Vincenzo Camuccini La Morte Di Cesare 1804

We’re full speed ahead into absolute election mayhem, and nobody’s even thinking of pulling the brakes. Throw in a second and third corona wave, more lockdowns, more riots.

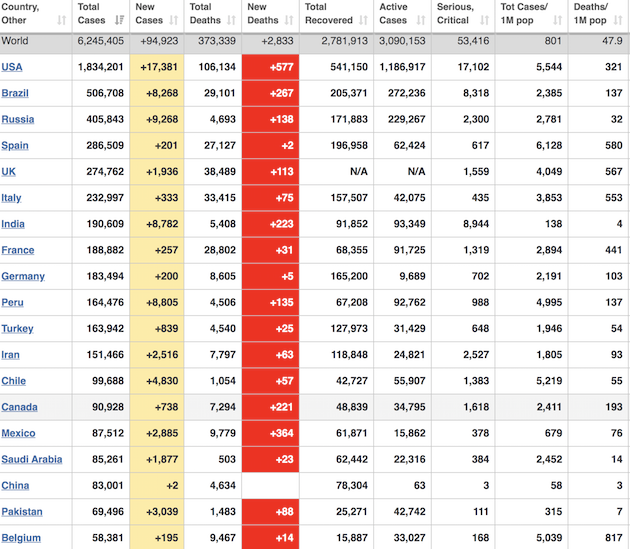

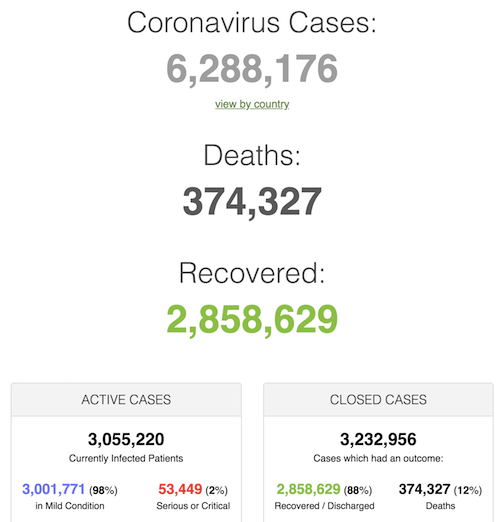

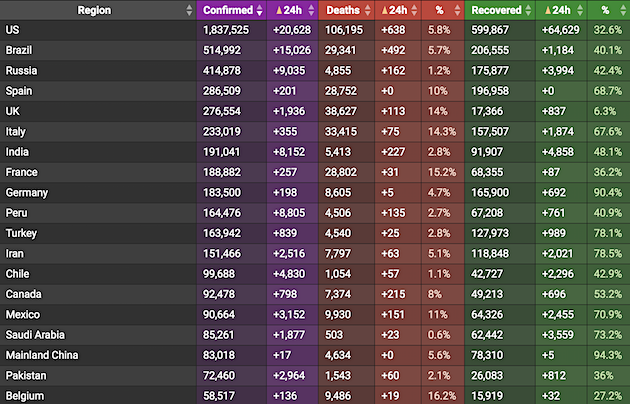

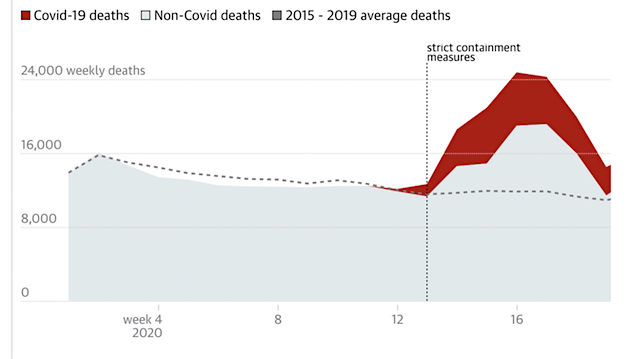

Today’s numbers gain in importance because of a model (see below) that predicts that before January 1, US total deaths will more than double to 410,000, and the world’s will triple to 2.8 million. A bold prediction.

I suggest you read this well. You’ll understand how this really works, and come away thinking you don’t understand a thing.

• Trump and Biden Could Face Dramatic Post-Election Battle (Yoo)

The Constitution requires the winner of the presidential election to garner a majority of the 538 votes in the Electoral College. Hillary Clinton won about 3 million more popular votes than Trump four years ago, but Trump won a clear Electoral College majority of 306-232. But if the election is close this year — as many prognosticators predict — and a few battleground states fail to report their votes on time, then neither President Trump nor former Vice President Biden might be able to assemble the required 270 electoral votes needed to become president. If such a stalemate occurs, a constitutional fail-safe would throw the election into the House of Representatives. Our nation barely avoided that outcome 20 years ago and has only used it twice in our history.

But even though the House will likely remain under Democratic control after the election, the Constitution’s process for resolving disputed elections should still bode well for Trump’s reelection. How could control of the White House end up in the domain of House Speaker Nancy Pelosi, D-Calif.? It depends on the decisions made 230 years ago. America’s founders rejected the idea that Congress should pick the president, which they believed would rob the chief executive of independence, responsibility and energy. They wanted the American people to have the primary hand in choosing the president. But the founders wanted the choice mediated through the states, because they also feared direct democracy.

In a compromise that binds us still, the founders allowed state legislatures to pick electors for the president, based on their number of senators and members of the House combined. The state-based organization of the Electoral College and its slight advantage for states with small populations (which receive two extra Electoral College votes no matter their population, since every state has two senators) underscore the founders’ desire to give federalism a say in the choice of the president. The founders went further in designing their constitutional backup. They realized that the Electoral College might yield no majority winner. They expected that regions might support their favorite sons instead.

In Article II of the Constitution, as modified by the 12th Amendment, the framers established that if no one won a majority of Electoral College votes, the House would pick the president from the top three vote-getters. But Pelosi and the Democrats — assuming that they hold onto their majority in the House — still won’t pick the president. Rather than allowing a simple majority vote in the House to select the president, the Constitution requires that the House choose the president by voting as state delegations. That means that California (represented by 53 House members) and Delaware (represented by 1 House member) would each get a single vote to pick the president. Once again, the founders decided to amplify the voice of the states in the presidential selection process, rather than defaulting to pure democracy.

And that is how Trump could win the presidency again. If the Electoral College votes yield no majority winner Dec. 14, the Constitution sends the vote to the House. Thanks to Republican advantages among the states, rather than the cities, the current balance of state delegations in the House favors Republicans, with 26 delegations controlled by Republicans and 23 controlled by Democrats (Pennsylvania is tied). If today’s House chose the president by voting by state delegations, Trump would win. But there is one more twist. The 20th Amendment to the Constitution seats a new Congress on Jan. 3, but does not begin the term of a new president until noon on Jan. 20. That means the new House chosen in the November election, rather than the current House, would choose the president if neither Trump nor Biden wins an Electoral College majority.

Even though Republicans currently have a majority of House delegations, Democrats have narrowed the gap. After the 2016 elections, Republicans had held a 32-17 advantage in House delegations. If Democrats can win one more congressional seat in Pennsylvania and then flip one more delegation, they could achieve a 25-25 tie in the House in January. Under this scenario, the election would require political bargaining of the most extreme kind for the House to resolve a disputed presidential election. But suppose the House can’t agree, which could well be likely given the polarization of our politics. The Constitution even provides for this. If the House splits 25-25 between Trump and Biden, then the 20th Amendment elevates the vice president-elect to the presidency. Under the 20th Amendment, when the Electoral College fails, the Senate chooses the vice president.

But unlike the House procedure, the senators each have an individual vote, meaning that under the current balance in the upper chamber, 53 Republicans would choose Mike Pence to effectively become the next president. But one-third of the seats in the Senate will be filled in the November election, meaning control of the chamber could flip to the Democrats. Under this scenario, Democratic vice presidential nominee Sen. Kamala Harris, D-Calif., could wind up as our next president and make history as the first woman to hold the office in American history. All of this is as complicated as it sounds. Election Day could be just the start of a new phase in a prolonged fight for control of the White House, rather than the conclusion of a long campaign.

Vaccination to start as early as October. What if it is a huge success, what will the west do?

• Russia COVID19 Vaccine Effective Against Any Dose Of Virus (RT)

The leader of the team behind Sputnik V said on Friday that the immune response documented among volunteers taking the world’s first registered coronavirus vaccine is sufficient to fight any level of Covid-19 infection. Alexander Gintsburg, head of Moscow’s Gamaleya Research Institute of Epidemiology and Microbiology, was speaking on the same day that The Lancet reported on trials confirming that every patient who received the vaccine had developed antibodies without any significant side-effects. The British publication, one of the oldest and best-respected medical journals in the world, confirmed that the Sputnik V vaccine had successfully produced antibodies in all 76 participants in early-stage trials.

“The vaccine’s immune response documented currently among volunteers is enough to counter any dose of Covid-19 that you could imagine,” Gintsburg said. Meanwhile, Moscow Mayor Sergey Sobyanin has revealed that post-registration clinical trials of Sputnik V in the capital could last from two to six months. He also confirmed that mass vaccination is likely to start in late 2020 or early 2021. “Some batches will arrive as early as this year,” he told Russia’s Channel One TV in an interview shown on Saturday. “There’s every likelihood that they will be used to vaccinate risk groups. These are healthcare, education, trade, the housing and utilities sectors, law enforcement agencies and some others – perhaps journalists.”

We need more models than just this one. But scary it is.

• Total COVID19 Deaths Projected To Double In US, Triple in World By Jan. 1 (R.)

U.S. deaths from the coronavirus will reach 410,000 by the end of the year, more than double the current death toll, and deaths could soar to 3,000 per day in December, the University of Washington’s health institute forecast on Friday. Deaths could be reduced by 30% if more Americans wore face masks as epidemiologists have advised, but mask-wearing is declining, the university’s Institute for Health Metrics and Evaluation said. The U.S. death rate projected by the IHME model, which has been cited by the White House Coronavirus Task Force, would more than triple the current death rate of some 850 per day.

“We expect the daily death rate in the United States, because of seasonality and declining vigilance of the public, to reach nearly 3,000 a day in December,” the institute, which bills itself as an independent research center, said in an update of its periodic forecasts. “Cumulative deaths expected by January 1 are 410,000; this is 225,000 deaths from now until the end of the year,” the institute said. It previously projected 317,697 deaths by Dec. 1. The model’s outlook for the world was even more dire, with deaths projected to triple to 2.8 million by Jan. 1, 2021.

Why have we been focusing on PCR as much as we have? It is so far from perfect it’s not funny anymore.

• PCR Tests ‘Could Be Picking Up Dead Coronavirus’ (BBC)

The main test used to diagnose coronavirus is so sensitive it could be picking up fragments of dead virus from old infections, scientists say. Most people are infectious only for about a week, but could test positive weeks afterwards. Researchers say this could be leading to an over-estimate of the current scale of the pandemic. But some experts say it is uncertain how a reliable test can be produced that doesn’t risk missing cases. Prof Carl Heneghan, one of the study’s authors, said instead of giving a “yes/no” result based on whether any virus is detected, tests should have a cut-off point so that very small amounts of virus do not trigger a positive result. He believes the detection of traces of old virus could partly explain why the number of cases is rising while hospital admissions remain stable.

[..] The PCR swab test – the standard diagnostic method – uses chemicals to amplify the virus’s genetic material so that it can be studied. Your test sample has to go through a number of “cycles” in the lab before enough virus is recovered. Just how many can indicate how much of the virus is there – whether it’s tiny fragments or lots of whole virus. This in turn appears to be linked to how likely the virus is to be infectious – tests that have to go through more cycles are less likely to reproduce when cultured in the lab. But when you take a coronavirus test, you get a “yes” or “no” answer. There is no indication of how much virus was in the sample, or how likely it is to be an active infection.

A person shedding a large amount of active virus, and a person with leftover fragments from an infection that’s already been cleared, would receive the same – positive – test result. But Prof Heneghan, the academic who spotted a quirk in how deaths were being recorded, which led Public Health England to reform its system, says evidence suggests coronavirus “infectivity appears to decline after about a week”. He added that while it would not be possible to check every test to see whether there was active virus, the likelihood of false positive results could be reduced if scientists could work out where the cut-off point should be. This could prevent people being given a positive result based on an old infection.

And Prof Heneghan said that would stop people quarantining or being contact-traced unnecessarily, and give a better understanding of the current scale of the pandemic. Public Health England agreed viral cultures were a useful way of assessing the results of coronavirus tests and said it had recently undertaken analysis along these lines. It said it was working with labs to reduce the risk of false positives, including looking at where the “cycle threshold”, or cut-off point, should be set. But it said there were many different test kits in use, with different thresholds and ways of being read, which made providing a range of cut-off points difficult.

Hear hear. It’s important to avoid unneeded pressure. Already, renewed lockdowns lead to a lot of protest. As predicted: you need to get the first one right, or trouble’s on the way.

• Italian Mayor Wants Penalties For Wearing A Face Mask When Unnecessary (RT)

These days, going out without wearing a face mask is considered poor form – and, in some places, an offense. But the mayor of an Italian town says fines should be slapped on those wearing a mask in an “inappropriate” situation. In the same way global health authorities insist masks contain the spread of coronavirus, Vittorio Sgarbi, the mayor of Sutri, is confident his unorthodox initiative will help stem the spread of “pandemic-related hysteria,” as he put it, according to the TASS news agency. The lingering Covid-19 pandemic has so far infected close to 275,000 people in Italy and killed more than 35,500 – almost seven times the entire population of Sutri. Yet, for Sgarbi, mandatory mask-wearing should have its limits, particularly when public safety is at stake.

Sgarbi, who is also a renowned art historian, cultural commentator, and television personality, told TASS he had issued a decree – yet to be approved by the Italian government – calling for imposition of a fine for wearing a mask in a situation when it’s not needed. “My decree has been issued under the current terrorism prevention laws,” he told the Russian media outlet. The legislation in question says people shouldn’t have their faces covered in a public place. Breaching this law can result in a one or two-year prison sentence or a fine of up to €2,000 (around $2,365). Sgarbi made it clear that anyone breaking his ban wouldn’t incur such a harsh penalty, but that people should wear a mask only when the occasion requires. “Wearing a mask at dinner is absurd,” he clarified. The mayor is no stranger to going against the mainstream. Ahead of the pandemic, he reportedly dismissed coronavirus as “a flu” and ridiculed those raising concerns about the looming crisis. He later made a formal apology when the death toll surged.

The story stinks.

• New Media Propaganda Tool: Use “Confirmed” to Mean its Opposite (Greenwald)

It seems the same misleading tactic is now driving the supremely dumb but all-consuming news cycle centered on whether President Trump, as first reported by the Atlantic’s editor-in-chief Jeffrey Goldberg, made disparaging comments about The Troops. Goldberg claims that “four people with firsthand knowledge of the discussion that day” — whom the magazine refuses to name because they fear “angry tweets” — told him that Trump made these comments. Trump, as well as former aides who were present that day (including Sarah Huckabee Sanders and John Bolton), deny that the report is accurate. So we have anonymous sources making claims on one side, and Trump and former aides (including Bolton, now a harsh Trump critic) insisting that the story is inaccurate.

Beyond deciding whether or not to believe Goldberg’s story based on what best advances one’s political interests, how can one resolve the factual dispute? If other media outlets could confirm the original claims from Goldberg, that would obviously be a significant advancement of the story. Other media outlets — including Associated Press and Fox News — now claim that they did exactly that: “confirmed” the Atlantic story. But if one looks at what they actually did, at what this “confirmation” consists of, it is the opposite of what that word would mean, or should mean, in any minimally responsible sense. AP, for instance, merely claims that “a senior Defense Department official with firsthand knowledge of events and a senior U.S. Marine Corps officer who was told about Trump’s comments confirmed some of the remarks to The Associated Press,” while Fox merely said “a former senior Trump administration official who was in France traveling with the president in November 2018 did confirm other details surrounding that trip.”

In other words, all that likely happened is that the same sources who claimed to Jeffrey Goldberg, with no evidence, that Trump said this went to other outlets and repeated the same claims — the same tactic that enabled MSNBC and CBS to claim they had “confirmed” the fundamentally false CNN story about Trump Jr. receiving advanced access to the WikiLeaks archive. Or perhaps it was different sources aligned with those original sources and sharing their agenda who repeated these claims. Given that none of the sources making these claims have the courage to identify themselves, due to their fear of mean tweets, it is impossible to know. But whatever happened, neither AP nor Fox obtained anything resembling “confirmation.”

They just heard the same assertions that Goldberg heard, likely from the same circles if not the same people, and are now abusing the term “confirmation” to mean “unproven assertions” or “unverifiable claims” (indeed, Fox now says that “two sources who were on the trip in question with Trump refuted the main thesis of The Atlantic’s reporting”). It should go without saying that none of this means that Trump did not utter these remarks or ones similar to them. He has made public statements in the past that are at least in the same universe as the ones reported by the Atlantic, and it is quite believable that he would have said something like this (though the absolute last person who should be trusted with anything, particularly interpreting claims from anonymous sources, is Jeffrey Goldberg, who has risen to one of the most important perches in journalism despite (or, more accurately because of) one of the most disgraceful and damaging records of spreading disinformation in service of the Pentagon and intelligence community’s agenda).

An across the board set-up. And yes, there will be more.

• The Stunning Synergy of The Atlantic’s Anonymous Attack on Trump (Pollak)

The Atlantic published a story Thursday evening that claimed President Donald Trump called the fallen American soldiers in a World War I cemetery “suckers” and “losers” in 2018. The author, Jeffrey Goldberg, cited four anonymous sources. Nearly a dozen current and former Trump administration officials disputed the story. One, notably, was John Bolton, the former national security adviser who says he will not vote for Trump. “I was there,” he said, and “I didn’t hear that.” Other claims in The Atlantic story are refuted by documentary evidence. The article claims, for instance, that Trump refused to visit the cemetery because the rain would ruin his hair. Bolton’s tell-all book said otherwise; so do official documents.

What is more interesting than the details of the story is how it was produced, and how it was rolled out. It has the appearance of a well-coordinated, well-executed campaign of disinformation, utilizing the full toolbox available to the Democratic Party. The article was published Thursday evening. By Friday morning, a left-wing group called Vote Vets had not only produced an ad based on the article, but had aired it on Morning Joe — MSNBC’s early-morning flagship news and opinion show. Meanwhile, the article spread across social media like a brush fire in a derecho. It trended at the top of Twitter; it was shared widely on Facebook, all without any of the “fact checks” that typically accompany disputed news reports on such platforms.

The Biden campaign issued a statement Thursday night — “If the revelations in today’s Atlantic article are true” — and held a press call Friday morning. The call featured, among others, Khizr Khan — the Gold Star father who attacked Trump in 2016. A short time later, Biden himself held a press briefing on the U.S. economy. Though he was expected to discuss the August jobs report — which came in better than expected, at 1.4 million jobs added — he led with an angry tirade about the article. At the end of his presentation, Biden turned to his campaign staff, who chose which reporters would be allowed to ask questions, and in what order. The first question went to Edward-Isaac Dovere, who writes for — surprise! — The Atlantic.

Dovere asked, “When you hear these remarks — ‘suckers,’ ‘losers,’ recoiling from amputees — what does it tell you about President Trump’s soul, and the life he leads?” It was a setup for Biden to attack Trump over The Atlantic allegations again. None of the other questions asked were challenging in any way; all appeared to be setup questions for Biden to attack Trump or to clarify some lingering problem — whether he had been tested for coronavirus (yes), where his running mate was (busy). No one asked Biden whether it was appropriate to attack Trump based on an unconfirmed report. No one even asked Biden about his economic policies.

What we witnessed Thursday night into Friday morning was the deployment of the Death Star — the full Democrat-media complex on display, coordinating journalists, outside political organizations, tech platforms, and unnamed military sources. It may be no coincidence that retired Gen. Stanley McChrystal — who was fired, ironically, because he had disparaged President Barack Obama and Biden — now advises a firm using military technology to help Democrats produce propaganda. It took weapons-grade skill to produce a story that, while unprovable, had the ring of truth to those eager to believe it (it “resonates,” said NBC’s Peter Alexander, whether it was true or not) and to make it the dominant story of the news cycle — on a day when the jobs market rebounded and Trump brokered a historic deal between Israel and Muslim-majority Kosovo.

Goldberg — the unofficial stenographer of the Obama White House — was just a vehicle. The real story is much bigger. The same machine that created and promoted The Atlantic piece will be sure to produce others.

He doubts Rosenstein frustrated the inquiry. Strzok has a book out, you’ll hear a lot about it soon. It argues there were tons of reasons for the inquiry.

• Strzok Joins Weissmann, Doubts NYT story on FBI’s Trump-Russia Inquiry (WE)

Controversial FBI agent Peter Strzok cast further doubt on a New York Times story that claimed the Justice Department secretly blocked special counsel Robert Mueller’s team from conducting a Trump-Russia counterintelligence investigation without informing the FBI. Strzok, who was a key member in the FBI’s investigation into both former Secretary of State Hillary Clinton’s improper private email server and Crossfire Hurricane’s Trump-Russia inquiry, said he “didn’t feel such a limitation” during his time on Mueller’s team when asked about a piece by New York Times reporter Michael Schmidt, whose article was adapted from his new book, Donald Trump v. The United States: Inside the Struggle to Stop a President.

Mueller’s “pitbull,” Andrew Weissmann, also cast doubt on the story a few days ago, and Mueller’s report and testimony also seem to contradict some claims made by the New York Times. “The Justice Department secretly took steps in 2017 to narrow the investigation into Russian election interference and any links to the Trump campaign, according to former law enforcement officials, keeping investigators from completing an examination of President Trump’s decades-long personal and business ties to Russia,” the New York Times reported on Sunday, adding the FBI opened the counterintelligence investigation in May 2017, but “within days,” former Deputy Attorney General Rod Rosenstein “curtailed the investigation without telling the bureau, all but ensuring it would go nowhere.”

Anne Applebaum of the Atlantic asked Strzok during an interview published Friday about the report, which she said, “suggests that the Justice Department secretly took steps in 2017 to narrow the investigation, precisely so that it would not touch on the president’s long-standing relationship with Russia.” Strzok cast doubt on that. “During the time I worked at the Special Counsel’s Office, I didn’t feel such a limitation,” Strzok replied. “When I discussed this with Mueller and others, it was agreed that FBI personnel attached to the Special Counsel’s Office would do the counterintelligence work, which necessarily included the president. But that’s an extraordinarily complex task, one of the most difficult counterintelligence investigations in the FBI’s history.”

Strzok added that “perhaps the FBI is somehow carrying out a comprehensive survey, with the full involvement of the CIA and NSA and the entire U.S. intelligence community” but said he worried that the inquiry “largely died on the vine.” Strzok was removed from Mueller’s team when numerous anti-Trump texts he’d exchanged with FBI lawyer Lisa Page, with whom he was having an affair, were unearthed, and he was fired in 2018. Strzok is currently suing the Justice Department. Weissmann also said the New York Times was wrong about its FBI counterintelligence story, tweeting, “NYT story today is wrong re: alleged secret DOJ order prohibiting a counterintelligence investigation by Mueller, ‘without telling the bureau.’ Dozens of FBI agents/analysts were embedded in Special Counsel’s Office and we were never told to keep anything from them.”

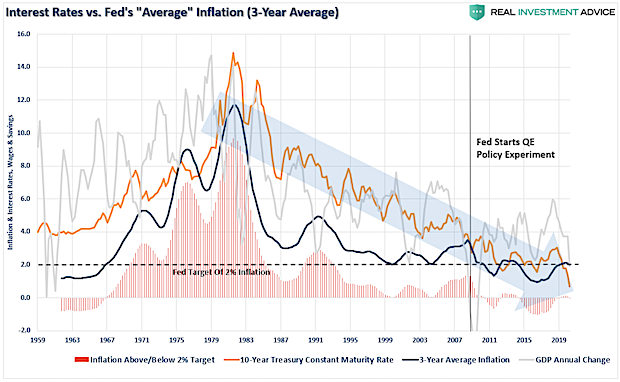

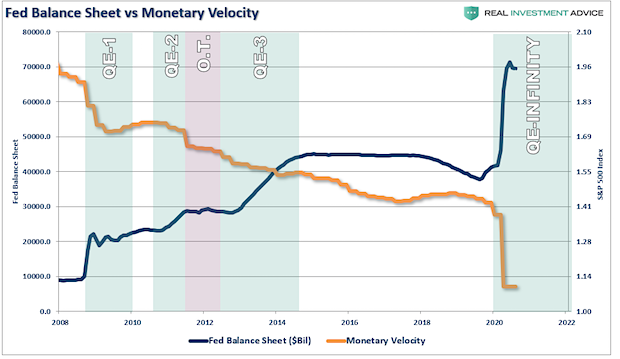

Lance Roberts lists 5 reasons why, I picked my per peeve: monetary velocity. That alone does the trick.

• 5 Reasons The Fed’s New Policy Won’t Get Inflation (Roberts)

What the Federal Reserve has failed to grasp is that monetary policy is “deflationary” when “debt” is required to fund it. How do we know this? Monetary velocity tells the story. What is “monetary velocity?” “The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia. With each monetary policy intervention, the velocity of money has slowed along with the breadth and strength of economic activity.

However, it isn’t just the expansion of the Fed’s balance sheet which is undermining the strength of the economy. It is also the ongoing suppression of interest rates to try and stimulate economic activity. In 2000, the Fed “crossed the Rubicon,” whereby lowering interest rates did not stimulate economic activity. Instead, the “debt burden” detracted from it.

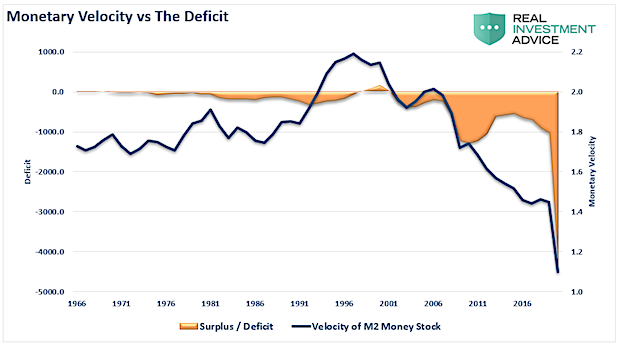

To illustrate the last point, we can compare monetary velocity to the deficit. To no surprise, monetary velocity increases when the deficit reverses to a surplus. Such allows revenues to move into productive investments rather than debt service. The problem for the Fed is the misunderstanding of the derivation of organic economic inflation.

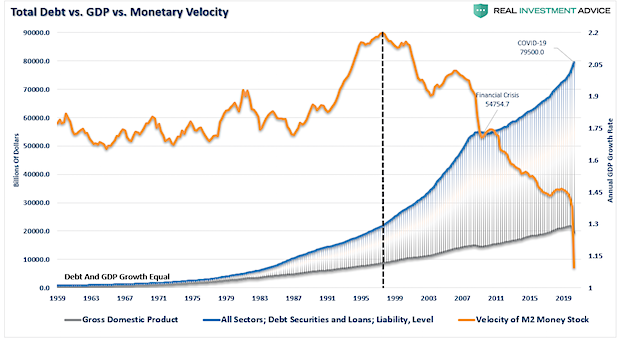

[..] in order to generate “real inflation,” economic growth must be strong enough to support employment that exceeds the rate of population growth. That employment must ALSO be productive (manufacturing based) employment which leads to higher wages. (Service jobs are deflationary as they go to the lower cost of labor.) Higher wages lead to increased consumption which allows producers to increase prices (inflation) over time. This has not been the case for nearly 40-years as technology continues to reduce the demand for labor by increasing productivity. This is the “dark side” of technology that no one wants to talk about. However, this cannot be achieved in an economy saddled by $75 Trillion in debt which diverts income from consumption to debt service. This is why “monetary velocity” began to decline as total debt passed the point of being “productive” to become “destructive.”

Virus, income and a few shut dorms.

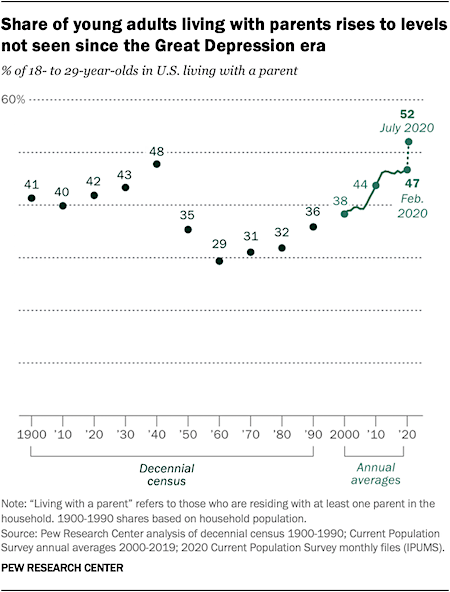

• Majority Of US Young Adults Live With Parents For The 1st Time In 80 Years (Pew)

In July, 52% of young adults resided with one or both of their parents, up from 47% in February, according to a new Pew Research Center analysis of monthly Census Bureau data. The number living with parents grew to 26.6 million, an increase of 2.6 million from February. The number and share of young adults living with their parents grew across the board for all major racial and ethnic groups, men and women, and metropolitan and rural residents, as well as in all four main census regions. Growth was sharpest for the youngest adults (ages 18 to 24) and for White young adults. The share of young adults living with their parents is higher than in any previous measurement (based on current surveys and decennial censuses).

Before 2020, the highest measured value was in the 1940 census at the end of the Great Depression, when 48% of young adults lived with their parents. The peak may have been higher during the worst of the Great Depression in the 1930s, but there is no data for that period. The share of young adults living with parents declined in the 1950 and 1960 censuses before rising again. The monthly share in the Current Population Survey has been above 50% since April of this year, reaching and maintaining this level for the first time since CPS data on young adults’ living arrangements became available in 1976.

Young adults have been particularly hard hit by this year’s pandemic and economic downturn, and have been more likely to move than other age groups, according to a Pew Research Center survey. About one-in-ten young adults (9%) say they relocated temporarily or permanently due to the coronavirus outbreak, and about the same share (10%) had somebody move into their household. Among all adults who moved due to the pandemic, 23% said the most important reason was because their college campus had closed, and 18% said it was due to job loss or other financial reasons.

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, your support is now an integral part of the process.

Thank you for your ongoing support.

Gettysburg Address. All of 272 words.

Support the Automatic Earth in virustime.