Reading the news on America should scare everyone, and every day, but it doesn’t. We’re immune, largely. Take this morning. The US Republican party can’t get its healthcare plan through the Senate. And they apparently don’t want to be seen working with the Democrats on a plan either. Or is that the other way around? You’d think if these people realize they were elected to represent the interests of their voters, they could get together and hammer out a single payer plan that is cheaper than anything they’ve managed so far. But they’re all in the pockets of so many sponsors and lobbyists they can’t really move anymore, or risk growing a conscience. Or a pair.

What we’re witnessing is the demise of the American political system, in real time. We just don’t know it. Actually, we’re witnessing the downfall of the entire western system. And it turns out the media are an integral part of that system. The reason we’re seeing it happen now is that although the narratives and memes emanating from both politics and the press point to economic recovery and a future full of hope and technological solutions to all our problems, people are not buying the memes anymore. And the people are right.

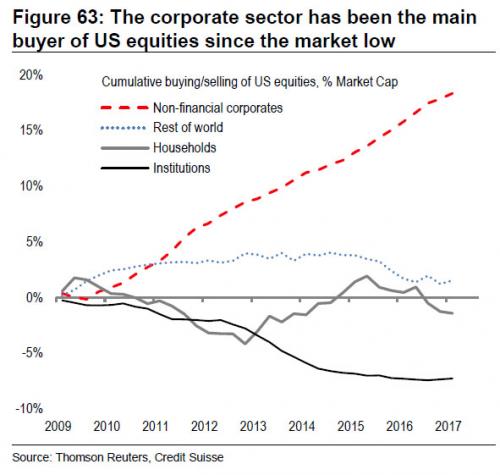

Tyler Durden ran a Credit Suisse graph overnight that should give everyone a heart attack, or something in that order. It shows that nobody’s buying stocks anymore, other than the companies who issue them. They use ultra-cheap leveraged loans to make it look like they’re doing fine. Instead of using the money/credit to invest in, well, anything, really. You can be a successful US/European company these days just by purchasing your own shares. How long for, you ask?

As CS’ strategist Andrew Garthwaite writes, “one of the major features of the US equity market since the low in 2009 is that the US corporate sector has bought 18% of market cap, while institutions have sold 7% of market cap.” What this means is that since the financial crisis, there has been only one buyer of stock: the companies themselves, who have engaged in the greatest debt-funded buyback spree in history.

Why this rush by companies to buyback their own stock, and in the process artificially boost their Earning per Share? There is one very simple reason: as Reuters explained some time ago, “Stock buybacks enrich the bosses even when business sags.” And since bond investor are rushing over themselves to fund these buyback plans with “yielding” paper at a time when central banks have eliminated risk, who is to fault them.

More concerning than the unprecedented coordinated buybacks, however, is not only the relentless selling by institutions, but the persistent unwillingness by “households” to put any new money into the market which suggests that the financial crisis has left an entire generation of investors scarred with “crash” PTSD, and no matter what the market does, they will simply not put any further capital at risk.

In other words, the system doesn’t only keep zombies alive, making it impossible for anyone to see who’s healthy or not, no, the system itself has become a zombie. The article mentions Blackrock’s Larry Fink talking about ‘cash on the sidelines’, but puhlease… Central banks have injected another $2 trillion into the zombie system this year alone, and that gives you that graph. Basically no-one supposedly on the sideline has a penny left.

So that’s your stock markets. Let’s call it bubble no.1. Another effect of ultra low rates has been the surge in housing bubbles across the western world and into China. But not everything looks as rosy as the voices claim who wish to insist there is no bubble in [inject favorite location] because of [inject rich Chinese]. You’d better get lots of those Chinese swimming in monopoly money over to your location, because your own younger people will not be buying. Says none other than the New York Fed.

College tuition hikes and the resulting increase in student debt burdens in recent years have caused a significant drop in homeownership among young Americans, according to new research by the Federal Reserve Bank of New York. The study is the first to quantify the impact of the recent and significant rise in college-related borrowing—student debt has doubled since 2009 to more than $1.4 trillion—on the decline in homeownership among Americans ages 28 to 30. The news has negative implications for local economies where debt loads have swelled and workers’ paychecks aren’t big enough to counter the impact. Homebuying typically leads to additional spending—on furniture, and gardening equipment, and repairs—so the drop is likely affecting the economy in other ways.

As much as 35% of the decline in young American homeownership from 2007 to 2015 is due to higher student debt loads, the researchers estimate. The study looked at all 28- to 30-year-olds, regardless of whether they pursued higher education, suggesting that the fall in homeownership among college-goers is likely even greater (close to half of young Americans never attend college). Had tuition stayed at 2001 levels, the New York Fed paper suggests, about 360,000 additional young Americans would’ve owned a home in 2015, bringing the total to roughly 2.9 million 28- to 30-year-old homeowners. The estimate doesn’t include younger or older millennials, who presumably have also been affected by rising tuition and greater student debt levels.

Young Americans -and Brits, Dutch etc.- get out of school with much higher debt levels than previous generations, but land in jobs that pay them much less. Ergo, at current price levels they can’t afford anything other than perhaps a tiny house. Which is fine in and of itself, but who’s going to buy the existent McMansions? Nobody but the Chinese. How many of them would you like to move in? And that’s not all. Another fine report from Lance Roberts, with more excellent graphs, puts the finger where it hurts, and then twists it around in the wound a bit more:

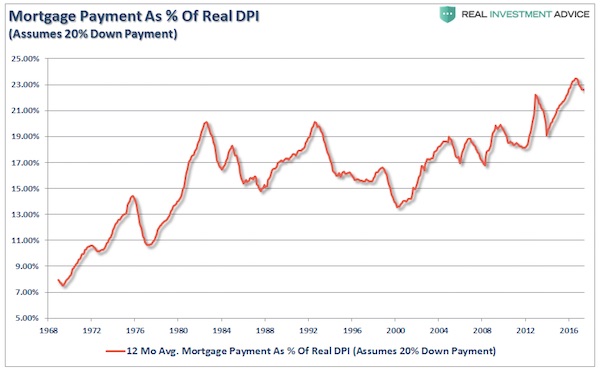

Over the last 30-years, a big driver of home prices has been the unabated decline of interest rates. When declining interest rates were combined with lax lending standards – home prices soared off the chart. No money down, ultra low interest rates and easy qualification gave individuals the ability to buy much more home for their money. The problem, however, is shown below. There is a LIMIT to how much the monthly payment can consume of a families disposable personal income.

In 1968 the average American family maintained a mortgage payment, as a percent of real disposable personal income (DPI), of about 7%. Back then, in order to buy a home, you were required to have skin in the game with a 20% down payment. Today, assuming that an individual puts down 20% for a house, their mortgage payment would consume more than 23% of real DPI. In reality, since many of the mortgages done over the last decade required little or no money down, that number is actually substantially higher. You get the point. With real disposable incomes stagnant, a rise in interest rates and inflation makes that 23% of the budget much harder to sustain.

In 1968 Americans paid 7% of their disposable income for a house. Today that’s 23%. That’s as scary as that first graph above on the stock markets. It’s hard to say where the eventual peak will be, but it should be clear that it can’t be too far off. And Yellen and Draghi and Carney are talking about raising those rates.

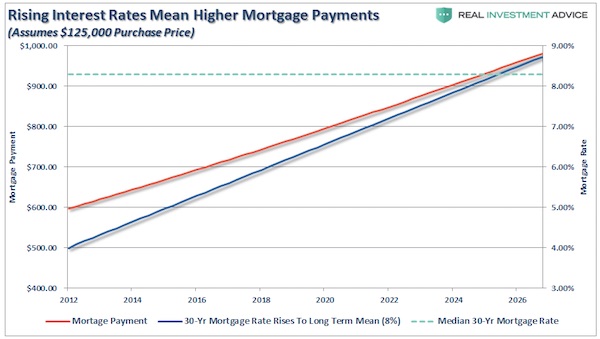

What Lance is warning for, as should be obvious, is that if rates would go up at this particular point in time, even a lot less people could afford a home. If you ask me, that would not be so bad, since they grossly overpay right now, they pay full-throttle bubble prices, but the effect could be monstrous. Because not only would a lot of people be left with a lot of mortgage debt, and we’d go through the whole jingle mail circus again, yada yada, but the economy’s main source of ‘money’ would come under great pressure.

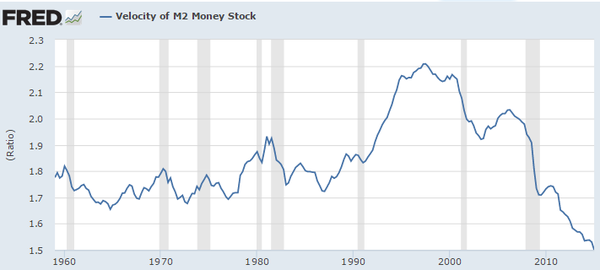

Don’t let’s forget that by far most of our ‘money’ is created when private banks issue loans to their customers with nothing but thin air and keyboard strokes. Mortgages are the largest of these loans. Sink the housing industry and what do you think will happen to the money supply? And since inflation is money velocity x money supply, what would become of central banks’ inflation targets? May I make a bold suggestion? Get someone a lot smarter than Janet Yellen into the Fed, on the double. Or, alternatively, audit and close the whole house of shame.

We’ve had bubbles 1, 2 and 3. Stocks, student debt and housing. Which, it turns out, interact, and a lot. An interaction that leads seamlessly to bubble 4: subprime car loans. Mind you, don’t stare too much at the size of the bubbles, of course stocks and housing are much bigger issues, but focus instead on how they work together. As for the subprime car loans, and the subprime used car loans, it’s the similarity to the subprime housing that stands out. Like we learned nothing. Like the US has no regulators at all.

It’s classic subprime: hasty loans, rapid defaults, and, at times, outright fraud. Only this isn’t the U.S. housing market circa 2007. It’s the U.S. auto industry circa 2017. A decade after the mortgage debacle, the financial industry has embraced another type of subprime debt: auto loans. And, like last time, the risks are spreading as they’re bundled into securities for investors worldwide. Subprime car loans have been around for ages, and no one is suggesting they’ll unleash the next crisis.

But since the Great Recession, business has exploded. In 2009, $2.5 billion of new subprime auto bonds were sold. In 2016, $26 billion were, topping average pre-crisis levels, according to Wells Fargo. Few things capture this phenomenon like the partnership between Fiat Chrysler and Banco Santander. [..] Santander recently vetted incomes on fewer than one out of every 10 loans packaged into $1 billion of bonds, according to Moody’s.

If it’s alright with you, we’ll deal with the other main bubble, no.5 if you will, another time. Yeah, that would be bonds. Sovereign, corporate, junk, you name it. The 4 bubbles we’ve seen so far are more than enough to create a huge crisis in America. Don’t want to scare you too much all at once. Just you read the news again tomorrow. There’ll be more. And the US Senate is not going to do a thing about it. They’re too busy not getting enough votes for other things.

We are constantly looking for new stocks by running stock screens, endlessly reading (blogs, research, magazines, newspapers), looking at holdings of investors we respect, talking to our large network of professional investors, attending conferences, scouring through ideas published on value investor networks, and finally, looking with frustration at our large (and growing) watch list of companies we’d like to buy at a significant margin of safety. The median stock on our watch list has to decline by about 35–40% to be an attractive buy. But maybe we’re too subjective. Instead of just asking you to take our word for it, in this letter, we’ll show you a few charts that not only demonstrate our point, but also show the magnitude of the stock market’s overvaluation and, more importantly, put it into historical context.

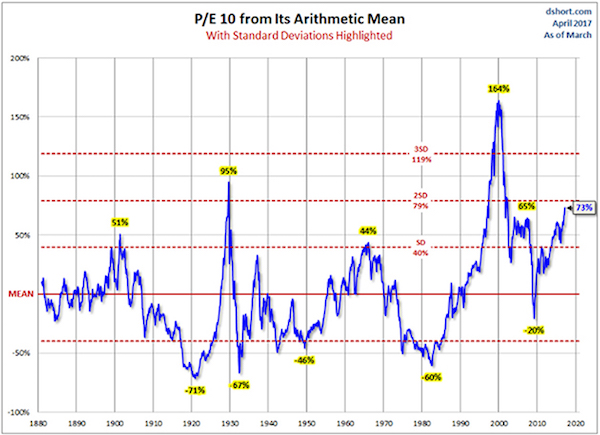

Each chart examines stock market valuation from a slightly differently perspective, but each arrives at the same conclusion: the average stock is overvalued somewhere between tremendously and enormously. If you don’t know whether “enormously” is greater than “tremendously” or vice versa, don’t worry, we don’t know either. But this is our point exactly: When an asset class is significantly overvalued and continues to get overvalued, quantifying its overvaluation brings little value. Let’s demonstrate this point by looking at a few charts. The first chart shows price-to-earnings of the S&P 500 in relation to its historical average. The average stock today is trading at 73% above its historical average valuation. There are only two other times in history that stocks were more expensive than they are today: just before the Great Depression hit and in the 1999 run-up to the dot-com bubble burst.

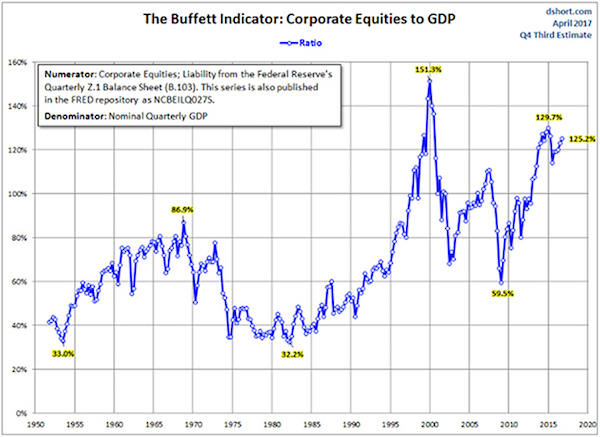

We know how the history played in both cases—consequently stocks declined, a lot. Based on over a century of history, we are fairly sure that, this time too, stock valuations will at some point mean revert and stock markets will decline. After all, price-to-earnings behaves like a pendulum that swings around the mean, and today that pendulum has swung far above the mean. What we don’t know is how this journey will look in the interim. Before the inevitable decline, will price-to-earnings revisit the pre-Great Depression level of 95% above average, or will it maybe say hello to the pre-dot-com crash level of 164% above average? Or will another injection of QE steroids send stocks valuations to new, never-before-seen highs? Nobody knows. One chart is not enough. Let’s take a look at another one called the Buffett Indicator. Think of this chart as a price-to-sales ratio for the whole economy, that is, the market value of all equities divided by GDP. The higher the price-to-sales ratio, the more expensive stocks are.

Total Household Wealth is exactly what it sounds like– the total net worth of every person in the United States, from Bill Gates down to the youngest newborn baby. So when you add up all the 330+ million folks in the Land of the Free and tally up their combined net worth, the total is $94 trillion. The thing is that the VAST majority of that wealth, especially the incredible growth over the last 8 years, has been from increases in just two asset classes: real estate and the stock market. In fact, stocks and real estate alone account for roughly 2/3 of the wealth increase since 2009. I’ll come back to that in a moment. Now, simultaneously, we see plenty of other interesting data, also published by the Federal Reserve and US federal government. Both the Fed and Census Bureau, for example, tell us that over 80% of businesses in the US are “nonemployer” companies, i.e. businesses which only employ one person (the owner), and often provide his/her primary source of income.

Yet according to the Federal Reserve, only 35% of these small businesses are profitable. Most are operating at a loss. In other words, only 35% of the companies which make up 80% of American businesses are profitable. You’re probably already doing the arithmetic– this means that a whopping 72% of all US businesses are NOT profitable. That hardly sounds like record wealth to me. Shifting gears, there’s the little factoid that an astounding 40% of young Americans are living with their parents– the highest%age in the last 75 years. And who can blame them considering student debt in the Land of the Free also hit a record $1.4 trillion three months ago, more than double the amount since the Great Recession. Speaking of record debt, US credit card debt passed a record $1 trillion, and total US consumer credit hit a record $3.8 trillion last month. Again, all of this hardly seems like ‘wealth’ to me.

Then there’s the issue of wages, which have remained essentially flat since the 2009 Great Recession if you adjust for inflation. According to the US Department of Labor, inflation-adjusted wages, aka “real hourly compensation” in the US fell an annualized 0.9% last quarter, and fell a dismal 5.6% in the previous quarter. Adjusted for inflation, the average American isn’t making any more money. Once again, this is a pitiful excuse for ‘wealth.’ American businesses aren’t more productive either. The same Labor Department report shows that productivity in the Land of the Free was flat in the first quarter of this year. And productivity actually declined in 2016– something that hasn’t happened in at least the last 50 years. Not to mention total economic growth in the Land of the Free has been pretty pitiful, logging a pathetic 1.6% last year. And GDP growth in the first quarter of 2017 was just 1.2% on an annualized basis. The US economy has exceed hasn’t surpassed 3% growth in more than 10-years.

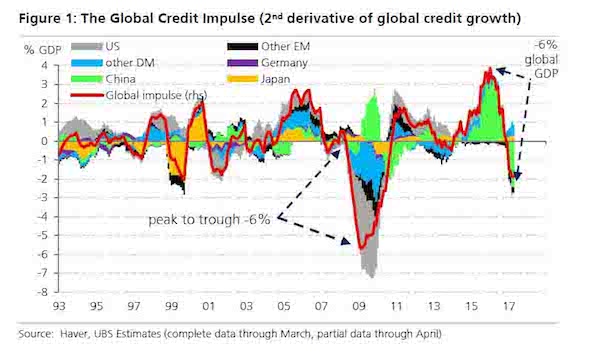

[..] fast forwarding just over three months later, where are we now? To answer that question, overnight UBS released its much anticipated update on the current state of the global credit impulse, and it’s nothing short of a disaster. As Kapteyn writes in what may have been the most eagerly awaited report in recent UBS history, “we have been inundated with questions about the chart below, first published in March. Yes, the global credit impulse is still falling. And yes, it matters because the correlation of this global credit impulse with global domestic demand is 0.61.” But it’s what follows next that should send shivers down the spine of anyone still clutching to the failed “recovery” narrative:

From peak to trough the deceleration in global credit growth is now approaching that during the global financial crisis (-6% of global GDP), even if the dispersion of the decline is much narrower. Currently 55% of the countries in our sample have experienced a -0.3 standard deviation deterioration in their credit impulse (median over 12 months) compared to 77% of countries in Dec ’09 when the median decline was -1.4 stdev.” Here is what the stunning collapse in the credit impulse looks like as of today:

While we urge all readers to get in touch with their friendly UBS sales coverage for the full report, here is a quick primer from UBS on what the current data is telling us, not so much about China where the credit impulse slowdown was discussed previously, but about the world’s biggest economy. From UBS: The credit impulse in the US has also turned down, seemingly on the back of a sharp drop in demand for C&I loans. The slowdown is more visible in the bank loan data than the Flow of Funds data we are using to calculate the credit impulse (the FoF is 3x as broad and includes non-bank credit as well). But the slowdown is nonetheless at odds with confidence being expressed about investment and future borrowing plans.

The US credit impulse was running at 0.7% GDP back in September 2016 and by March had fallen to -0.53% GDP (recovering somewhat in April based on bank loan data). Why does this matter? Because as UBS shows in the chart below, in the US the correlation between activity and the impulse is very strong, and the lack of credit growth could constrain an acceleration in GDP from weak Q1 levels (the credit impulse suggests domestic demand growth should be close to 1% rather than the 2+% which consensus is currently tracking).

The U.S. Federal Reserve is widely expected to raise its benchmark interest rate this week due to a tightening labor market and may also provide more detail on its plans to shrink the mammoth bond portfolio it amassed to nurse the economic recovery. The central bank is scheduled to release its decision at 2 p.m EDT on Wednesday at the conclusion of its two-day policy meeting. Fed Chair Janet Yellen is due to hold a press conference at 2:30 pm EDT. “The expectation of a rate hike…is widely held, and has been reinforced by the most recent round of Fed communications,” said Michael Feroli, an economist with J.P. Morgan. Economists polled by Reuters overwhelmingly see the Fed raising its benchmark rate to a target range of 1.00 to 1.25% this week.

The Fed embarked on its first tightening cycle in more than a decade in December 2015. A quarter%age point interest rate rise on Wednesday would be the second nudge upwards this year following a similar move in March. Since then, the unemployment rate has fallen to a 16-year low of 4.3% and economic growth appears to have reaccelerated following a lackluster first quarter. However, other indicators of the economy’s health have been more mixed. The Fed’s preferred measure of underlying inflation has retreated to 1.5% from 1.8% earlier in 2017 and investors are growing increasingly doubtful policymakers will be able to stick to their anticipated pace of tightening of three interest rate rises this year and next.

Firms that clear euro-denominated derivatives may be forced to relocate to the European Union from London after Brexit under EU proposals to be rolled out on Tuesday, according to a person with knowledge of the matter. Under the European Commission’s plans for overhauling supervision of clearinghouses that are based outside the bloc, firms deemed systemically important to the EU financial system could be required to accept direct oversight by the bloc’s authorities, the person said, asking not to be named because the proposals aren’t yet public. Firms could also be forced to move their euro clearing operations to a location inside the EU, the person said.

This so-called location requirement has spurred warnings from the industry of skyrocketing costs, and has helped to turn clearing into a political football as the EU and U.K. prepare for divorce negotiations. In a June 8 letter to Valdis Dombrovskis, the EU’s financial-services policy chief, the International Swaps and Derivatives Association said a survey of data from 11 banks showed that requiring euro-denominated interest-rate derivatives to be cleared by an EU-based clearinghouse would boost initial margin by as much as 20%. The proposals to be published on Tuesday are largely in line with initial plans floated last month by the commission, the EU’s executive arm.

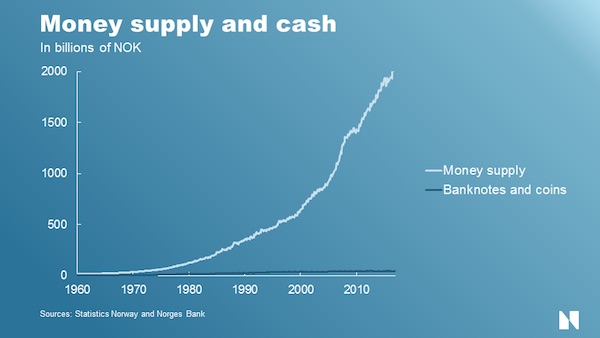

Today, there are two forms of central bank money. One of the forms is common knowledge – banknotes and coins. The other, bank reserves at Norges Bank, is less well known. The sum total of banknotes and coins and bank reserves at Norges Bank is about NOK 85 billion.[5] But the total money supply is much larger than this. Customer deposits in banks are also money. These deposits, referred to as deposit money, total more than NOK 2 trillion in Norway. This money is created by banks, not by Norges Bank. Chart 1 shows the money supply and the supply of banknotes and coins in Norway since 1960. In Norway, the money supply mainly comprises deposit money in banks.[6] In the early 1960s, banknotes and coins accounted for a fifth of the money supply. Current accounts and cheques were already becoming commonplace.

Since then, banks’ deposit money has increased dramatically, and today, banknotes and coins make up less than 2.5% of the money supply. In other words, virtually all the money we use has been created by banks. So how do banks create money? The answer to that question comes as quite a surprise to most people. When you borrow from a bank, the bank credits your bank account. The deposit – the money – is created by the bank the moment it issues the loan. The bank does not transfer the money from someone else’s bank account or from a vault full of money. The money lent to you by the bank has been created by the bank itself – out of nothing: fiat – let it become. The money created by the bank does not disappear when it leaves your account. If you use it to make a payment, it is just transferred to the recipient’s account.

The money is only removed from circulation when someone uses their deposits to repay a bank, as when we make a loan repayment.[7] The money supply is therefore only reduced when banks’ claims on the rest of the economy decrease. Banks also fund lending by raising loans themselves instead of creating money in the form of deposits. In order to reduce risk, banks also use other forms of investment in addition to lending.[8] Nevertheless, the money supply is growing at almost at the same pace as total bank credit. To sum up: banks create money out of nothing and withdraw it when loans are repaid. Growth in total bank credit is normally matched by growth in the money supply.[9] This does not sound encouraging. Is money an illusion? Why is today’s privately issued deposit money often perceived to be as safe as money issued by the central bank?

Call it the biggest bovine airlift in history. The showdown between Qatar and its neighbors has disrupted trade, split families and threatened to alter long-standing geopolitical alliances. It’s also prompted one Qatari businessman to fly 4,000 cows to the Gulf desert in an act of resistance and opportunity to fill the void left by a collapse in the supply of fresh milk. It will take as many as 60 flights for Qatar Airways to deliver the 590-kilogram beasts that Moutaz Al Khayyat, chairman of Power International Holding, bought in Australia and the U.S. “This is the time to work for Qatar,” he said. Led by Saudi Arabia, Qatar stands accused of supporting Islamic militants, charges the sheikhdom has repeatedly denied.

The isolation that started on June 5 has forced the world’s richest country by capita to open new trade routes to import food, building materials and equipment for its natural gas industry. The central bank said domestic and international transactions were running normally. Turkish dairy goods have been flown in, and Iranian fruit and vegetables are on the way. There’s also a campaign to buy home-grown produce. Signs with colors of the Qatari flag have been placed next to dairy products in stores. One sign dangling from the ceiling said: “Together for the support of local products.” “It’s a message of defiance, that we don’t need others,” said Umm Issa, 40, a government employee perusing the shelves of a supermarket before taking a carton of Turkish milk to try. “Our government has made sure we have no shortages and we are grateful for that. We have no fear. No one will die of hunger.”

“..they had no idea what to do about it, except maybe try to escape the moment-by-moment pain of their ruined lives with powerful drugs. And then, a champion presented himself..”

As our politicos creep deeper into a legalistic wilderness hunting for phantoms of Russian collusion, nobody pays attention to the most dangerous force in American life: the unraveling financialization of the economy. Financialization is what happens when the people-in-charge “create” colossal sums of “money” out of nothing — by issuing loans, a.k.a. debt — and then cream off stupendous profits from the asset bubbles, interest rate arbitrages, and other opportunities for swindling that the artificial wealth presents. It was a kind of magic trick that produced monuments of concentrated personal wealth for a few and left the rest of the population drowning in obligations from a stolen future. The future is now upon us. Financialization expressed itself in other interesting ways, for instance the amazing renovation of New York City (Brooklyn especially).

It didn’t happen just because Generation X was repulsed by the boring suburbs it grew up in and longed for a life of artisanal cocktails. It happened because financialization concentrated immense wealth geographically in the very few places where its activities took place — not just New York but San Francisco, Washington, and Boston — and could support luxuries like craft food and brews. Quite a bit of that wealth was extracted from asset-stripping the rest of America where financialization was absent, kind of a national distress sale of the fly-over places and the people in them. That dynamic, of course, produced the phenomenon of President Donald Trump, the distilled essence of all the economic distress “out there” and the rage it entailed.

The people of Ohio, Indiana, and Wisconsin were left holding a big bag of nothing and they certainly noticed what had been done to them, though they had no idea what to do about it, except maybe try to escape the moment-by-moment pain of their ruined lives with powerful drugs. And then, a champion presented himself, and promised to bring back the dimly remembered wonder years of post-war well-being — even though the world had changed utterly — and the poor suckers fell for it. Not to mention the fact that his opponent — the avaricious Hillary, with her hundreds of millions in ill-gotten wealth — was a very avatar of the financialization that had turned their lives to shit. And then the woman called them “a basket of deplorables” for noticing what had happened to them.

The Global Seed Vault, built in the Arctic as an impregnable deep freeze for the world’s most precious food seeds, is to undergo a multi-million dollar upgrade after water from melting permafrost flooded its access tunnel. No seeds were damaged but the incident undermined the original belief that the vault would be a “failsafe” facility, securing the world’s food supply forever. Now the Norwegian government, which owns the vault, has committed $4.4m (NOK37m) to improvements. The vault is buried 130m inside a mountain in the Svalbard archipelago and contains almost a million packets of seeds, each a variety of an important food crop. The vault was opened in 2008, sunk deep into the permafrost, and was expected to provide protection against “the challenge of natural or man-made disasters” and “to stand the test of time”.

But the vault’s planners had not anticipated the extreme warm weather seen recently at the end of the world’s hottest ever recorded year. “The background to the technical improvements is that the permafrost has not established itself as planned,” said a government statement. “A group will investigate potential solutions to counter the increased water volumes resulting from a wetter and warmer climate on Svalbard.” One option could be to replace the access tunnel, which slopes down towards the vault’s main door, carrying water towards the seeds. A new upward sloping tunnel would take water away from the vault.

A former Svalbard coal miner, Arne Kristoffersen, told the Guardian most coal mines on the islands had upward sloping entrance tunnels: “For me it is obvious to build an entrance tunnel upwards, so the water can run out. I am really surprised they made such a stupid construction.” Hege Njaa Aschim, the Norwegian government’s spokeswoman for the vault, said: “The construction was planned like that because it was practical as a way to go inside and it should not be a problem because of the permafrost keeping it safe. But we see now, when the permafrost is not established, maybe we should do something else with the tunnel, so that is why we have this project now.”

The European Union’s executive will decide on Tuesday to open legal cases against three eastern members for failing to take in asylum-seekers to relieve states on the front lines of the bloc’s migration crisis, sources said. The European Commission would agree at a regular meeting to send so-called letters of formal notice to Poland and Hungary, three diplomats and EU officials told Reuters. Two others said the Czech Republic was also on the list. This would mark a sharp escalation of the internal EU disputes over migration. Such letters are the first step in the so-called infringement procedures the Commission can open against EU states for failing to meet their legal obligations. The eastern allies Poland and Hungary have vowed not to budge. Their staunch opposition to accepting asylum-seekers, and criticism of Brussels for trying to enforce the scheme, are popular among their nationalist-minded, eurosceptic voters.

Speaking in Hungary’s parliament earlier on Monday, Prime Minister Viktor Orban said: “We will not give in to blackmail from Brussels and we reject the mandatory relocation quota.” A spokeswoman in Brussels did not confirm or deny the executive would go ahead with the legal cases, but referred to an interview that Commission head Jean-Claude Juncker gave to the German weekly Der Spiegel last week. “Those that do not take part have to assume that they will be faced with infringement procedures,” he was quoted as saying. Poland and Hungary have refused to take in a single person under a plan agreed in 2015 to relocate 160,000 asylum-seekers from Italy and Greece, which had been overwhelmed by mass influx of people from the Middle East and Africa. Poland’s Interior Minister Mariusz Blaszczak was quoted as saying on Monday by the state news agency PAP: “We believe that the relocation methods attract more waves of immigration to Europe, they are ineffective.”

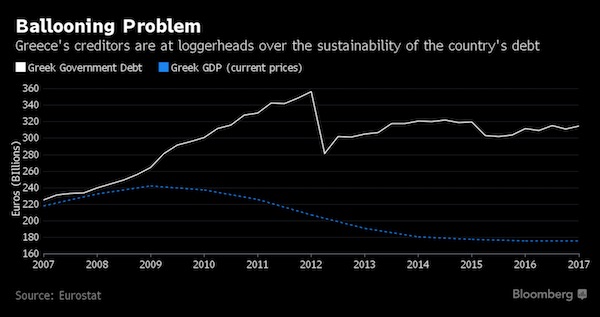

The ECB is unlikely to include Greek bonds in its asset-purchase program for the foreseeable future, a person familiar with the matter said, as European creditors aren’t prepared to offer substantially easier repayment terms on bailout loans to improve the nation’s debt outlook. Euro-area finance ministers will meet in Luxembourg on June 15 to discuss debt-relief measures that the ECB has said are needed before it will consider purchasing Greek bonds. The so-called Eurogroup is expected to complete a review of Athens’s rescue program that would allow for the disbursement of at least €7.4 billion in aid needed for a similar amount of bond repayments in July. An agreement among the ministers will likely allow the IMF – whose participation in the rescue program is a requirement for many nations – to commit in principle to a conditional loan, said the person.

But the extent and wording of debt-relief commitments probably won’t convince the Governing Council of the ECB to buy Greek bonds. And while the government of Prime Minister Alexis Tsipras is relying on quantitative easing to aid Greece’s return to the public debt market, the ECB won’t factor fiscal consequences into its policy-making decisions and excessive emphasis on QE inclusion would be misguided, according to the person. [..] The ECB’s quantitative easing is scheduled to continue until December 2017, with economists saying purchases will be gradually tapered throughout 2018. This would leave little time for purchases of Greek bonds before the program’s end.

Meanwhile, France, which is trying to bridge differences on the debt issue, has proposed automatically reducing loan repayments when Greece misses growth targets, according to two people with knowledge of the talks. European officials see the proposal as a step in the right direction but doubt it will be enough to convince the ECB to include Greece in its bond purchase program if the IMF maintains its position that the country’s debt is unsustainable. Other euro-area member states so far have opposed France’s proposal, the people said.

A deal on debt relief for Greece is “not far,” France’s new finance minister Bruno Le Maire said Monday ahead of crunch eurozone talks on the issue on Thursday. “I am optimistic that we will have a good solution. We are not far from agreement,” Le Maire said ahead of a meeting with Greek PM Alexis Tsipras. “We are really doing our best to find an agreement,” he had said earlier after seeing his Greek counterpart Euclid Tsakalotos. “It’s difficult. It’s complicated,” he said. At the June 15 meeting, Le Maire said he planned to propose a “mechanism” of “flexibility” to lessen Greek debt repayment based on its economic growth. “It’s a mechanism which should allow us to revise certain (debt) parameters based on Greek growth,” he told reporters.

The issue of debt relief for Greece has sharply divided its international creditors, the EU and the IMF, for months in the latest round of talks. The impasse has held up a tranche of bailout cash which Greece needs to repay loans in July, and Athens says its fragile recovery has also been impaired. Tsipras has said he will ask EU leaders to resolve the issue at the end of June if no solution is forthcoming on Thursday. “Piling drama on the problem helps no one,” he said on Monday. The Europeans expect Greece’s economy to grow strongly and its government to bring in large surpluses in revenue in the coming years, allowing it to pay down its debts. But the IMF is less optimistic, arguing there must be further relief for Athens before it can label its debt sustainable and justify loaning Greece any more cash.

New French President Emmanuel Macron last month called Tsipras after his election, saying he was in favour of “finding a deal soon to alleviate the weight of Greece’s debt over time.” Macron’s position puts him at odds with Germany where Greek debt relief – following three different bailouts with public money for the country since 2010 – is seen as a vote loser ahead of general elections in September. Macron explained his thinking about Greece in an interview to the Mediapart website two days before his election. “I am in principle in favour of a concerted restructuring of Greek debt and in keeping Greece in the eurozone. Why? Because the current system is unsustainable,” he said.

A woman died and 10 people were hurt on Monday when a 6.3-magnitude earthquake struck the Greek islands of Lesbos and Chios and the Aegean coast of western Turkey, officials said. The middle-aged victim had been trapped for around seven hours in the ruins of her home in the Lesbos village of Vrisa, the area that bore the brunt of the strong quake and where several homes collapsed. “Our fellow citizen who was trapped in the house that collapsed in Vrisa was pulled out dead,” Lesbos mayor Spyros Galinos said in a tweet. The earthquake also struck the Aegean coast of western Turkey after 1200 GMT.

Video footage shot by a Vrisa resident on a cellphone showed masonry from several single and two-level homes clogging the streets. “It’s a difficult situation, we are facing a disaster,” Christiana Kalogirou, governor of the north Aegean region, told Greek state TV station ERT, adding: “Some 10 people are injured.” “The army is bringing in tents so people can spend the night,” she said, adding that the south of Lesbos had taken the brunt of the quake. The tremor, felt as far as Athens and Izmir in Turkey, damaged at least three churches and shops in south Lesbos, local owners said, while rock slides blocked some roads.

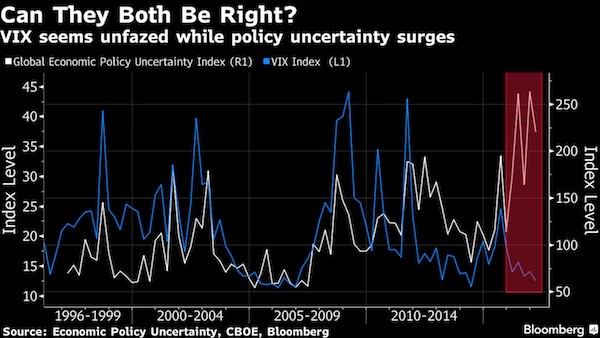

The last time Robert Shiller heard stock-market investors talk like this in 2000, it didn’t end well for the bulls. Back then, the Nobel Prize-winning economist says, traders were captivated by a “new era story” of technological transformation: The Internet had re-defined American business and made traditional gauges of equity-market value obsolete. Today, the game changer everyone’s buzzing about is political: Donald Trump and his bold plans to slash regulations, cut taxes and turbocharge economic growth with a trillion-dollar infrastructure boom. “They’re both revolutionary eras,” says Shiller, who’s famous for his warnings about the dot-com mania and housing-market excesses that led to the global financial crisis. “This time a ‘Great Leader’ has appeared. The idea is, everything is different.”

For Shiller, the power of a new-era narrative helps answer one of the most hotly debated questions on Wall Street as stocks set one high after another this year: Why are traders so fixated on the upsides of a Trump presidency when the downside risks seem just as big? For all his pro-business promises, the former reality TV star’s confrontational foreign policy and haphazard management style have bred uncertainty – the one thing investors are supposed to hate most. Charts illustrating the conundrum have been making the rounds on trading floors. One, called “the most worrying chart we know” by SocGen at the end of last year, shows a surging index of global economic policy uncertainty severing its historical link with credit spreads, which have declined in recent months along with other measures of investor fear. The VIX index, a popular gauge of anxiety in the U.S. stock market, has dropped more than 30 percent since Trump’s election.

[..] For Hersh Shefrin, a finance professor at Santa Clara University and author of a 2007 book on the role of psychology in markets, the rally is just another example of investors’ remarkable penchant for tunnel vision. Shefrin has a favorite analogy to illustrate his point: the great tulip-mania of 17th century Holland. Even the most casual students of financial history are familiar with the frenzy, during which a rare tulip bulb was worth enough money to buy a mansion. What often gets overlooked, though, is that the mania happened during an outbreak of bubonic plague. “People were dying left and right,” Shefrin says. “So here you have financial markets sending signals completely at odds with the social mood of the time, with the degree of fear at the time.”

Shiller says when markets are as buoyant as they are now, resisting the urge to pile in is hard regardless of what else might be happening in society. “I was tempted to do it, too,” he says. “Trump keeps talking about a new spirit for America and so you could (A) believe that or (B) you could believe that other investors believe that.” On whether stocks are nearing a top, Shiller can’t say with any certainty. He’s loathe to make short-term forecasts. Despite the well-timed publication of his book “Irrational Exuberance” just as the dot-com bubble peaked in early 2000, the Yale University economist had warned (with caveats) that shares might be overvalued as early as 1996. Investors who bought and held an S&P 500 fund in the middle of that year made about 8 percent annually over the next decade, while those who invested at the start of 2000 lost money. The index sank 49 percent from its high in March 2000 through a bottom in October 2002.

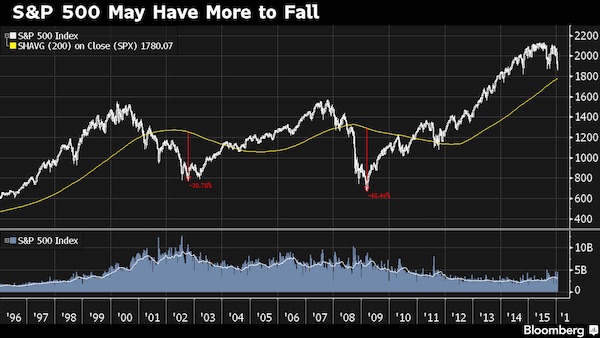

This is the most dangerous and overvalued stock market on record — worse than 2007, worse than 2000, even worse than 1929. Or so warns Wall Street soothsayer John Hussman in his scariest jeremiad yet. “Presently, we observe the broadest market valuation extreme in history,” writes the chairman of the cautious Hussman Funds investment group, “with the steepest median valuations on record, and the most reliable capitalization-weighted measures within a few percent of their 2000 peaks.” On top of such warning signs as “extreme valuations, bullish sentiment, and consumer confidence,” he adds, “market action has deteriorated in interest-sensitive sectors… As of Friday, more than one-third of stocks are already below their 200-day moving averages.” Don’t be fooled by the booming headline indexes.

More NYSE stocks hit new 52-week lows last week than new 52-week highs, he notes. In a nutshell: Run. OK, so, it is always easy to criticize. Husssman, a professional economist and well-known Wall Street figure, has been here before. He’s been warning about stock-market valuations for several years. He’s in that camp that the permabulls, wrongly, call “permabears.” He’s been wrong — or, perhaps, just very early — many times. But he was, notably, also correct and prescient about both the 2000 and 2008 crashes before they happened, when few others were. Opinions, of course, are free. But facts are sacred. And more than a few are suggesting caution. According to the World Bank, the total U.S. stock market is now valued at more than 150% of annual GDP. That is way above historic norms, and about the same as it was at the market extreme of 2000.

Wall Street speculators are zeroing in on the next U.S. credit crisis: the mall. It’s no secret many mall complexes have been struggling for years as Americans do more of their shopping online. But now, they’re catching the eye of hedge-fund types who think some may soon buckle under their debts, much the way many homeowners did nearly a decade ago. Like the run-up to the housing debacle, a small but growing group of firms are positioning to profit from a collapse that could spur a wave of defaults. Their target: securities backed not by subprime mortgages, but by loans taken out by beleaguered mall and shopping center operators. With bad news piling up for anchor chains like Macy’s and J.C. Penney, bearish bets against commercial mortgage-backed securities are growing.

In recent weeks, firms such as Alder Hill Management – an outfit started by protégés of hedge-fund billionaire David Tepper – have ramped up wagers against the bonds, which have held up far better than the shares of beaten-down retailers. By one measure, short positions on two of the riskiest slices of CMBS surged to $5.3 billion last month – a 50% jump from a year ago. “Loss severities on mall loans have been meaningfully higher than other areas,” said Michael Yannell at Gapstow Capital, which invests in hedge funds that specialize in structured credit. Nobody is suggesting there’s a bubble brewing in retail-backed mortgages that is anywhere as big as subprime home loans, or that the scope of the potential fallout is comparable.

After all, the bearish bets are just a tiny fraction of the $365 billion CMBS market. And there’s also no guarantee the positions, which can be costly to maintain, will pay off any time soon. Many malls may continue to limp along, earning just enough from tenants to pay their loans. But more and more, bears are convinced the inevitable death of retail will lead to big losses as defaults start piling up. The trade itself is similar to those that Michael Burry and Steve Eisman made against the housing market before the financial crisis, made famous by the book and movie “The Big Short.” Often called credit protection, buyers of the contracts are paid for CMBS losses that occur when malls and shopping centers fall behind on their loans. In return, they pay monthly premiums to the seller (usually a bank) as long as they hold the position. This year, traders bought a net $985 million contracts that target the two riskiest types of CMBS. That’s more than five times the purchases in the prior three months.

The Federal Reserve, which has struggled to stoke inflation since the financial crisis and up until now raised rates less frequently than it and markets expected, may be about to hit the accelerator on rate hikes. On Wednesday, the U.S. central bank is almost universally expected to raise its benchmark interest rates, a move that just a few weeks ago was viewed by the markets as unlikely. And with inflation showing signs of perking up, Fed policymakers may signal there could be more than the three rate rises they have forecast for this year. “They do not have as much room to be patient as they did before,” said Tim Duy, an economics professor at the University of Oregon, who expects Fed policymakers to lift their rate forecasts this week.

Policymakers have their eyes on achieving full employment and 2-percent inflation. The faster the economy approaches those goals, Duy said, the quicker the Fed will want to tighten policy to avoid getting behind the curve. “That’s an acceleration in the dots,” he said, referring to forecasts published by the Fed that show policymakers’ individual rate-hike forecasts as dots on a chart. The economy already appears closer to its goals than the Fed had expected in December, the last time it released forecasts. The jobless rate, at 4.7%, is below what policymakers see as the long-run norm, and inflation, at 1.7%, is already in the range they had expected by year end. As Fed policymakers prepare to raise rates this week for the second time in three months, the inflation terrain they face looks steeper than it has been since the financial crisis when one of the central bank’s policy aims was to generate inflation.

There are signs of more inflation globally, the dollar is pushing down less on U.S. prices, domestic inflation expectations have picked up and Friday’s closely watched monthly jobs report showed wages rising 2.8% year-on-year in February, with payrolls rising a sturdy 235,000. The Fed’s preferred inflation measure, the so-called core PCE price index, recorded its biggest monthly increase in five years in January and was up 1.7% year-on-year after a similar gain in December. Most Fed policymakers say such data gives them increasing confidence that inflation will eventually reach the Fed’s goal after years of undershooting.

As of October 24, the U.S. Treasury was flush with $435 billion of cash. That was because the department’s bureaucrats had been issuing debt hand-over-fist and piling up a cash hoard, apparently, for the period after March 15, 2017 when President Hillary Clinton would need to coax another debt ceiling increase out of Congress. Needless to say, Hillary was unexpectedly (and thankfully) retired to Chappaqua, New York. But the less discussed surprise is that the U.S. Treasury’s cash hoard has virtually disappeared in the run-up to the March 15 expiration of the debt ceiling holiday. That’s right. As of the Daily Treasury Statement (DTS) for March 7, the cash balance was down to just $88 billion — meaning that $347 billion of cash has flown out the door since October 24.

And I find that on March 8 alone the Treasury consumed another $22 billion of cash — bringing the balance down to $66 billion! To be sure, there has been no heist at the Treasury Building — other than the normal larceny that is the stock-in-trade of the Imperial City. What’s different this time around is that the bureaucrats have apparently decided to sabotage what they undoubtedly believe to be the usurper in the White House. To this end, they’ve been draining Trump’s bank account rather than borrowing the money to pay Uncle Sam’s monumental bills. This has especially been the case since the January 20 inauguration. The net Federal debt on March 7 was $19.802 trillion — up $237 billion since January 20th. But that’s not the half of it. During that same 47 day period, the Treasury bureaucrats took the opportunity to pay-down $57 billion of maturing treasury bills and notes by tapping its cash hoard.

In all, they drained $294 billion from the Donald’s bank account during that brief period — or about $6.4 billion per day. You wouldn’t be entirely wrong to conclude that even Putin’s alleged world class hackers couldn’t have accomplished such a feat. At this point I could don my tin foil hat because this massive cash drain was clearly deliberate. Last year, for example, during the same 47 day period, the operating deficit was even slightly larger — $253 billion. But the Treasury funded that mainly by new borrowings of $157 billion, which covered 62% of the shortfall. Its cash balance was still $223 billion on March 7. Again, that cash balance is just $66 billion right now. Moreover, the Trump Administration has only a few business days until its credit card expires on March 15 — so it’s also way too late for an eleventh hour borrowing spree to replenish its depleted cash account. (Besides that, I’m predicting a very dangerous market event will start on the 15th.)

We see health as a basic human right. Every society should provide medical care for its citizens at the level it can afford. And, while the United States has made some progress in improving access to care, the results do not justify the costs. So, while we agree with President Trump’s statement that the U.S. health care system should be cheaper, better and universal, the question is how to get there. In this post, we start by setting the stage: where matters stand today and why they are unacceptable. This leads us to the real question: where can and should we go? As economists, we are genuinely partial to market-based solutions that allow individuals to make tradeoffs between quality and price, while competition pushes suppliers to contain costs.

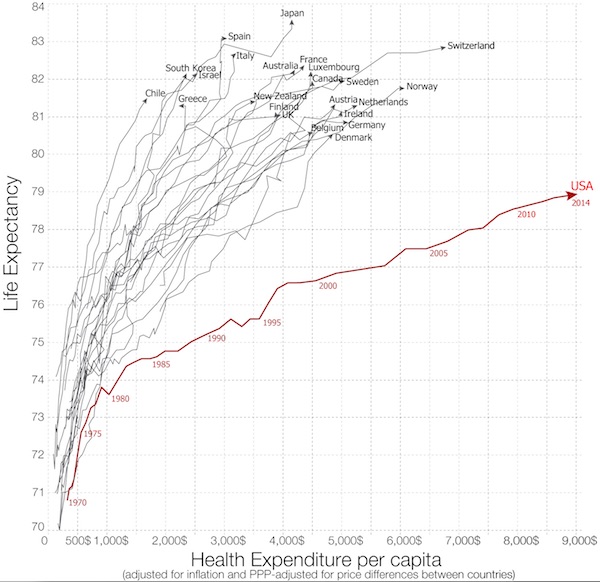

But, in the case of health care, we are skeptical that such a solution can be made workable. This leads us to propose a gradual lowering of the age at which people become eligible for Medicare, while promoting supplier competition. Before getting to the details of our proposal, we begin with striking evidence of the inefficiency of the U.S. health care system. The following chart (from OurWorldInData.org) displays life expectancy at birth on the vertical axis against real health expenditure per capita on the horizontal axis. The point is that the U.S. line in red lies well below the cost-performance frontier established by a range of advanced economies (and some emerging economies, too). Put differently, the United States spends more per person but gets less for its money.

Life Expectancy and Health Expenditure per capita, 1970-2014

It really doesn’t matter how you measure U.S. health care outlays, you will come away with the same conclusion: the U.S. system is extremely inefficient compared to that of other countries. Today, for example, health expenditures account for more than 17% of U.S. GDP. This is more than twice the average of the share in the 42 other countries shown in the figure, and more than 40% higher than the next highest (which happens to be Sweden at 12%).

“..considering the Trump administration is directly sending American troops to fight in Syrian territory, perhaps the various rebel groups on the ground have outlived their usefulness..”

According to a press release released Friday by the office of Rep. Tulsi Gabbard, Sen. Rand Paul has introduced their bill, the Stop Arming Terrorists Act, in the U.S. Senate. The bipartisan legislation (H.R.608 and S.532) aims to prohibit any federal agency from using taxpayer dollars to provide weapons, cash, intelligence, or any support to al-Qaeda, ISIS, and other terrorist groups. It would also prohibit the government from funneling money and weapons through other countries that are directly or indirectly supporting terrorists.

Gabbard said: “For years, the U.S. government has been supporting armed militant groups working directly with and often under the command of terrorist groups like ISIS and al-Qaeda in their fight to overthrow the Syrian government. Rather than spending trillions of dollars on regime change wars in the Middle East, we should be focused on defeating terrorist groups like ISIS and al-Qaeda, and using our resources to invest in rebuilding our communities here at home.” [..] “The fact that American taxpayer dollars are being used to strengthen the very terrorist groups we should be focused on defeating should alarm every Member of Congress and every American. We call on our colleagues and the Administration to join us in passing this legislation.

Rand Paul provided much-needed support for the bill, stating: “One of the unintended consequences of nation-building and open-ended intervention is American funds and weapons benefiting those who hate us. This legislation will strengthen our foreign policy, enhance our national security, and safeguard our resources.” The legislation is currently co-sponsored by Reps. John Conyers (D-MI); Scott Perry (R-PA); Peter Welch (D-VT; Tom Garrett (R-VA); Thomas Massie (R-KY); Barbara Lee (D-CA); Walter Jones (R-NC); Ted Yoho (R-FL); and Paul Gosar (R-AZ). It is endorsed by Progressive Democrats of America (PDA), Veterans for Peace, and the U.S. Peace Council.

One of Trump’s campaign narratives that resonated deeply with his voter base was an anti-radical Islam agenda, which separated him from Clinton’s campaign as he vowed to “bomb the shit” out of ISIS-controlled oil fields. However, his voter base may or may not be somewhat disillusioned now given that he just approved an arms sale to Saudi Arabia that was so controversial it was even blocked by Obama, a president who made a literal killing from arms sales to the oil-rich kingdom (ISIS adheres to Saudi Arabia’s twisted form of Wahhabist philosophy). In the context of recent events, whether or not the Trump administration will get fully behind Gabbard’s bill remains to be seen. But considering the Trump administration is directly sending American troops to fight in Syrian territory, perhaps the various rebel groups on the ground have outlived their usefulness and the bill will be allowed to proceed unimpeded.

“The first hurdle for the lawsuits will be proving “standing,” which means finding someone who has been harmed by the policy. With so many exemptions, legal experts have said it might be hard to find individuals who would have a right to sue..”

A group of states renewed their effort on Monday to block President Donald Trump’s revised temporary ban on refugees and travelers from several Muslim-majority countries, arguing that his executive order is the same as the first one that was halted by federal courts. Court papers filed by the state of Washington and joined by California, Maryland, Massachusetts, New York and Oregon asked a judge to stop the March 6 order from taking effect on Thursday. An amended complaint said the order was similar to the original Jan. 27 directive because it “will cause severe and immediate harms to the States, including our residents, our colleges and universities, our healthcare providers, and our businesses.” A Department of Justice spokeswoman said it was reviewing the complaint and would respond to the court.

A more sweeping ban implemented hastily in January caused chaos and protests at airports. The March order by contrast gave 10 days’ notice to travelers and immigration officials. Last month, U.S. District Judge James Robart in Seattle halted the first travel ban after Washington state sued, claiming the order was discriminatory and violated the U.S. Constitution. Robart’s order was upheld by the 9th U.S. Circuit Court of Appeals. Trump revised his order to overcome some of the legal hurdles by including exemptions for legal permanent residents and existing visa holders and taking Iraq off the list of countries covered. The new order still halts citizens of Iran, Libya, Syria, Somalia, Sudan and Yemen from entering the United States for 90 days but has explicit waivers for various categories of immigrants with ties to the country.

[..] The first hurdle for the lawsuits will be proving “standing,” which means finding someone who has been harmed by the policy. With so many exemptions, legal experts have said it might be hard to find individuals who would have a right to sue, in the eyes of a court. To overcome this challenge, the states filed more than 70 declarations of people affected by the order including tech businesses Amazon and Expedia, which said that restricting travel hurts their revenues and their ability to recruit employees. Universities and medical centers that rely on foreign doctors also weighed in, as did religious organizations and individual residents, including U.S. citizens, with stories about separated families.

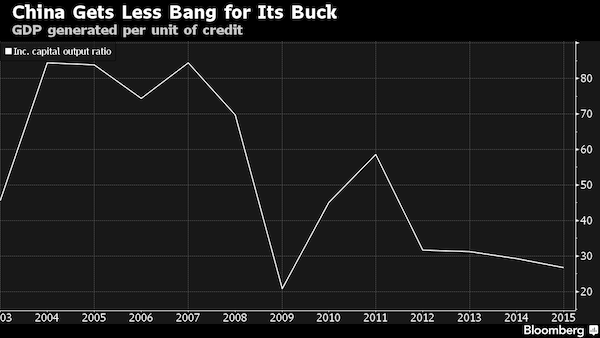

A research note from Goldman Sachs highlights how large, complex and opaque China’s credit market has become over the last decade. In a report called Mapping China’s Credit, analysts Kenneth Ho and Claire Cui write that the rise in China’s total debt started with a RMB 4 trillion ($AU770 billion) stimulus package in 2009 to counter the global financial crisis. Since late 2008, debt to GDP (excluding financial debt) has risen from 158% to 262%. Including financial debt bumps the figure up to 289%. The rise in China’s debt to GDP follows a similar increase in America, where last week bond fund manager Bill Gross discussed the risks associated with the US debt to GDP ratio, which sits at around 350%. The analysts note they’re struggling to break down and make sense of the country’s credit market.

“Given the development of the shadow banking sector, and the introduction of a number of retail investment channels such as wealth management products, it has become much more difficult to analyse and monitor China’s credit growth,” they say. In 2006, 85% of China’s credit was supplied by bank loans (offset by deposits). According to Ho and Cui’s estimates, the share of credit from bank loans has reduced to 53%. In its place, approximately 31% of debt is now supplied through bond and securities markets, and 16% through the shadow banking sector (more on that later). Ho and Cui write that as China’s debt pool has grown, larger state-related companies have seen a significant increase in leverage through traditional loans from state-affiliated banks. In addition, however, a decrease in domestic interest rates has encouraged smaller companies and individual investors to shift savings away from bank deposits.

Let’s take a breather from more consequential money matters at hand midweek to consider the tending moods of our time and place — while a blizzard howls outside the window, and nervous Federal Reserve officials pace the grim halls of the Eccles Building. It is clear by now that we have four corners of American politics these days: the utterly lost and delusional Democratic party; the feckless Republicans; the permanent Deep State of bureaucratic foot-soldiers and errand boys; and Trump, the Golem-King of the Coming Greatness. Wherefore, and what the fuck, you might ask. The Democrats reduced themselves to a gang of sadistic neo-Maoists seeking to eradicate anything that resembles free expression across the land in the name of social justice.

Coercion has been their coin of the realm, and especially in the realm of ideas where “diversity” means stepping on your opponent’s neck until he pretends to agree with your Newspeak brand of grad school neologisms and “inclusion” means welcome if you’re just like us. I say Maoists because just like Mao’s “Red Guard” of rampaging students in 1966, their mission is to “correct” the thinking of those who might dare to oppose the established leader. Only in this case, that established leader happened to lose the sure-thing election and the party finds itself unbelievably out-of-power and suddenly purposeless, like a termite mound without a queen, the workers and soldiers fleeing the power center in an hysteria of lost identity.

They regrouped briefly after the election debacle to fight an imaginary adversary, Russia, the phantom ghost-bear, who supposedly stepped on their termite mound and killed the queen, but, strangely, no actual evidence was ever found of the ghost-bear’s paw-print. And ever since that fact was starkly revealed by former NSA chief James Clapper on NBC’s Meet the Press, the Russia hallucination has vanished from page one of the party’s media outlets — though, in an interesting last gasp of striving correctitude, Monday’s New York Times features a front page story detailing Georgetown University’s hateful traffic in the slave trade two centuries ago. That should suffice to shut the wicked place down for once and for all!

It looks set to be a week packed with big financial milestones. In the US, the Federal Reserve will raise interest rates, putting the country on a path towards getting back to a normal price for money. In the Netherlands, a tense election may deal the fragile eurozone another blow. In this country, Theresa May could finally trigger Article 50, starting the process of taking the UK out of the European Union. The most significant event, however, as is so often the case, may well be something that hardly anyone is paying attention to. On Sunday, Iceland ended capital controls, finally returning its economy to normal after a catastrophic banking collapse back in 2008 and 2009. Why does that matter? Because Iceland was the one country that defied the global consensus and did not bail out its bankers.

True, there was shock to the system. But it was relatively short, and once the pain was dealt with, the country has bounced back stronger than ever. There is, surely, a lesson in that. It might well be better just to let banks go to the wall. Next time around, we should follow Iceland’s example. The crash of 2008 hit every country in the world. And yet none was quite so completely destroyed as Iceland. A tiny country, home to just 323,000 people, with cod fishing and tourism as its two major industries, it deregulated its finance sector and went on a wild lending spree. Its banks started bulking up in a way that might have made Royal Bank of Scotland’s Fred Goodwin start to wonder if his foot wasn’t pressed too hard on the accelerator. When confidence collapsed, those banks were done for.

In every other country in the world, the conventional wisdom dictated the financiers had to be bailed out. The alternative was catastrophe. Cash machines would stop working, trade would grind to a halt, and output would collapse. It would be the 1930s all over again. The state had no option but to dig deep, and pay whatever it took to keep the financial sector alive. But Iceland did not have that option. Its banks had run up debts of $86bn, an impossible sum for an economy with a GDP of $13bn in 2009. Even Gordon Brown, in full “saving the world’” mode, might have baulked at taking on liabilities of that scale. Iceland did the only thing it could do under the circumstances. It let its banks go bust: as British depositors quickly found out to their cost.

Chancellor Angela Merkel derided as “clearly absurd” Turkish President Recep Tayyip Erdogan’s accusation that Germany supports terrorism, as Ankara announced retaliatory measures against the Dutch government amid escalating tensions with Europe. After Erdogan excoriated Merkel’s government for “openly giving support to terrorist organizations” on Monday, the Turkish government announced it would block the Dutch ambassador from re-entering the country. Erdogan has blasted European leaders, including accusing Germany of using “Nazi practices,” after a string of rallies by Turkish ministers on European soil were canceled. “The chancellor has no intention of participating in a competition of provocations” with Erdogan, her chief spokesman, Steffen Seibert, said in an emailed statement on Monday. “She’s not going to join in with that. The accusations are clearly absurd.”

Erdogan is seeking votes from Turkish expatriates in a referendum next month on constitutional changes that would make the presidency his country’s highest authority. He has lashed out at the EU and risked deepening tensions, particularly with Merkel. In an interview on Monday, he said Merkel’s government “mercilessly” supported groups such as the Kurdish PKK group, which has waged a separatist war with the Turkish military for more than three decades. “I don’t want to put all EU countries in the same basket, but some of them can’t stand Turkey’s rise, primarily Germany,” Erdogan told A Haber television. The standoff came to a head over the weekend when the Dutch government prevented Turkish ministers from participating in referendum campaign rallies. Some 3 million Turks outside their country can vote, though fewer than half of them did so in the last general election in 2015.

Merkel struck an unusually strident tone earlier this month, slamming Erdogan for trivializing World War II-era crimes by using a Nazi comparison to censure Germany for canceling ministers’ appearances. Such a tone “can’t be justified,” Merkel said March 6 after Erdogan’s previous outburst. European leaders have been vocal in their disapproval of the referendum, saying the executive-centered system that Erdogan is planning to introduce will concentrate power in the president’s hands at the expense of democracy in a NATO member state and EU membership applicant.

Theresa May’s Brexit bill has cleared all its hurdles in the Houses of Parliament, opening the way for the prime minister to trigger article 50 by the end of March. Peers accepted the supremacy of the House of Commons late on Monday night after MPs overturned amendments aimed at guaranteeing the rights of EU citizens in the UK and giving parliament a “meaningful vote” on the final Brexit deal. The decision came after a short period of so-called “ping pong” when the legislation bounced between the two houses of parliament as a result of disagreement over the issues. The outcome means the government has achieved its ambition of passing a “straightforward” two-line bill that is confined simply to the question of whether ministers can trigger article 50 and start the formal Brexit process.

It had been widely predicted in recent days that May would fire the starting gun on Tuesday, immediately after the vote, but sources quashed speculation of quick action and instead suggested she will wait until the final week of March. MPs voted down the amendment on EU nationals’ rights by 335 to 287, a majority of 48, with peers later accepting the decision by 274 to 135. The second amendment on whether to hold a meaningful final vote on any deal after the conclusion of Brexit talks was voted down by 331 to 286, a majority of 45, in the Commons. The Lords then accepted that decision by 274 to 118, with Labour leader Lady Smith telling the Guardian that continuing to oppose the government would be playing politics because MPs would not be persuaded to change their minds.

“If I thought there was a foot in the door or a glimmer of hope that we could change this bill, I would fight it tooth and nail, but it doesn’t seem to be the case,” she said. But the decision led to tensions between Labour and the Lib Dems, whose leader, Tim Farron, hit out at the main opposition. “Labour had the chance to block Theresa May’s hard Brexit, but chose to sit on their hands. Tonight there will be families fearful that they are going to be torn apart and feeling they are no longer welcome in Britain. Shame on the government for using people as chips in a casino, and shame on Labour for letting them,” he said.

Theresa May has faced down Nicola Sturgeon’s demand for a second referendum on Scottish independence, accusing the SNP leader of “tunnel vision” and rejecting her timetable for a second vote. The prime minister said that the Scottish leader’s plan to hold a second referendum between the autumn of 2018 and spring 2019 represented the “worst possible timing,” setting the Conservative government on a collision course with the administration in Holyrood. The first minister’s intervention had been timed a day ahead of when May had been predicted to trigger article 50, but No 10 later indicated that it would not serve notice to leave the EU until the end of the month. The confirmation of the later date, in the aftermath of the speech, fuelled speculation the prime minister had been unnerved by Sturgeon.

Buoyed by three successive opinion polls putting support for independence at nearly 50/50, Sturgeon said that she had been left with little choice than to offer the Scottish people, who voted to remain in the EU, a choice at the end of the negotiations of a “hard Brexit” or living in an independent Scotland. “The UK government has not moved even an inch in pursuit of compromise and agreement. Our efforts at compromise have instead been met with a brick wall of intransigence,” the first minister said, claiming that any pretence of a partnership of equal nations was all but dead. Downing Street denied that it had ever planned to fire the starting gun on Brexit this week, but critics pointed out that ministers had failed to deny the widespread suggestion in media reports over the weekend. The Guardian understands that May will now wait until the final week of March to begin the process, avoiding a clash with the Dutch elections and the anniversary of the Rome Treaty, and giving the government time to seek consensus in different parts of the country.

Supermarkets in Quebec will now be able to donate their unsold produce, meat and baked goods to local food banks in a program – described as the first of its kind in Canada – that also aims to keep millions of kilograms of fresh food out of landfills. The Supermarket Recovery Program launched in 2013 as a two-year pilot project. Developed by the Montreal-based food bank Moisson Montréal, the goal was to tackle the twin issues of rising food bank usage in the province and the staggering amount of edible food being regularly sent to landfills. Provincial officials said the pilot – which last year saw 177 supermarkets donate more than 2.5m kg of food that would have otherwise been discarded – would now begin expanding across the province.

“The idea behind it is: ‘Hey, we’ve got enough food in Quebec to feed everybody, let’s not be throwing things out,’” Sam Watts, of Montreal’s Welcome Hall Mission, which offers several programs for people in need, told Global News on Friday. “Let’s be recuperating what we can recuperate and let’s make sure we get it to people who need it.” Recent years have seen food bank usage surge across Canada, with children making up just over a third of the 900,000 people who rely on the country’s food banks each month. In Quebec, the number of users has soared by nearly 35% since 2008, to about 172,000 people per month.

The program’s main challenge was in developing a system that would allow products such as meat and frozen foods to be easily collected from grocers and quickly redistributed, said Watts. “There is enough food in the province of Quebec to feed everybody who needs food. Our challenge has always been around management and distribution,” he added. “Supermarkets couldn’t accommodate individual food banks coming to them one by one by one.” More than 600 grocery stores across the province are expected to take part in the program, diverting as many as 8m kg of food per year.

The austerity measures introduced by the government are forcing thousands of taxpayers to hand over inherited property to the state as they are unable to cover the taxation it would entail. The number of state properties grew further last year due to thousands of confiscations that reached a new high. According to data presented recently by Alpha Astika Akinita, real estate confiscations increased by 73 percent last year from 2015, reaching up to 10,500 properties. The fate of those properties remains unknown as the state’s auction programs are fairly limited. For instance, one auction program for 24 properties is currently ongoing. The precise number of properties that the state has amassed is unknown, though it is certain they are depreciating by the day, which will make finding buyers more difficult.

Financial hardship has forced many Greeks to concede their real estate assets to the state in order to pay taxes or other obligations. Thousands of taxpayers are unable to pay the inheritance tax, while others who cannot enter the 12-tranche payment program are forced to concede their properties to the state. Worse, the law dictates that any difference between the obligations due and the value of the asset conceded should not be returned to the taxpayer. The government had announced it would change that law, but nothing has happened to date. Property market professionals estimate that the upsurge in forfeiture of inherited property will continue unabated in the near future as the factors that have generated the phenomenon, such as high unemployment, the Single Property Tax (ENFIA) etc, remain in place.

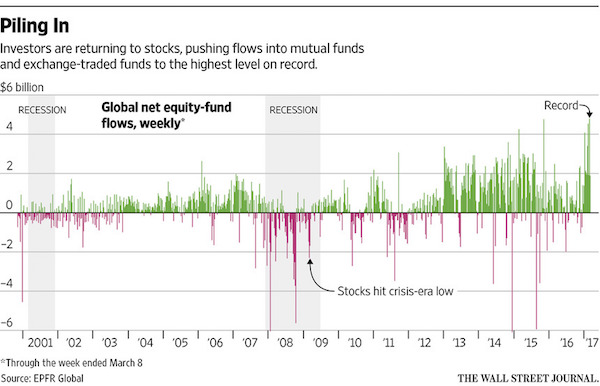

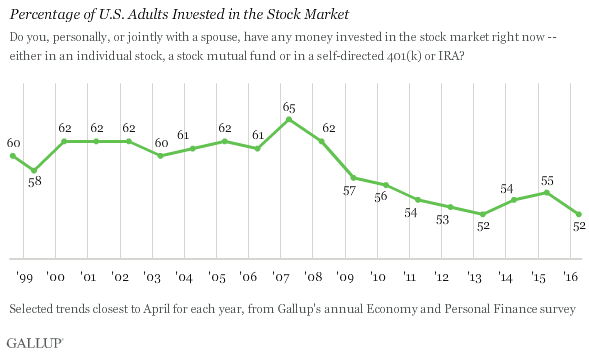

The stock-market rally presents a difficult choice for some individual investors: Miss out or risk getting in at the top. The scars of the financial crisis have left many wary, even as the second-longest bull run in S&P 500 history has added more than $14 trillion in value to the index since it bottomed in March 2009, according to S&P Dow Jones Indices. Yet there are signs that caution is dissipating. Investors have poured money into stocks through mutual funds and exchange-traded funds in 2017, with global equity funds posting record net inflows in the week ended March 1 based on data going back to 2000, according to fund tracker EPFR Global. Inflows continued the following week, even as the rally slowed. The S&P 500 shed 0.4% in the week ended Friday.

The investors’ positioning suggests burgeoning optimism, with TD Ameritrade clients increasing their net exposure to stocks in February, buying bank shares and popular stocks such as Amazon.com and sending the retail brokerage’s Investor Movement Index to a fresh high in data going back to 2010. The index tracks investors’ exposure to stocks and bonds to gauge their sentiment. “People went toe in the water, knee in the water and now many are probably above the waist for the first time,” said JJ Kinahan at TD Ameritrade. That brings individual investors increasingly in line with Wall Street professionals. A February survey of fund managers by Bank of America Merrill Lynch found optimism about the global economy improving while investors were holding above-average levels of cash, leaving room for them to drive stocks still higher.

Bullishness among Wall Street newsletter writers reached 63.1%—the highest level since 1987—a week ago in a survey by Investors Intelligence, before falling to 57.7% this past week. Overall investor sentiment is strong right now for the U.S. stock market, said Ann Gugle, principal at Alpha Financial Advisors. She pointed to a typical growth-and-income portfolio with 70% in stocks and 30% in bonds and alternatives. The 70% allocation to stocks, she said, would ordinarily be evenly split between U.S. and international stocks, but for the past three years it has shifted about 40% to U.S. stocks and 30% international.

Last week I updated the Warren Buffett yardstick, market cap-to-GNP. The only time it was ever higher than it is today was for a few months at the top of the dotcom mania.

However, when you look under the surface of the market-cap-weighted indexes at median valuations they are currently far more extreme than they were back then. As my friend John Hussman puts it, this is now “the most broadly overvalued moment in market history.”

U.S. subprime auto lenders are losing money on car loans at the highest rate since the aftermath of the 2008 financial crisis as more borrowers fall behind on payments, according to S&P Global Ratings. Losses for the loans, annualized, were 9.1% in January from 8.5% in December and 7.9% in the first month of last year, S&P data released on Thursday show, based on car loans bundled into bonds. The rate is the worst since January 2010 and is largely driven by worsening recoveries after borrowers default, S&P said. Those losses are rising in part because when lenders repossess cars from defaulted borrowers and sell them, they are getting back less money. A flood of used cars has hit the market after manufacturers offered generous lease terms.

Recoveries on subprime loans fell to 34.8% in January, the worst since early 2010, S&P data show. With losses increasing, investors in bonds backed by car loans are demanding higher returns, as reflected by yields, on their securities. That increases borrowing costs for finance companies, with those that depend on asset-backed securities the most getting hit hardest. American Credit Acceptance, one of nearly two dozen subprime lenders to securitize their loans in recent years, had one of the highest cost of funds last year with yields on its securitizations as high as 4.6%, even as the two-year swap rate benchmark hovered around 1%, according to a report from Wells Fargo. The company relies heavily on asset-backed securities for funding.

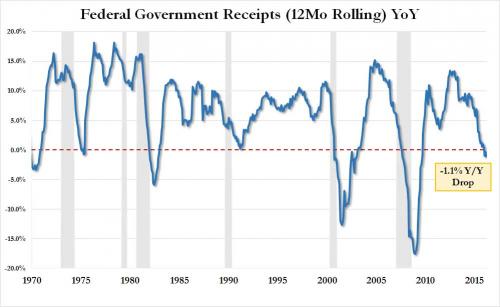

[..] something more concerning emerges when looking at the annual change in the rolling 12 month total. It is here that we find that, like last month, in the LTM period ended Feb 28, total federal revenues, tracked as government receipts on the Treasury’s statement, were $3.275 trillion. This amount was 1.1% lower than the $3.31 trillion reported one year ago, and is the third consecutive month of annual receipt declines. This was the biggest drop since the summer of 2008. At the same time, government spending rose 3.8%. Why is this important? Because as the chart below shows, every time since at least 1970 when government receipts have turned negative on an annual basis, the US was on the cusp of, or already in, a recession. Indicatively, the last time government receipts turned negative was in July of 2008.