confrontation between Greece and its creditors from last summer. The nation’s government submitted a bill to parliament on Friday evening, overhauling the Greek pension system and raising income tax for middle and high earners. The bill, which also raises taxation on gambling and dividends, is part of a €5.4 billion belt-tightening package required by creditors for the conclusion of the bailout review. The government still has to negotiate with representatives of creditor institutions a set of contingency measures equal to 2% of Greek GDP, which will only be triggered if it fails to meet its budget targets. An agreement on the bailout package and the target for Greece to reach a primary surplus of 3.5% of GDP by 2018 “appear possible,” Schaeuble said.

[..] The European Council chose to forget or ignore that Juncker had long resisted attempts to improve banking transparency and improve cross-border taxation – which had given Luxembourg a particular competitive advantage over its neighbors. A lot now depends on the extent to which LuxLeaks and/or the Panama Papers erode Juncker’s defense that everything was legal and he was ignorant of any wrongdoing. If there was law-breaking, then the ex-prime minister is vulnerable to the charge that either he didn’t know what was going on and should have, or he knew what was going on and allowed it. He is vulnerable also to whispers that Luxembourg’s business and political community is so small and tightly knit that complete ignorance is implausible.

What is more difficult to guess – at this moment of shifting standards – is whether Juncker will be condemned for allowing practices in Luxembourg that though legal were morally questionable. (You do not have to be a tax lawyer to see that what Juncker calls “the logic of non-harmonization” was compounded by Luxembourg’s culture of secrecy/discretion, which meant that companies could keep secret their tax arrangements and individuals could hide their revenue.) It is entirely possible that the government leaders who put Juncker in place – and their successors – will stick to the view that bygones should be bygones and Juncker’s past policies should not affect his standing as Commission president.

But what I detect, in at least some parts of Europe, is a readiness to revisit the past and to apply the standards of the present — meaning that what was legally correct may yet be found morally unacceptable in the court of public opinion. Juncker may choose to argue that his Commission is at the vanguard of reform. But what if his past record embarrasses the likes of Margrethe Vestager, as she turns over tax rulings made by national authorities with multinational corporations? Or Jonathan Hill, as he advances his proposal for increasing the tax transparency rules applying to multinationals? Or Pierre Moscovici, arguing for measures against tax evasion and money-laundering? Is this a sinner who repents, an opportunist, or just a hypocrite?

Whether Juncker is credible will also be important in the context of the Commission’s attempt to enforce fiscal discipline in Greece (or anywhere else). How does the Commission argue for improving revenue collection while LuxLeaks and Panama Papers paint a picture of a Juncker-run Grand-Duchy promoting tax-avoidance?

EU finance ministers agreed on Saturday to discuss whether they can regain some control over a morass of EU budget rules by focusing mainly on an annual spending cap as the best measure of compliance. Years of changes and additions to EU rules, called the Stability and Growth Pact, have made meeting targets extremely complex, prompting an attempt to simplify them, European Commissioner Vice President Valdis Dombrovskis told a news conference after the meeting of EU finance ministers. “We did not discuss how to change the Pact, just how to choose the indicators to assess the compliance with the Pact,” Dutch Finance Minister Jeroen Dijsselbloem said.

The Dutch, who currently preside over the EU, proposed that the ministers consider using a single indicator with which to judge budgetary compliance, called the expenditure rule. It already exists in EU law as one indicator to be used to judge the fiscal performance of an EU country, but has so far been more in the background. The focus until now was on the development of the structural budget balance, a measure that strips off changes to budget revenue and expenditure stemming from the phase of the business cycle as well as all one-offs. Because the structural deficit is a complex and volatile indicator, the Dutch instead proposed putting more emphasis on the expenditure rule, which says a government cannot increase annual spending more than its medium-term potential growth rate.

“It is directly in the hands of finance ministers. It gives us more guidance in the process of designing the budget. It says in advance what you have to do, and you have the control in your hands,” Dijsselbloem said. He said that while the structural deficit, which is the key indicator mentioned in EU economic legislation, was a valuable theoretical concept, it could not be directly controlled by finance ministers. “There was general agreement that we need an indicator that takes out all the cyclical elements and one-offs but preferably it should be more stable and not change all the time, and we could put more emphasis on indicators that we can actually directly influence as finance ministers,” he said.

Dijsselbloem said EU deputy finance ministers would further work on what measurement to use to better assess compliance and the ministers would return to the discussion in the third quarter of 2016. The aim of the EU budget rules, created in 1997, is to keep nominal budget deficits below 3% of gross domestic product and public debt below 60%. But as the rules were revised in 2005, 2011 and 2013 to take account of economic and political realities and to incorporate intergovernmental treaties, they became more and more complex. “The sheer number of indicators in the current framework poses a massive challenge for the national implementation of the fiscal framework,” the Dutch presidency said in a paper prepared for the ministers’ meeting. “It contains targets, upper limits and benchmarks for the nominal balance, structural balance, expenditure growth and debt development,” the paper said.

The U.K. government has updated foreign travel advice, warning British citizens about risks visiting America’s Southern states. Specifically the new advice draws attention to potential difficulties for lesbians, gays, bisexuals and transgenders. “The U.S. is an extremely diverse society and attitudes towards LGBT people differ hugely across the country,” the U.K. Foreign Office website says. “LGBT travelers may be affected by legislation passed recently in the states of North Carolina and Mississippi,” it said. North Carolina and Mississippi have introduced laws that negatively affect people in the LGBT community. The North Carolina “bathroom” law is a statewide policy banning individuals from using public bathrooms that don’t correspond to their sex as stated on their birth certificate.

Celebrities including Bruce Springsteen, Ringo Starr and Pearl Jam have canceled concerts there in protest. And tech giant PayPal has canceled a large-scale investment plan after the legislation was rubber stamped. In Mississippi a “religious liberties” law will take effect in July. That legislation again blocks cities from allowing transgender people to use public bathrooms for the sex they identify as. It also aims to protect dozens of forms of businesses and services from being prosecuted if they refuse to serve LGBT people. A similar transgender “bathroom bill” in the Tennessee state failed Monday after it was withdrawn by its sponsor.

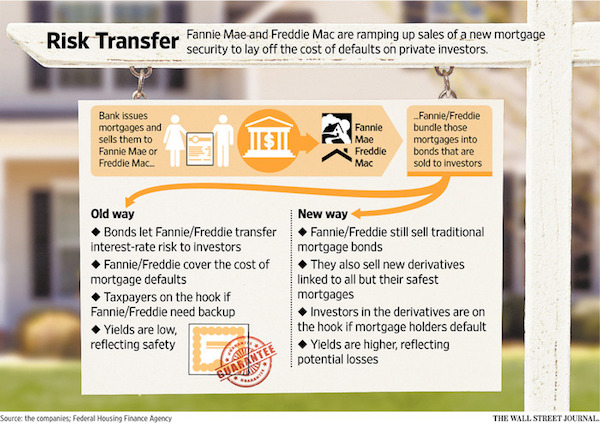

According to a study released by the Federal Reserve Bank of New York in March of last year, U.S. taxpayers have already injected $187.5 billion into Fannie Mae and Freddie Mac, two companies that prior to the 2008 financial crash traded on the New York Stock Exchange, had shareholders and their own Board of Directors while also receiving an implicit taxpayer guarantee on their debt. The U.S. government put the pair into conservatorship on September 6, 2008. The public has been led to believe that the $187.5 billion bailout of the pair was the full extent of the taxpayers’ tab. But in an astonishing acknowledgement on February 25 of this year, the Government Accountability Office, the nonpartisan investigative arm of Congress, issued an audit report of the U.S. government’s finances, revealing that the government’s “remaining contractual commitment to the GSEs, if needed, is $258.1 billion.”

This suggests that somehow, without the American public’s awareness, the U.S. government is on the hook to two failed companies for $445.6 billion dollars. And that may be just the tip of the iceberg of this story. The official narrative around the bailout of Fannie and Freddie is that they were loaded up with toxic subprime debt piled high by the Wall Street banks that sold them dodgy mortgages. While that is factually true, the other potentially more important part of this story is the counterparty exposure the Wall Street banks had to Fannie and Freddie’s derivatives if the firms had been allowed to fail.

The New York Fed’s staff report of March 2015 concedes the following: “Fannie Mae and Freddie Mac held large positions in interest rate derivatives for hedging. A disorderly failure of these firms would have caused serious disruptions for their derivative counterparties.” Exactly how big was this derivatives exposure and which Wall Street banks were being protected by the government takeover of these public-private partnerships that had spiraled out of control into gambling casinos? According to Fannie and Freddie’s regulator of 2003, OFHEO, “The notional amount of the combined financial derivatives outstanding of Fannie Mae and Freddie Mac increased from $72 billion at the end of 1993, the first year for which comparable data were reported, to $1.6 trillion at year-end 2001.”

An Australian politician has set fire to a river to draw attention to methane gas he says is seeping into the water due to fracking, with the dramatic video attracting more than two millions views. Greens MP Jeremy Buckingham used a kitchen lighter to ignite bubbles of methane in the Condamine River in Queensland, about 220 kilometres (140 miles) west of Brisbane. The video shows him jumping back in surprise, using an expletive as flames shoot up around the dinghy. “Unbelievable. A river on fire. Don’t let it burn the boat,” Buckingham, from New South Wales, said in the footage posted on Facebook on Friday evening, which has been viewed more than two million times. “Unbelievable, the most incredible thing I’ve seen. A tragedy in the Murray-Darling Basin (river system),” he said, blaming it on nearby coal-seam gas mining, or fracking.

Australia is a major gas exporter, but the controversial fracking industry has faced a public backlash in some parts of the country over fears about the environmental impact. Farmers and other landowners are concerned that fracking, an extraction method under which high-pressure water and chemicals are used to split rockbeds, could contaminate groundwater sources. The Murray-Darling Basin is a river network sprawling for one million square kilometres (400,000 square miles) across five Australian states. But the industry has said the practice is safe and that coal seam gas mining is a vital part of the energy mix as the world looks for cleaner fuel sources.