Might as well do it this way. May survives confidence vote and can now prepare to defend the deal whose certain defeat made her delay Tuesday’s Parliament vote, a delay which led to the confidence vote in the first place. She still can’t win that one. It’s not so much May who is cooked, it’s the country.

No 10 will not be happy with today’s front pages, which are all about Theresa May’s survival in the no-confidence vote, but paint the win as less of a triumph for May than a pyrrhic victory. Let’s start with the good news for the prime minister. Two papers have come out in support of the her, with the Express featuring a picture of a smiling May and the headline: “Now just let her get on with it”.

The Mail is similarly supportive: “Now let her get on with the job!”, saying that “despite two months of sabre-rattling by her hardline opponents, and deadlock over Brexit, almost two-thirds of Tory MPs backed her”.

Others were less sympathetic. “Time to call it a May”, says the Sun, never one to miss the chance of putting a pun in a headline. The Sun says the prime minister was “left wounded last night after a battering by Tory Brexit rebels”.

The Mirror has: “It’s lame duck for Christmas”, saying May’s “goose is cooked”. The paper describes her as “wounded” and “battered” and says she only managed to survive the no-confidence vote “by promising not to fight the next election”.

A Tory grandee recently sidled up to me to express grave reservations about the Brexit process. “We simply cannot allow the Irish to treat us like this,” the former minister said about the negotiating tactics of the Taoiseach, Leo Varadkar. The Conservative MP was exasperated that the Republic of Ireland (population: 4.8m) has been able to shape the EU negotiating stance that has put such pressure on the UK (population: 66m). “This simply cannot stand,” the one-time moderniser told me. “The Irish really should know their place.” The remarks explained why Conservatives from both sides of the Brexit divide are so troubled by the negotiations. They also explain why Theresa May might find that any concessions from the EU over the Northern Ireland backstop may fall short of the demands of Tory MPs.

Over the last few months Tory MPs have asked in private how the Irish Republic can believe its relationship with the EU trumps its relationship with the UK. They cite economic reasons (the Irish Republic’s strong trading links with the UK) and the historical relationship. The MPs do of course acknowledge that left a troubled legacy. One minister familiar with Anglo-Irish relations points out that these Tories should bear in mind one date and one word to explain both the Irish and the EU’s approach. The date is 1973: when the Irish Republic joined the EEC at the same time as the UK and Denmark. That was the moment when Ireland took a giant political leap at the same time as the UK.

But it turned out to be arguably the biggest unilateral strategic move since Partition in the 1920s – a move that defined the modern Irish Republic as an independent state within Europe, with a wholly different approach to its larger neighbour.

I’m afraid I missed something along the way. If you run for office in the US and someone tries to blackmail you, you can’t get rid of them, you need to have lawsuits, court cases etc., interfere with your campaign. Not doing so is illegal. But, as Candace Owens said today,

“Congress has a slush fund, made up of tax dollars, that is used to pay off & silence their alleged sexual assaults and affairs. To date, over 200 million dollars in 200 settlements have been paid since 1998. But tell us more about Trump’s possible campaign finance violations…”

Moreover, a US judge just sentenced Stormy Daniels to paying Trump’s legal costs. But he was still in the wrong? How is that possible?

Michael Cohen has warned that he has more to say about what he called the ”dirty deeds” of Donald Trump as the president’s former lawyer and fixer was sentenced to three years in prison for facilitating payments to two women who have had alleged affairs with Mr Trump. Cohen was sentenced to 36 months for tax fraud and for his role in the payment of hush money to porn star Stormy Daniels and the former Playboy model Karen McDougal. Both say they had affairs with Mr Trump before the 2016 presidential election. The judge in a district court in New York also handed Cohen an extra two months for lying to Congress about a proposed Trump Tower project in Russia.

The payments have implicated Mr Trump directly in criminal conduct according to a court filing from prosecutors last week, which said that Cohen was working in coordination with the president. Cohen’s adviser Lanny Davis, who was his attorney for the case, said after the sentencing that Cohen will disclose more information concerning Mr Trump, once Robert Mueller wraps up his investigation into Russian interference in the 2016 US presidential election and possible collusion with Trump campaign officials. “At the appropriate time, after Mr Mueller completes his investigation and issues his final report, I look forward to assisting Michael to state publicly all he knows about Mr Trump – and that includes any appropriate congressional committee interested in the search for truth and the difference between facts and lies,” Mr Davis said in a statement.

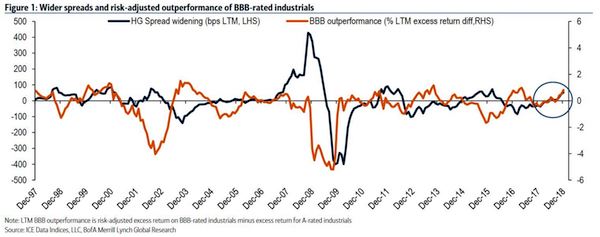

The corporate debt scaring policy experts like former Fed Chair Janet Yellen isn’t throwing too much of a fright into market participants. In fact, some of them are continuing to load up on lower-grade corporate debt because it’s managed to be a better performer than some of the investments considered to be safer. “Offense is the best defense,” Hans Mikkelsen, credit strategist at Bank of America Merrill Lynch, told clients in a note pointing out that BBB-rated companies are outperforming their A-rated counterparts. BBB is the last rung before junk, and the increasing level of company bonds going to that level is causing concern.

Some investors worry that the companies whose debt is in danger of slipping into high-yield territory will have trouble meeting their obligations during the next economic downturn. But Mikkelsen thinks those concerns are misplaced. The S&P 500 Triple-B investment-grade corporate bond index is down 2.9 percent year to date, which is not good. However, the group is outperforming the broader S&P 500/MarketAxess Investment Grade Corporate Bond Index, which is off 3.5 percent in 2018. The outperformance grows when isolating for risk-adjusted excess returns and runs counter to history when credit spreads are widening. Higher-quality bonds usually outperform in those cases, Mikkelsen noted.

“This outperformance of BBBs is noteworthy as one of [the] key investor concerns this year remains the possibility that large BBB-rated capital structures get downgraded to high yield during the next downturn,” Mikkelsen wrote. “We think this outperformance reflects in part a low recession probability being priced into credit spreads, as well as the fact that most large BBBs are unlikely to get downgraded to [high-yield] anytime soon as they tend to have stable cash flows and significant financial flexibility.”

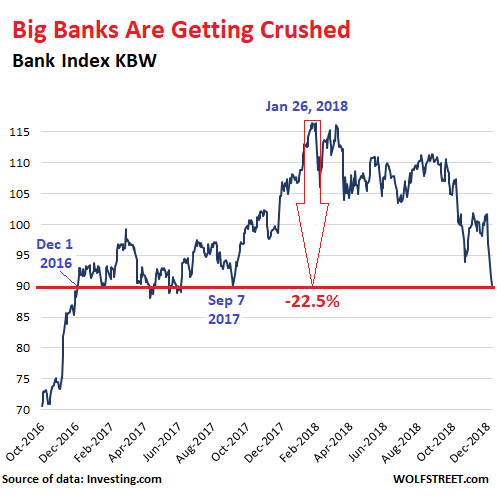

On Tuesday, the US KBW Bank index, which tracks the largest 24 US banks and serves as a benchmark for the banking sector, dropped 1.2%, the fifth day in a row of declines, to the lowest close since September 7, 2017. The index is now back where it had been on December 1, 2016. Two years of big gains gone up in smoke. [..] But no, the index doesn’t include Goldman Sachs – which is big in other ways but not as a bank, and which has skidded 35% from its all-time peak in February. The index has now dropped 22.5% since the post-financial crisis peak on January 26:

So far in Q4, the index has dropped 14%. Unless a miraculous banking-Santa-Claus rally pulls banks out of their dive by the end of the quarter, a 14% decline would make it the worst quarterly decline since Q3 2011. If tax selling kicks in, given the losses bank-stock investors have taken so far this year, it could get worse in the coming days. Not even in Q3 2015, during the oil bust, when investors were fearing that banks would take steep losses on their loans to the oil industry, did shares drop this much.

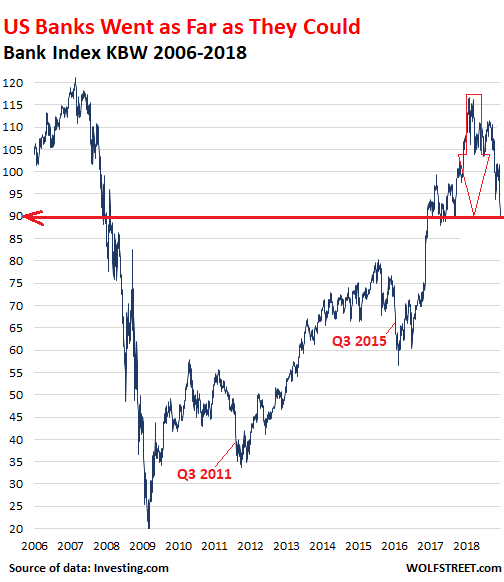

The index is now back where it had first been a couple of years before its crazy peak in February 2007. Said peak occurred about a year before Bear Stearns toppled. During the subsequent collapse of banks stocks, it looked like the index would hit zero. After the bottom in March 2009, the Fed’s strategies to benefit the banks and those that owned them took hold, at the expense of depositors and other classes of US stake holders, such as renters or future home buyers. And it worked. But that era is now over. And the tax cut too has been baked in, and banks are left to fend for themselves:

Those negative rates will come back to haunt Draghi. But when their damage becomes obvious, he’ll be living quietly in some splendid villa on Lake Como.

The European Central Bank is all but certain to formally end its lavish bond purchase scheme on Thursday but will take an increasingly dim view on growth, raising the odds that its next step in removing stimulus will be delayed. The long-flagged end of bond buys must be irreversible for the sake of credibility, but with France and Italy in political turmoil, a global trade war still looming large and growth slowing, ECB chief Mario Draghi will be keen to emphasize that other forms of support will remain. This leaves Draghi with yet another delicate balancing act: appear confident enough to justify the end of the 2.6 trillion euro ($2.95 trillion), four-year-long bond buying program, but also sound sufficiently concerned to keep investors expectations about further policy tightening relatively cool.

“Ending quantitative easing now looks more like the ammunition is running out rather than (being) based on a convincing economic outlook,” Societe Generale economist Anatoli Annenkov said. The ECB’s problem is that growth is weaker than policymakers thought even just weeks ago while the predicted rise in underlying inflation has failed to materialize, putting in doubt some of the bank’s assumptions about the broader economy. Overall inflation, the ECB’s primary objective, may be near the target now but falling oil prices suggest a dip in the months ahead and a solid rise in wages is not feeding through to prices, leaving the bank with an unexplained disconnect.

Highlighting this complication, the ECB is likely to cut growth and underlying inflation projections and may take a dimmer view on risks, all while Draghi argues that growth is merely falling back to normal after a recent run.

ECB President Mario Draghi has to tread a fine line once again as he gives his latest update on euro area monetary policy on Thursday. While steering the bank out of its QE program and stressing interest rates and reinvestments going forward, Draghi is faced with an economy that may be slowing and a dreary inflation outlook. “We expect the ECB to announce at its meeting next Thursday an end to net-purchases under the APP programme,” said Natixis’ Dirk Schumacher in a note. “While there has been a clear weakening in the economic environment, the ECB will argue that the reinvestment of the stock of bond holdings will ensure a continuing accommodative policy stance justifying an end of the program,” he added.

On Thursday, the ECB also will publish its newest staff projections for economic growth and inflation for the next three years. While it is expected that the central bank will lower its outlook for growth for the next two years, the numbers are also expected to remain just punchy enough to underline the case to exit their purchase program. Another big topic for Thursday will be the design of the ECB’s reinvestments. “The ECB will likely maintain its guidance that it will fully reinvest the proceeds and thus keep its bond holdings constant ‘for an extended period of time’ and ‘for as long as necessary’ to put inflation on track towards its target,” said Florian Hense, Economist with Berenberg.

Left-of-center lawmakers in France have tabled a motion of no confidence in the French government following repeated protests and scenes of violence. The “gilets jaunes” (“yellow vests”) crisis started as a demonstration against a carbon tax policy and planned fuel tax increases, but have morphed into wider discontent at the leadership of President Emmanuel Macron. Now representatives from the French Communist Party, the Socialist Party and the far-left populist movement France Unbowed (La France Insoumise) have come together to table the motion against Macron’s government.

The government of Georges Pompidou in 1962 was successfully toppled by such a motion but few believe this one will pass as Macron’s centrist La République En Marche! party enjoys a strong majority in the 577-seat house. “The French political system makes it extremely difficult to remove a President from office,” said the Deputy Director of Research at Teneo Intelligence in a note Wednesday. “The only political tool available to the opposition to expel Macron is the constitution’s impeachment procedure, which no one is currently considering,” he added.

Japan has chosen the character for ‘disaster’ to symbolise 2018. The public chose the symbol following a series of natural disasters. In July, 200 people died in floods and millions were evacuated from their homes, and mere days later 65 people died in a heatwave that hospitalised more than 20,000 people. The country was also hit by an earthquake with a magnitude of 6.7 and was rocked by its strongest typhoon for 25 years. These numerous natural disasters have had an adverse effect on the Japanese economy, and the country’s GDP has gradually shrunk over the last three months, by 1.2 per cent.

The country also experienced societal problems this year, as stories of sexual harassment in the workplace and suicide rates came to light. The master of the ancient temple in Kyoto, Seihan Mori, wrote the symbol for ‘disaster’ in dark ink on traditional white washi paper to mark the vote. The competition has been run by the Kanji Aptitude Testing Foundation since 1995. In the annual poll, 21,000 of the 190,000 people who voted picked the character to summarise the years events, but the symbol for peace was a close runner-up.

What kind of headline is this, Reuters? The UK has refused Assange medical care for years, and now you make it look like Ecuador, not Assange himself. makes it happen?

Wikileaks founder Julian Assange received a series of medical exams, Ecuador’s top attorney said on Wednesday, in line with a new set of rules for his asylum at the Andean country’s London embassy that prompted him to sue the government. Assange first took asylum in the embassy in 2012, but his relationship with Ecuador has grown increasingly tense, with President Lenin Moreno saying he does not like his presence in the embassy. The government in October imposed new rules requiring him to receive routine medical exams, following concerns he was not getting the medical attention he needed. The rules also ordered Assange to pay his medical and phone bills and clean up after his pet cat.

Inigo Salvador told reporters Ecuador did not have access to results of the tests, which were conducted by doctors Assange trusted, out of respect for his privacy. But he said Assange, who has sued Ecuador arguing that the new rules violate his rights, appeared coherent and lucid to him. On Wednesday, Assange appeared via videoconference in an Ecuadorean court to appeal a previous ruling that had upheld the new rules. Assange is concerned that Ecuador is seeking to end his asylum and extradite him to the United States, but Ecuador has said the United Kingdom told it he would not be extradited.

U.S. officials have acknowledged that federal prosecutors have been conducting a lengthy criminal probe into Assange and Wikileaks. Wikileaks published U.S. diplomatic and military secrets when Assange ran the operation. A lawyer for Assange said he did not know the results of the medical tests, and called on Ecuador to produce documentation proving that the UK would not extradite him to any country where his life was at risk.

Julian Assange has accused his Ecuadorean hosts of spying and feeding information to US authorities, and slammed attempts to block his journalistic work as a more subtle way of silencing than the murder of Jamal Khashoggi. Suggesting there were “facts of espionage” inside the embassy, the WikiLeaks co-founder expressed concern during a hearing in Quito on Wednesday that Ecuadorean intelligence is not only spying on him, but sharing the data it has harvested with the FBI. Ecuadorean intelligence clearly spent a sizable amount of money equipping the embassy for surveillance, Assange added.

He accused Ecuadorean authorities of “comments of a threatening nature” relating to his journalistic work and compared attempts to silence him to the murder of Washington Post columnist Jamal Khashoggi, who was tortured and cut up in the Saudi embassy in Istanbul in October, but “more subtle.” The comparison elicited a harsh reaction from Ecuadorean Prosecutor General Inigo Salvador, who accused Assange of biting the hand that feeds him. Assange told the Ecuadorean court that the living conditions in the embassy were so detrimental to his health that they may put him in the hospital – and suggested that may be the point, because once he leaves the building, he’s fair game for UK and US authorities.

[..] Assange was in court appealing a strict set of rules handed down in October governing his conduct, which he has called a violation of human rights. He submitted 15 “facts of evidence” along with letters from individuals and groups barred from visiting him at the embassy. An earlier attempt to sue his hosts over the restrictive measures was ultimately dismissed by a judge last month, while Assange rejected E

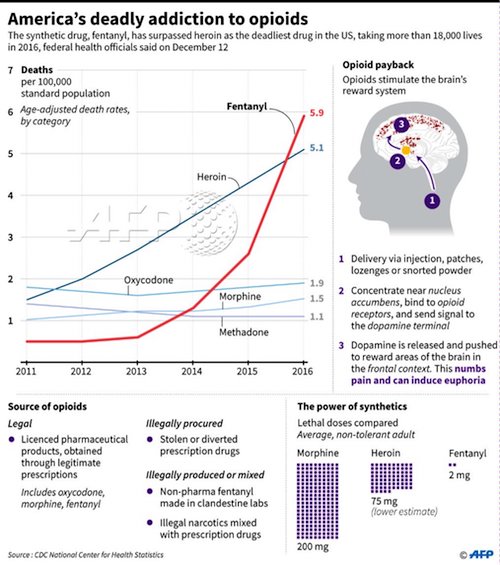

The synthetic drug, fentanyl, has surpassed heroin as the deadliest drug in the United States, taking more than 18,000 lives in 2016, federal health officials said Wednesday. In 2016, the latest year for which full data is available, “29 percent of all drug overdose deaths mentioned involvement of fentanyl,” said the report from the National Center for Health Statistics, part of the US Centers for Disease Control and Prevention. Fentanyl is a powerful, synthetic narcotic that has been blamed for the deaths of rock stars including Prince and Tom Petty. It works on the brain like morphine or heroin, but is 50 to 100 times more potent, and can easily lead to overdose.

The rate of drug overdose deaths in the United States has tripled from 1999 through 2016, as the nation grapples with a persistent opioid epidemic. Fentanyl-related drug overdose deaths have doubled each year from 2013 through 2016, “from 0.6 per 100,000 in 2013 to 1.3 in 2014, 2.6 in 2015, and 5.9 in 2016,” said the report. Meanwhile, deaths from heroin and methamphetamine more than tripled from 2011 to 2016. Heroin was the top cause of drug overdose death from 2012 to 2015, said the report. The prescription painkiller Oxycodone ranked highest in 2011.

Every word of this is broken. Time defends the MSM against Trump, but he didn’t create fake news. I like the term ‘abuse of truth’, that verges on doublespeak, as does ‘..the willingness to dismiss anything including credible news reporting as fake news”. And c’mon, free and fair press? Who believes that?

Despite the White House ramping up its rhetoric, the United States remains a free and fair press, Ben Goldberger the assistant managing editor of Time magazine told CNBC on Wednesday. The year 2018 has been marked by manipulation, abuse of truth, along with efforts by governments to instigate mistrust of the facts, the magazine said in an essay when it named killed and imprisoned journalists as Person of the Year for 2018 on Tuesday. “There’s no doubt that the rhetoric from the White House about the demonization of the media as ‘the enemy of the people,’ or the willingness to dismiss anything including credible news reporting as fake news, is incredibly worrisome and chilling,” Goldberger said. “But that said, I return to what I said about the United States — this remains a free and fair press.” “Journalists here enjoy legal protections that are the envy of those in virtually every other country,” he added.

With stocks down significantly, corporate buybacks could help stabilize the market. Buybacks have been one of the big stories supporting the market this year. DataTrek estimates that in the last 12 months, the companies in the S&P 500 have purchased $646 billion of their own stock, 29 percent more than the previous 12 months. And there’s plenty of “dry powder” left. One firm estimates at least $350 billion of buybacks that have been planned for the year and are just waiting to be put to work. And no, it is not just Apple that is buying its own stock. More than 300 large-cap companies have active buyback programs.

Unfortunately, some traders are resurrecting an old chestnut to help explain the current market weakness. They say we are entering a “blackout” period, when corporations cannot buy their stock because they are about to report quarterly earnings. It’s a neat explanation, except there’s not a lot to it. “Buybacks do occur during blackout periods,” Ben Silverman at InsiderScore told me. “Buyback volume does often decline in the first month of the quarter due to some buyback blackouts,” but companies can, and do, continue to buy back stock, he told me. Another trader (who declined to be identified) confirmed Silverman’s point. Corporate buybacks decline in the month before earnings, but only marginally. He estimated the decline is 30 percent or less.

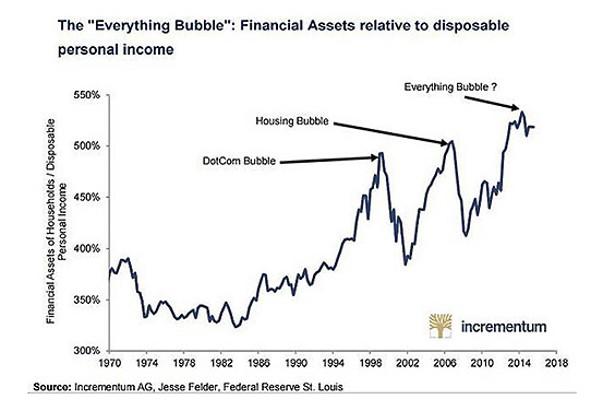

The first thing we must understand is that we are not facing a panic created by a black swan, that is, an unexpected event, but by three factors that few could deny were evident: 1) Excessive valuations after $20 trillion of monetary expansion inflated most financial assets. 2) Bond yields rising as the US 10-year reaches 3.2%. 3) The evidence of the Yuan devaluation, which is on its way to surpass 7 Yuan per US dollar. 4) Global growth estimates trimmed for the sixth time in as many months. Therefore, the US rate hikes – announced repeatedly and incessantly for years – are not the cause, nor the alleged trade war. These are just symptoms, excuses to disguise a much more worrying illness.

What we are experiencing is the evidence of the saturation of excesses built around central banks’ loose policies and the famous “bubble of everything”. And therein lies the problem. After twenty trillion dollars of reckless monetary expansion, risk assets, from the safest to the most volatile, from the most liquid to the unquoted, have skyrocketed with disproportionate valuations.

The cracks in the building always appear first with currencies. Countries that have become accustomed to the idea that “this time is different” and that debt does not matter, started to multiply their indebtedness in foreign currency. Debt in dollars from emerging countries soared to 41% of their total debt. In the first three months of 2018, global debt rose 11% to a record of 247 trillion dollars (according to the IIF), and that of emerging markets soared by 2.5 trillion to an all-time high of 58.5 trillion. . When the lowest risk bond, the United States 10-year, went to 3.1%, the synchronized growth and complacent veil lifted, and many assets showed how risky they truly are.

Markets woke up to a reality that we had decided to ignore. That rates do rise. And if the safest bond gives a return of 3.2% … Am I willing to buy bonds from much riskier countries with negligible spreads? Add to that “sobriety” effect, another one. The inevitable devaluation of the yuan , which soared to almost 7 against the dollar. Am I willing to buy emerging markets and commodities when China exports its imbalances sending disinflationary pressure to the rest of the world?

Days after the collapse of 97% of its banking industry, Icelandic authorities designed a comprehensive policy of accountability, based on two overlapping objectives: establishing the truth and punishing those responsible. An independent truth commission was mandated to document the causes of the meltdown, and the newly established Office of the Special Prosecutor was tasked to thoroughly investigate and prosecute those responsible for any crimes committed in the run up to the crisis. Both mechanisms have been remarkably successful.

Published in 2010, the truth commission’s 2,200-page report not only documented the manifold failings of the financial system in Iceland but also offered specific recommendations to protect state institutions from a future crisis. The report instantly became a bestseller, with copies sold in supermarkets. It was a popular gift – parents even gave it to their children to help them avoid making the same mistakes. The Office of the Special Prosecutor successfully prosecuted 40 bank executives. This is remarkable, especially given the small population of the island and the comparative experience of other European countries affected by the recession, such as Ireland, Cyprus, or the UK (table below).

For decades, developing countries have relied on outside investments to boost their growth despite trade imbalances. But running a current account deficit has come to be regarded as “a sin,” according to Singapore’s deputy prime minister. Such a development is just “crazy,” Tharman Shanmugaratnam told CNBC on Friday during the annual meeting of the Institute of International Finance on the Indonesian island of Bali. Shanmugaratnam was referring to the widely held outlook that nations should seek to avoid current account deficits — which indicate they’re operating on borrowed means because the value of incoming goods, services and investments exceeds the amount leaving the country.

“How did the Singapores and Koreas of the world grow?” he said. “We grew by running current account deficits at an early stage of development so we could invest ahead for growth while our savings were being built up.” Singapore was able to rely on financing through foreign direct investments and long-term investors during its early years of growth, as the international financial system at that time had capital flowing to developing economies, Shanmugaratnam said. “Today, it’s a sin to run a current account deficit and that’s crazy,” said the minister, who is also the chairman of the Monetary Authority of Singapore, the country’s central bank and financial regulator. “I mean, it’s bad in economics, it’s bad in policy sense, and the whole world is going to suffer.”

European Central Bank President Mario Draghi is sending a warning to Rome ahead of its formal budget submission: Don’t expect the ECB to save the day. In a Saturday press conference at the IMF and World Bank meetings in Bali, Indonesia, Draghi said he was confident that a budget agreement would be reached and urged all parties to “calm down with the tone.” He also voiced relief that there has not been evidence of a wider spillover effect in European bond markets, even as Italian yields hit multi-year highs. “Everything that happened today is local to Italy.”

When asked whether an eventual realization of contagion or a further rise in Italian yields would force the ECB to scrap tightening plans by year end, Draghi told CNBC: “I don’t want to speculate on this. I just don’t want to conceive such a hypothesis. I’m confident that the authorities — and by the way all parties, not only Italy — all parties will in the end find a compromise solution, an agreement.” He went on to suggest that the situation had been “dramatized,” and that was “not the first time there are deviations from established rules in Europe.” But investors are worried that the Italian government may seize on that precedent and take a gamble that running foul of EU budget rules won’t incur serious penalties, and that, if things do turn worse for Italian financial markets, they”ll be able to lean on the ECB for support. Draghi, for his part, told CNBC that would not be a possibility.

Ottawa will keep its $15bn arms deal with Riyadh despite concerns over Saudi involvement in the disappearance of dissident journalist Jamal Khashoggi and the diplomatic row over human rights, Prime Minister Trudeau said. “We respected that contract,” Canadian Prime Minister Justin Trudeau told reporters on Friday, adding that his cabinet has put forward measures to make the arms sales more transparent. “We are making sure Canadians’ expectations and laws are always being followed,” he said. The contract was signed in 2014 by the previous conservative government, and has since been upheld by Trudeau. The specifics of the sales were originally not disclosed by the parties.

According to documents obtained by CBC News last month, a Canadian company is to ship 742 LAV-6 light armored vehicles to Riyadh. The same outlet revealed in March that hundreds of the LAV-6s will be outfitted as “heavy assault” and “anti-tank” types. [..] Human rights campaigners and journalists have criticized Canada’s approach to Saudi Arabia as inconsistent. They point out that the government doesn’t mince words when attacking the kingdom’s human rights record, but at the same time never waivers in its willingness to ship military hardware to Riyadh. Media reports have also strongly suggested that the Saudis might be using Canadian-made LAVs against civilians in Yemen.

[..] Canada stuck to the arms deal even after becoming embroiled in a diplomatic spat with Riyadh in August. Foreign Minister Chrystia Freeland called on the kingdom to release two high-profile dissidents. In response, Saudi Arabia expelled the Canadian envoy. It then froze trade talks, cut academic ties, and suspended flights to Canada.

Cabinet ministers should “exert their collective authority” and rebel against Theresa May’s proposed Brexit deal, ex-Brexit Secretary David Davis has said. The PM has suggested a temporary customs arrangement for the whole UK to remain in the customs union while the Irish border issue is resolved. Brexiteers suspect this could turn into a permanent situation, restricting the freedom to strike trade deals. Writing in the Sunday Times, Mr Davis said the plan was unacceptable. “This is one of the most fundamental decisions that government has taken in modern times,” he added.

The issue of the border between Northern Ireland and the Republic Ireland is one of the last remaining obstacles to achieving a divorce deal with Brussels, with wrangling continuing over the nature of a “backstop” to keep the frontier open if a wider UK-EU trade arrangement cannot resolve it. The EU’s version, which would see just Northern Ireland remain aligned with Brussels’ rules, has been called unacceptable by Mrs May and the DUP. Mr Davis said the government’s negotiating strategy had “fundamental flaws”, arising from the “unwise decision in December to accept the EU’s language on dealing with the Northern Ireland border”.

On Saturday evening, German newspaper Suddeutsche Zeitung reported a deal had already been reached between Mrs May and the EU, and would be announced on Monday. But a No 10 source told the BBC the report was “100%, categorically untrue” and negotiations were ongoing. The paper said it had seen a leaked memo from EU negotiators to EU ambassadors stating: “Deal made.”

[..] early Sunday in London, the Brexiteer hardliners published an open letter signed by 63 Conservative MPs, including David Davis, the former Brexit secretary, Jacob Rees-Mogg, the chairman of the European Research Group of Eurosceptic backbenchers and former Brexit minister Steve Baker, the former Brexit minister. At the same time, Anne-Marie Trevelyan, a pro-leave MP, published an editorial in the Sunday Telegraph demanding that any possibility that the UK could remain in a “temporary customs arrangement” after the Brexit transition period ends in December 2020 be stricken from the final agreement – because leaving open the possibility would be tantamount to ignoring the political will of the 17.4 million Britons who voted for Brexit.

Meanwhile, Davis demanded in an editorial in the Sunday Times that Cabinet ministers should “exert their collective authority” and rebel against Theresa May’s proposed Brexit deal. All of this is happening amid even more conflicting reports, citing sources from the EU and sources from No. 10 Downing Street, affirming and denying that a deal had been reached. Underscoring the hostility to a deal, the leader of Northern Ireland’s Democratic Unionist Party said Sunday that she would prefer a “no deal” Brexit to a “backstop” transition agreement that would require any borders between Northern Ireland and the UK, arguing that this would amount to the “annexation” of Northern Ireland by the EU, per CNBC.

While most indie media was focused on debating the way people talk about Kanye West and the disappearance of Saudi journalist Jamal Khashoggi, an unprecedented escalation in internet censorship took place which threatens everything we all care about. It received frighteningly little attention. After a massive purge of hundreds of politically oriented pages and personal accounts for “inauthentic behavior”, Facebook rightly received a fair amount of criticism for the nebulous and hotly disputed basis for that action. What received relatively little attention was the far more ominous step which was taken next: within hours of being purged from Facebook, multiple anti-establishment alternative media sites had their accounts completely removed from Twitter as well.

As of this writing I am aware of three large alternative media outlets which were expelled from both platforms at almost the same time: Anti-Media, the Free Thought Project, and Police the Police, all of whom had millions of followers on Facebook. Both the Editor-in-Chief of Anti-Media and its Chief Creative Officer were also banned by Twitter, and are being kept from having any new accounts on that site as well.

“I unfortunately always felt the day would come when alternative media would be scrubbed from major social media sites,” Anti-Media’s Chief Creative Officer S.M. Gibson said in a statement to me. “Because of that I prepared by having backup accounts years ago. The fact that those accounts, as well as 3 accounts from individuals associated with Anti-Media were banned without warning and without any reason offered by either platform makes me believe this purge was certainly orchestrated by someone. Who that is I have no idea, but this attack on information was much more concise and methodical in silencing truth than most realize or is being reported.”

Finance professor John Griffin, along with his doctoral student companion, Amin Shams, were the two academics that drew market-moving conclusions about bitcoin last year, while the digital currency was trading around $20,000. After sifting through 2 terabytes of trading data, they alleged that bitcoin was being manipulated by someone using the cryptocurrency Tether to purchase it. Tether remains a relatively little-known crypto, which is pegged to one US dollar. Part of its appeal is that it can “stand in” for dollars when necessary, according to Bloomberg. Griffin and Shams authored a paper in June, with the results of their findings ultimately catalyzing many digital assets to move lower, despite the fact that the CEO of Tether publicly denied that its currency was used to prop up bitcoin.

Griffin works at the University of Texas at Austin, and has become quite an unpopular figure on Wall Street for similar work he has done in the past on ratings companies, the VIX and investment banks. In most of his findings, he claims that these well-known financial instruments and players are, in one way or another, rigged. And the professor seems to enjoy exposing precisely that: rigged, manipulated markets and shady players. “I not only want to understand the world, but make it better,” he told Bloomberg. Griffin’s work has become popular reading within the DOJ and the Commodity Futures Trading Commission, according to Bloomberg.

These regulators – many of them low on resources, time and staff – welcome any additional help they can get (the SEC’s budget has forced it into a hiring freeze and the CFTC budget was cut by Congress in March of this year). John Reed Stark, a former attorney in the SEC’s enforcement division, stated: “It’s incredibly helpful to have an expert of Griffin’s caliber.”

If I were President, I’d declare Oct 12 Greater Fool Day. (Nobody likes Christopher Columbus anymore, that genocidal monster of dead white male privilege.) The futures are zooming as I write, a last roundup for suckers at the OD corral, begging the question: who will show up on Monday. Nobody, I predict. And then what? The great false front of the financial markets resumes falling over into the November election. The rubble from all that buries whatever is left of the automobile business and the housing market. The smoldering aftermath will be described as the start of a long-overdue recession — but it will actually be something a lot worse, with no end in sight.

The Democratic Party might not be nimble enough to capitalize on the sudden disappearance of capital. Their only hope to date has been to capture the vote of every female in America, to otherwise augment their constituency of inflamed and aggrieved victims of unsubstantiated injustices. It’s been fun playing those cards, and the Party might not even know how to play a different game at this point. Democratic politicians may also be among the one-percenters who watch their net worth go up in a vapor in a market collapse, leaving them too numb to act. The last time something like this happened, in the fall of 2008, candidate Barack Obama barely knew what to say about the fall of Lehman Brothers and the ensuing cascade of misery — though unbeknownst to the voters, he was already a hostage of Wall Street.

Complicating matters this time will be the chaos unleashed in politics and governing when the long-running “Russia collusion” melodrama boomerangs into a raft of indictments against the cast of characters in the Intel Community and Department of Justice AND the Democratic National Committee, and perhaps even including the Party’s last standard bearer, HRC, for ginning up the Russia Collusion matter in the first place as an exercise in sedition. The wheels of the law turn slowly, but they’ll turn even while financial markets tumble. And the threat to order might be so great that an unprecedented “emergency” has to be declared, with soldiers in the streets of Washington, as was sadly the case in 1861, the first time the country turned itself upside down.

The loudest and most powerful voices when it comes to the future of the planet — the ones with their hands on the levers of power — have a strong tactical advantage: they will be dead before the shit really hits the fan. This fact curiously goes unspoken, for the most part. Popular arguments tend to be framed around a rosy vision preserving the planet for future generations, which gives our boomer aristocracy the most effective cover story imaginable. They don’t need to care about that, as nice as it sounds. Why would they? It’s all completely hypothetical to them. You may as well be talking about climate patterns in Narnia. Make no mistake: older generations living in the developed world are part of history’s most under-appreciated death cult.

This isn’t abstract psychoanalysis. There is a brutal calculus going on in the minds of everyone from your skeptic uncle to the bankrollers of squillion dollar think tanks whenever they think or talk about climate change. They know that they will never have to really answer for their opinions on this matter, because they’ll be six feet under (and loving it!) when the world’s arable land is rendered infertile and its coastal cities flooded by rising oceans. In some dark and venal corner of their minds, they’re thinking about that fact all the damn time. Despite the frightening predictions of the new IPCC report, they’ve still got plenty of wiggle room to keep denying until they’re dead – which will be sooner rather than later. With any luck they’ll even avoid being held accountable in any concrete way, which for the conservative commentariat is an even worse fate than the Mad Max hellworld towards which we are hurtling.

[..] a scientist named Richard Alley in a Skype discussion with students at Bard College, as well as with Eban Goodstein, director of the Graduate Programs in Sustainability at Bard. It would be just another nerdy Skype chat except Alley is talking frankly about something that few scientists have the courage to say in public: As bad as you think climate change might be in the coming decades, reality could be far worse. Within the lifetime of the students he’s talking with, Alley says, there’s some risk — small but not as small as you might hope — that the seas could rise as much as 15-to-20 feet.

[..] Richard Alley is not a fringe character in the world of climate change. In fact, he is widely viewed as one of the greatest climate scientists of our time. If there is anyone who understands the full complexity of the risks we face from climate change, it’s Alley. And far from being alarmist, Alley is known for his careful, rigorous science. He has spent most of his adult life deconstructing past Earth climates from the information in ice cores and rocks and ocean sediments. And what he has learned about the past, he has used to better understand the future. For a scientist of Alley’s stature to say that he can’t rule out 15 or 20 feet of sea-level rise in the coming decades is mind-blowing.

And it is one of the clearest statements I’ve ever heard of just how much trouble we are in on our rapidly warming planet (and I’ve heard a lot — I wrote a book about sea-level rise). To judge how radical this is, compare Alley’s numbers to the latest report from the Intergovernmental Panel on Climate Change, which was released on Monday. That report basically argued that if we don’t get to zero carbon emissions by 2050, we have very little chance of avoiding 1.5 Celsius of warming, the threshold that would allow us to maintain a stable climate. The report projected that with 2 Celsius of warming, which is the target of the Paris Climate Agreement, the range of sea level rise we might see by the end of the century is between about one and three feet.

The British Museum is launching an initiative intended to counter the perception that its collections derive only from looted treasures. The monthly Collected Histories talks, which begin on Friday, will provide information on how certain artefacts entered the collection, with the museum saying it will offer a more nuanced take on these stories than is available elsewhere. The museum has long faced criticism for displaying – and refusing to return – looted treasures, including the Parthenon Marbles, Rosetta Stone, and the Gweagal shield.

Earlier this year, the art historian Alice Procter’s Uncomfortable Art Tours around London institutions, including the British Museum, made headlines for their attempts to expose the role of colonialism, with those on the tour given “Display It Like You Stole It” badges. Dr Sushma Jansari, the curator of the Asian ethnographic and South Asia collections at the British Museum, said she had devised Collected Histories in response to Procter’s tours. “There are a lot of partial histories and they tend to focus on the colonial aspect of the collecting so you have a bunch of people who tend to be quite angry and upset,” she said. “We’re trying to reset the balance a little bit. A lot of our collections are not from a colonial context; not everything here was acquired by Europeans by looting.”

Yes, it is hard to believe, but still happening: 10 years after Lehman the very same people who either directly caused the financial crisis of 2008 or made things much much worse in its aftermath, are not only ALL walking around freely and enjoying even better paid jobs than 10 years ago, they are even asked by the media to share their wisdom, comment on what they did to prevent much much worse, and advise present day politicians and bankers on what THEY should do.

You know, what with all the wisdom, knowledge and experience they built up. because that’s the first thing you’ll hear them all spout: Oh YES!, they learned so many lessons after that terrible debacle, and now they’re much better prepared for the next crisis, if it ever might come, which it probably will, but not because of but despite what their wise ass class did back in the day.

Which never fails to bring back up the question about Ben Bernanke, who said right after Lehman that the Fed was entering ‘uncharted territory’ but ever after acted as if the territory had started looking mighty familiar to him, which is the only possible explanation for why he had no qualms about throwing trillion after trillion of someone else’s many at the banks he oversaw.

Somewhere along the line he must have figured it out, right, or he wouldn’t have done that?! He couldn’t still have been grasping in the pitch black dark the way he admitted doing when he made the ‘uncharted territory’ comment?! Thing is, he never returned to that comment, and was never asked about it, and neither were Draghi, Kuroda or Yellen. Did they figure out something they never told us about, or were and are they simple blind mice?

We have an idea, of course. Because we know central bankers serve banks and bankers, not countries or societies. Ergo, after Lehman crashed, whether that was warranted or not, Bernanke and the Fed focused on saving the banks that were responsible for the crisis, instead of the people in the country and society that were not.

They threw their out-of-thin-air trillions at making the asset markets look good, especially stock markets. Knowing that’s what people look at, and knowing foreclosures are of fleeting interest and can be blamed on borrowers, not lenders, anyway when necessary.

And obviously they knew and know they are and were simply blowing yet another bubble, just this time the biggest one ever, but the wealth transfer that has taken place under the guise of saving the economy has made the rich so much money they can’t and won’t complain for a while. They actually WILL eat cake.

Everyone else, sorry, we ran out of money, got to cut pensions and wages and everything else now. Healthcare? Nice idea, but sorry. Housing, foodstamps? Hey, what part of ‘the government is broke’ don’t you understand? You’re on your own, buddy. Remember the America Dream? Let that be your Yellow Brick Road.

The banking class is going to divest of their shares, while the individuals, money funds and pensions funds who are also in stocks because nothing else made money, will find their cupboards and cabinets replete with empty bags. Right after that the economy will start tanking, and for real this time. Want a loan to buy a home, a car, to start a business? Sorry, told you, there’s no money left.

But look, the banks are still standing! You don’t understand this, but that’s much more important. And oh well, those were all honest mistakes. And the ones that perhaps weren’t, shareholders paid big fines for those, didn’t they? See, we can’t have those banking experts in jail, because we need them to build the economy back up after the next crisis. The knowledge and experience, you just can’t replace that.

And it will be alright, you’ll see. Sure, it’ll be like Florence and all of her sisters blew themselves all over flyover country, but hey, that cleans up a lot of stuff too, right? And who needs all that stuff anyway? What is more important for the economy after all, Lower Manhattan or Appalachia?

And who are you going to blame for all this? We strongly suggest you blame Donald Trump, we sure as hell will at the Fed. So just fall in line, that’s better for everyone. Blame his tax cuts, or better even, blame his trade wars. Nobody likes those, and they sound credible enough to have caused the crash when it comes.

Anyway, while you’re stuck with the emergency menu at Waffle House, we hope your socks’ll dry soon, we really do, and we’re sorry about Aunt Mildred and the dogs and cats and chickens that have gone missing, but then that’s Mother Nature, don’t ya know?! Even we can’t help that. All we can really do is keep our own feet dry.

Central bankers haven’t merely NOT saved the economy, they have used the financial crisis to feed additional insane amounts of money to those whose interests they represent, and who already made similarly insane amounts, which caused the crisis to begin with. They have not let a good crisis go to waste.

But judging from the comments and ‘analyses’ on Lehman’s 10-year anniversary, the financial cabal still gets away with having people believe they’s actually trying to save the economy, and they just make mistakes every now and then, because they’re only human and uncharted territory, don’t you know?! Well, if you believe that, know that you’re being played for fools. Preferences and priorities are crystal clear here, and you’re not invited.

All the talk about how important it is that a central bank be independent is empty nonsense if that does not also, even first of all, include independence from financial institutions like commercial banks etc. Well, it doesn’t. Ben Bernanke’s Waffle House is nothing but a front for Grand Theft Auto.

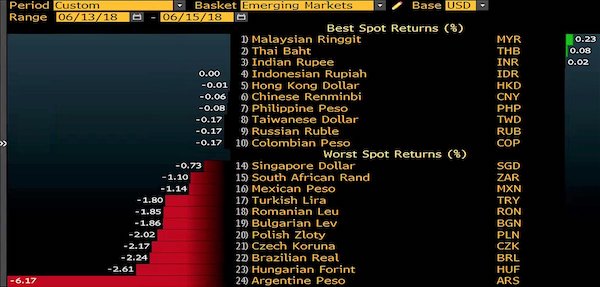

Today the Argentina peso plunged another 5.5% against the US dollar. It now takes ARS 27.7 to buy $1. Over the past 16 years, the peso has gone through waves of collapses. This collapse began on April 20. The central bank of Argentina (BCRA) countered it by selling $1 billion per day of scarce foreign exchange reserves and buying pesos. The peso fell more quickly. The BCRA responded with three rate hikes, to finally 40%! On May 8, the government asked the IMF for a bailout. On May 16, after a chaotic plunge of the peso, the BCRA was able to refinance about $26 billion in maturing peso-denominated short-term debt (Lebacs) at an annual interest of 40%, and the peso bounced. It was a dead-cat bounce, however, and the peso plunged another 13% against the dollar through today.

Since April 20, the peso has plunged 27.5%. The annotated chart shows the daily moves of the collapse, and the various failed gyrations to halt it (the chart depicts the value of 1 ARS in USD). The collapse of the peso comes despite an endless series of measures to halt it. Just this week so far: On Tuesday, the BCRA decided to keep its key interest rate at 40%; and on Wednesday, the Ministry of Finance announced it would hold daily auctions to sell $7.5 billion in foreign exchange reserves and buy pesos, to prop up the peso. But it was apparently the only one buying pesos. With inflation at 25.5% and heading to 27% by year-end, according to government estimates, with a rising budget deficit, a surging current account deficit, soaring borrowing costs, and burned investors, what else is there to do?

The European Central Bank has shrugged off evidence of a slowdown in the eurozone and announced that it will phase out the stimulus provided by its massive three-year bond-buying programme to the eurozone economy by the end of the year. Despite warning that the single currency area was going through a soft patch at a time when protectionist risks were rising, the ECB said it would wind down its bond purchases over the next six months. The ECB is currently boosting the eurozone money supply by buying €30bn of assets each month, but this will be reduced to €15bn a month after September and ended completely at the end of 2018.

The move follows strong pressure from some eurozone countries, led by Germany, that were uncomfortable about the more than €2.4tn of assets accumulated by the ECB since it launched its quantitative easing programme at the start of 2015. Mario Draghi, the ECB’s president, said at the end of a meeting of the bank’s governing council in Latvia that the QE programme had succeeded in its aim of putting inflation on course to meet its target of being below but close to 2%. Eurozone activity has accelerated markedly over the past three years, with some estimates suggesting that QE contributed 0.75percentage points a year to the average 2.25% annual growth rate.

The ECB’s statement reflected the battle between hawks and doves on the bank’s council, with the decision on QE matched by a softening of its approach to interest rates. Draghi said there would be no prospect of an increase in the ECB’s key lending rate – currently 0.0% – until next summer at the earliest. “We decided to keep the key ECB interest rates unchanged and we expect them to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with our current expectations of a sustained adjustment path,” Draghi said.

The Bank of Japan maintained its ultra-loose monetary policy on Friday and downgraded its view on inflation in a fresh blow to its long-held 2% price goal, further complicating the central bank’s path to rolling back its crisis-era stimulus. Markets are on the lookout for clues from BOJ Governor Haruhiko Kuroda’s post-meeting briefing on how long the central bank could hold off on whittling down stimulus given recent disappointingly weak price growth. As widely expected, the Bank of Japan kept its short-term interest rate target at minus 0.1% and a pledge to guide 10-year government bond yields around zero%.

The move contrasts with the European Central Bank’s decision to end its asset-purchase program this year and the U.S. Federal Reserve’s steady rate increases, which signaled a break from policies deployed to battle the 2007-2009 financial crisis. “Consumer price growth is in a range of 0.5 to 1%,” the BOJ said in a statement accompanying the decision. That was a slightly bleaker view than in the previous meeting in April, when the bank said inflation was moving around 1%. The BOJ stuck to its view the economy was expanding moderately, unfazed by a first-quarter contraction that many analysts blame on temporary factors like bad weather.

Federal Reserve Chairman Jerome Powell has taken the first steps in remaking the central bank in his “plain-English” image, which can only be a good thing for financial markets. Earlier this week, news leaked that the central bank was considering holding a press conference following each Federal Open Market Committee meeting instead of after every other one like it does now. The reports set off a mini-storm. Speculation rose the Fed would implement this new policy immediately, which could mean the central bank was considering accelerating the pace of interest-rate increases as soon as August. After all, investors had become accustomed to the Fed only making a major policy move at meetings followed by a press conference. Now, every meeting would be “live.”

But in a masterful move, Chairman Jerome Powell managed to confirm the policy while also putting financial markets at ease. Rather than announcing the change in the official statement outlining the Fed’s plan to raise its target for the federal funds rate for the seventh time since December 2015, Powell waited until the start of his press conference to drop the bomb, noting that the policy wouldn’t start until January. Here’s Powell’s reasoning: “My colleagues and I meet eight times a year and take a fresh look each time at what is happening in the economy and consider whether our policy needs adjusting. We don’t put our interest rate decisions on auto-pilot because the economy can always evolve in unexpected ways.

History has shown that moving interest rates either too quickly or too slowly can lead to bad economic outcomes. We think the outcomes are likely to be better overall if we are as clear as possible about what we are likely to do and why. To that end, we try to give a sense of our expectations for how the economy will evolve and how our policy stance may change. As Chairman, I hope to foster a public conversation about what the Fed is doing to support a strong and resilient economy. And one practical step in doing so is to have a press conference like this after every one of our scheduled FOMC meetings. We’re going to do that beginning in January. That will give us more opportunities to explain our actions and to answer your questions.

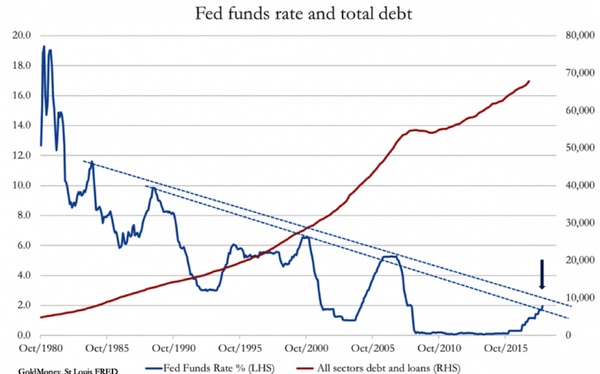

Since Hayek’s time, monetary policy, particularly in America, has evolved away from targeting production and discouraging savings by suppressing interest rates, towards encouraging consumption through expanding consumer finance. American consumers are living beyond their means and have commonly depleted all their liquid savings. But given the variations in the cost of consumer finance (between 0% car loans and 20% credit card and overdraft rates), consumers are generally insensitive to changes in interest rates. Therefore, despite the rise of consumer finance, we can still regard Hayek’s triangle as illustrating the driving force behind the credit cycle, and the unsustainable excesses of unprofitable debt created by suppressing interest rates as the reason monetary policy always leads to an economic crisis.

The chart below shows we could be living dangerously close to another tipping point, whereby the rises in the Fed Funds Rate (FFR) might be about to trigger a new credit and economic crisis. Previous peaks in the FFR coincided with the onset of economic downturns, because they exposed unsustainable business models. On the basis of simple extrapolation, the area between the two dotted lines, which roughly join these peaks, is where the current FFR cycle can be expected to peak. It is currently standing at about 2% after yesterday’s increase, and the Fed expects the FFR to average 3.1% in 2019. The chart tells us the Fed is already living dangerously with yesterday’s hike, and further rises will all but guarantee a credit crisis.

Some statesmen by their sheer force of personality and unorthodox ways of politicking arouse disdain among onlookers. US President Donald is perhaps the most famous figure of that kind in world politics today. No matter what he does, Trump attracts criticism. He evokes strong feelings of antipathy among a large and voluble swathe of opinion within half of America. The making of history in a virtual solo act on his part, which is the rarest of efforts, on Sentosa Island in Singapore on Tuesday and which the world watched with awe and disbelief, will be instinctively stonewalled. Half of America simply refuses to accept the positive tidings about him coming from Singapore.

The skeptics are all over social media pouring scorn, voicing skepticism, unable to accept that if the man has done something sensible and good for his country and for world peace, it deserves at the very least patient, courteous attention. The problem is about Trump – not so much the imperative need of North Korea’s denuclearization. But western detractors – ostensibly rooting for the “liberal international order” – will eventually lapse into silence because what emerges is that North Korean leader Kim Jong-un has enough to “bite” here in the deal that Trump is offering – broadly, a security guarantee from the US and the offer of a full-bodied relationship with an incremental end to sanctions plus a peace treaty.

Succinctly put, Trump has offered a deal that Kim simply cannot afford to reject. The ending of the US-ROK military exercises forthwith; Trump’s agenda of eventual withdrawal of troops from ROK; the lure of possible withdrawal of sanctions once 20% of the denuclearization process gets underway, or once the process becomes irreversible; Trump’s hint that he has sought assurances from Japan and the ROK that they will be “generous” in offering economic assistance to the reconstruction of North Korea; China’s involvement in the crucial process – these are tangibles.

The absence of any reference to “complete, verifiable, and irreversible dismantlement” (CVID) of North Korea’s nuclear program in the joint statement reached at US President Donald Trump and North Korean leader Kim Jong-un’s June 12 summit in Singapore is being seen by some as a “negotiation failure” on the US’s part. But an analysis of Trump’s subsequent remarks – and a reading between the lines of the Pyongyang’s official announcement – suggests the US achieved practical gains in terms of a commitment from the North in exchange for the face-saving measure of avoiding use of the “CVID” term due to possible North Korean objections to it.

To begin with, the Singapore joint statement’s language marks a step forward from the Panmunjeom Declaration of Apr. 27 in terms of the final goal of denuclearizing the Korean Peninsula. The latest statement refers to Kim having “reaffirmed his firm and unwavering commitment to complete denuclearization of the Korean Peninsula.” While the Panmunjeom Declaration referred to “realizing, through complete denuclearization, a nuclear-free Korean Peninsula,” the new statement includes the additional reference to a “firm and unwavering commitment.”

From the reference to Kim’s “firm and unwavering” commitment to denuclearization, some experts are suggesting North Korea may have agreed to verification in addition to denuclearization – in other words, that the language may be a substitute for the “verifiable” part of the CVID approach demanded by Washington. “You could see them as having used the term out of awareness of North Korea’s discomfort with the word ‘verification,’” Handong Global University professor Kim Joon-hyung said after a Korea Press Foundation debate at Singapore’s Swissotel on June 13. “It may be fair to say North Korea made a definite commitment on the implementation and verification issues,” Kim argued.

“..while you can always count on Capitol Hill to make it incredibly easy for a president to deploy military personnel around the globe, giving that same office the power to bring troops home is a completely different matter. ”

Off the top of my head I have a hard time thinking of anything sleazier than smearing peace talks in order to gain partisan political points, but that has indeed been the theme of the last few days when it comes to the Singapore summit. Liberal pundits everywhere have been busily circulating the narrative that Kim Jong-Un “played” Trump by getting him to temporarily halt military drills in exchange for suspended nuclear testing. It was the most fundamental beginning of peace negotiations and a slight deescalation in tensions on the Korean Peninsula, but the way they talk about it you’d think Kim had taken off from Singapore in Air Force One with the keys to Fort Knox and Melania on his lap.

I’m not sure how far up the military-industrial complex’s ass one’s head needs to be to think that one single step toward peace is a gigantic take-all-the-chips win for the impoverished North Korea, but many of Trump’s political enemies are taking it even further. Senate Democrats have introduced a bill to make it more difficult for Trump to withdraw US troops from South Korea, because while you can always count on Capitol Hill to make it incredibly easy for a president to deploy military personnel around the globe, giving that same office the power to bring troops home is a completely different matter.

Surprising no one, MSNBC’s cartoon children’s program The Rachel Maddow Show took home the trophy for jaw-dropping, shark-jumping ridiculousness with an eighteen-minute Alex Jones impression claiming that the chief architect of the Korean negotiations was none other than (and if you can’t guess whose name I’m going to write once we get out of these parentheses I deeply envy your ignorance on this matter) Vladimir Putin. [..] This president is facilitating acts of military violence and dangerous escalations around the world; anyone who isn’t relieved by the possibility of one powder keg being defused in that rampage actually has a lot more faith in Trump’s competence than they’re pretending to.

Private equity firm Blackstone, the undisputed king of property funds, continues to bet big on global real estate. In the last week it raised $9.4 billion for Asian real estate. It was also given the green light to acquire Spain’s biggest real estate investment fund (REIT), Hispania, for €1.9 billion. The move, after its prior acquisitions, will cement its position as Spain’s biggest hotel owner and fully private landlord. Hispania’s 46 hotels, added to Blackstone’s other hotels, will turn the PE firm into Spain’s largest hotelier with almost 17,000 rooms, far ahead of Meliá (almost 11,000), H10 (more than 10,000) and Hoteles Globales (just over 9,000).

It took Blackstone just three moves to become market leader. First, it acquired the hotel group HI Partners from struggling Spanish lender Banco Sabadell for €630 million in October 2017. Then, a month ago, it bought 29.5% of the hotel chain NH Hoteles, which is currently in the hands of the Chinese conglomerate HNA. Now, by raising its stake in Hispania from 16.75% to 100%, it will take up a dominant position in one of the world’s biggest tourist markets. With this deal, it will also expand its residential property empire in Spain. Blackstone has over 100,000 real estate assets controlled via dozens of companies. Those assets include a huge portfolio of impaired real estate assets, including defaulted mortgages and real estate-owned assets (REOs).

Blackstone also owns 1,800 social housing units, which it acquired from Madrid City Hall in a controversial deal brokered by the son of former Spanish prime minister José María Aznar and former Madrid mayor Ana Botella. Blackstone paid €202 million for the apartments in 2013; they are now estimated to be worth €660 million — a 227% return in just five year! Since its purchase of the properties, Blackstone has hiked rents on the flats by 49%. Those who can’t pay have been evicted. Blackstone also played a starring role in one of the world’s biggest real estate operations of 2017, in which it payed €5.1 billion for the defaulted loans Banco Santander inherited from its shotgun-acquisition of Banco Popular.

“..a dramatic drop in the number of Japanese properties available via Airbnb, from more than 60,000 this spring to just 1,000 on the eve of the law’s introduction.”

It has become a familiar scene: tourists in rented kimonos posing for photographs in front of a Shinto shrine in Kyoto. They and other visitors have brought valuable tourist dollars to the city and other locations across Japan. But now the country’s former capital is on the frontline of a battle against “tourism pollution” that has already turned locals against visitors in cities across the world such as Venice, Barcelona and Amsterdam. The increasingly fraught relationship between tourists and their Japanese hosts has spread to the short-stay rental market. On Friday a new law comes into effect that requires property owners to register with the government before they can legally make their homes available through Airbnb and other websites.

The restriction has caused the number of available properties to plummet and has cost the US-based company millions of dollars. Thanks to government campaigns, the number of foreign tourists visiting Japan has soared since the end of a flat period caused by a strong yen and radiation fears in the aftermath of the 2011 Fukushima disaster. A record 28.7 million people visited last year, an increase of 250% since 2012. Almost seven million were from China, with visitors from South Korea, Taiwan, Hong Kong Thailand and the US taking the next five spots. By 2020, the year Tokyo hosts the Olympic Games, the government hopes the number will have risen to 40 million.

[..] Under the new private lodging law, which was supposed to address a legal grey area surrounding short-term rentals – known as minpaku – properties can be rented out for a maximum of 180 days a year, and local authorities are permitted to impose additional restrictions. The result has been a dramatic drop in the number of Japanese properties available via Airbnb, from more than 60,000 this spring to just 1,000 on the eve of the law’s introduction. The legislation has forced the firm to cancel reservations for guests planning to stay in unregistered homes after Friday and to compensate clients to the tune of about $10m.

A sign in Kyoto cautions against touching geishas, taking selfies, littering, sitting on fences and eating and smoking on the street. Photograph: Justin McCurry for the Guardian

Greece is the least satisfied nation in the European Union, according to a Eurobarometer survey published Thursday. More specifically, the survey, conducted between March 17 and 28, showed that just 52% of Greeks said they were satisfied with their lives, compared to a 83% average for the 28-member bloc. Only 35% of Greeks surveyed said they were satisfied with the financial situation of their households, compared to 71% across the EU. A staggering 98% said the state of the country’s economy is bad while one in two Greeks said the country’s financial crisis is not over yet and that it will deteriorate even further. As for the country’s general situation, 94% said it is negative. Just 6% said the general situation was positive compared to the 51% average for EU member-states.

With Greece featuring prominently in Turkey’s election campaigning, Turkish Foreign Minister Mevlut Cavusoglu raised the tension a notch again Thursday, warning that not even a bird will fly over the Aegean without Ankara’s permission. Responding to criticism by Turkish ultra-nationalists that 18 islands have been “lost” to Greece in recent years, Cavusoglu said that since the crisis over the Imia islets in 1996 there have been no changes in the legal status of the Aegean. “Not only during our own rule, but before that there has been no change in the status of the Aegean. We will not allow this. Even in the case of research we will not give permission, not even to a bird in the Aegean,” he said during an interview with a Turkish radio station.

He went on to say that Turkey will make no concessions in the Aegean and Cyprus, and that Ankara will also begin gas exploration “around” the Eastern Mediterranean island. “We also have a drill,” he said. Turkey has vowed to stop Cyprus from drilling for gas and oil in its exclusive economic zone (EEZ), insisting there can be no development of the island’s natural resources without the participation of the Turkish Cypriots in the island’s Turkish-occupied north. “In the last few months we have prevented drilling and we drove the Italians away. We will not allow anyone to take away the rights of Turkish Cypriots,” he said. Cyprus government spokesman Prodromos Prodromou said that Nicosia will not be dragged into the “climate of tension” that Turkey is cultivating. He cited international law and said that Cyprus has an established EEZ. Moreover, he said the US, Russia and the European Union have all backed Cyprus’s rights.

James Comey once described his position in the Clinton investigation as being the victim of a “500-year flood.” The point of the analogy was that he was unwittingly carried away by events rather than directly causing much of the damage to the FBI. His “500-year flood” just collided with the 500-page report of the Justice Department inspector general (IG) Michael Horowitz. The IG sinks Comey’s narrative with a finding that he “deviated” from Justice Department rules and acted in open insubordination. Rather than portraying Comey as carried away by his biblical flood, the report finds that he was the destructive force behind the controversy. The import of the report can be summed up in Comeyesque terms as the distinction between flotsam and jetsam.

Comey portrayed the broken rules as mere flotsam, or debris that floats away after a shipwreck. The IG report suggests that this was really a case of jetsam, or rules intentionally tossed over the side by Comey to lighten his load. Comey’s jetsam included rules protecting the integrity and professionalism of his agency, as represented by his public comments on the Clinton investigation. The IG report concludes, “While we did not find that these decisions were the result of political bias on Comey’s part, we nevertheless concluded that by departing so clearly and dramatically from FBI and department norms, the decisions negatively impacted the perception of the FBI and the department as fair administrators of justice.”

The report will leave many unsatisfied and undeterred. Comey went from a persona non grata to a patron saint for many Clinton supporters. Comey, who has made millions of dollars with a tell-all book portraying himself as the paragon of “ethical leadership,” continues to maintain that he would take precisely the same actions again. Ironically, Comey, fired FBI deputy director Andrew McCabe, former FBI agent Peter Strzok and others, by their actions, just made it more difficult for special counsel Robert Mueller to prosecute Trump for obstruction. There is now a comprehensive conclusion by career investigators that Comey violated core agency rules and undermined the integrity of the FBI. In other words, there was ample reason to fire James Comey.

As we digest and unpack the DOJ Inspector General’s 500-page report on the FBI’s conduct during the Hillary Clinton email investigation “matter,” damning quotes from the OIG’s findings have begun to circulate, leaving many to wonder exactly how Inspector General Michael Horowitz was able to conclude: “We did not find documentary or testimonial evidence that improper considerations, including political bias, directly affected the specific investigative actions we reviewed” We’re sorry, that just doesn’t comport with reality whatsoever. And it really feels like the OIG report may have had a different conclusion at some point.

Just read IG Horowitz’s own assessment that “These texts are “Indicative of a biased state of mind but even more seriously, implies a willingness to take official action to impact the Presidential candidate’s electoral prospects.” Of course, today’s crown jewel is a previously undisclosed exchange between Peter Strzok and Lisa Page in which Page asks “(Trump’s) not ever going to become president, right? Right?!” to which Strzok replies “No. No he’s not. We’ll stop it.” Nevermind the fact that the FBI Director, who used personal emails for work purposes, tasked Strzok, who used personal emails for work purposes, to investigate Hillary Clinton’s use of personal emails for work purposes. Of course, we know it goes far deeper than that…

The Wall Street Journal’s Kimberley Strassel also had plenty to say in a Twitter thread:

1) Don’t believe anyone who claims Horowitz didn’t find bias. He very carefully says that he found no “documentary” evidence that bias produced “specific investigatory decisions.” That’s different

2) It means he didn’t catch anyone doing anything so dumb as writing down that they took a specific step to aid a candidate. You know, like: “Let’s give out this Combetta immunity deal so nothing comes out that will derail Hillary for President.”

3) But he in fact finds bias everywhere. The examples are shocking and concerning, and he devotes entire sections to them. And he very specifically says in the summary that they “cast a cloud” on the entire “investigation’s credibility.” That’s pretty damning.

4) Meanwhile this same cast of characters who the IG has now found to have made a hash of the Clinton investigation and who demonstrate such bias, seamlessly moved to the Trump investigation. And we’re supposed to think they got that one right?

5) Also don’t believe anyone who says this is just about Comey and his instances of insubordination. (Though they are bad enough.) This is an indictment broadly of an FBI culture that believes itself above the rules it imposes on others.

6) People failing to adhere to their recusals (Kadzik/McCabe). Lynch hanging with Bill. Staff helping Comey conceal details of presser from DOJ bosses. Use of personal email and laptops. Leaks. Accepting gifts from media. Agent affairs/relationships.

7)It also contains stunning examples of incompetence. Comey explains that he wasn’t aware the Weiner laptop was big deal because he didn’t know Weiner was married to Abedin? Then they sit on it a month, either cuz it fell through cracks (wow) or were more obsessed w/Trump

8) And I can still hear the echo of the howls from when Trump fired Comey. Still waiting to hear the apologies now that this report has backstopped the Rosenstein memo and the obvious grounds for dismissal.

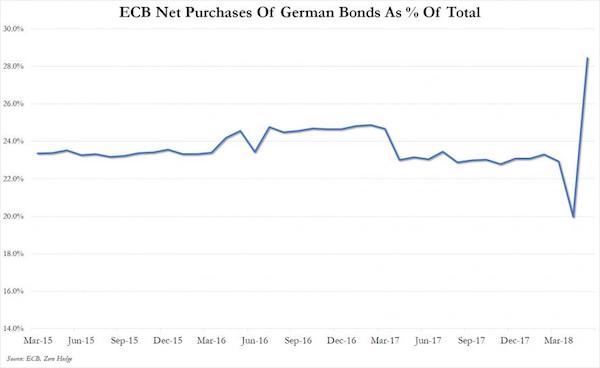

[..] as Bloomberg’s Lisa Abramowicz said in a podcast today, it was the ECB “basically just giving the finger to Italy.” Confirming as much, Anne Mathias, Global Rates and FX strategist for Vanguard, responded that “part of the vocal nature of the ‘talking about the talking about’ [the end of QE] probably has something to do with Italy, especially as they’ve been paring their purchases of Italian debt. What the ECB is trying to say is hey, “this is our party, and you’re welcome to it, but if you’re going to leave it’s not going to be easy for you.” The ECB is trying to show Italy a future without the ECB as backstop.”

A spot-on follow up question from Pimm Fox asked if this is “a situation in which the ECB is cutting off its nose to spite its face, because you can stick to rules for the sake of sticking to rules, but when you have a potential crisis, why wait for it to be a real crisis such as Italy, which the new government has pledged to spend a lot of money, to lower taxes, while they still have a huge government deficit. Why would the ECB do this.” The brief answer is that yes, it is, because sending the Euro and yields higher on ECB debt monetization concerns, only tends to destabilize the market, and sends a message to investors that the happy days are ending, in the process slamming confidence in asset returns, a process which usually translates into a sharp economic slowdown and eventually recession, or even depression if the adverse stimulus is large enough.